The biggest highlight of $Amazon.com(AMZN)$ Q3 earnings report released after the market on October 27th was the release of profits that exceeded expectations. As its consumer business showed higher-than-expected growth in an inflationary environment last quarter, the market naturally had high expectations for this part.

Although the post-market shock had an element of expected management, it also reflected the market's divergence in response to the sell-off of major technology company earnings reports over the past few days.

Summary

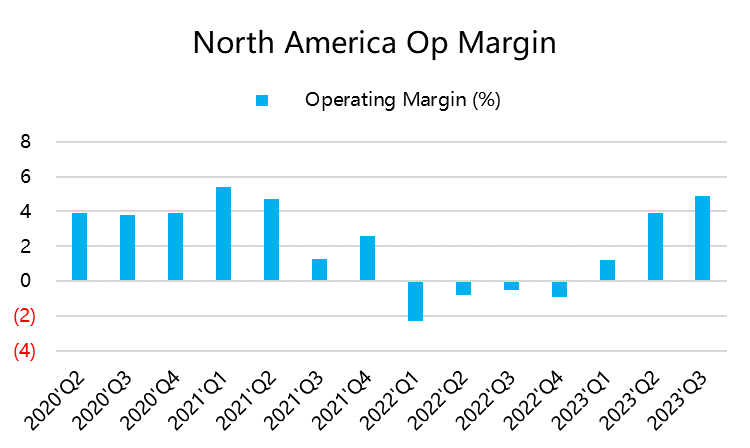

Retail sector's profits continued to rebound, supporting the release of large profits this quarter. The North American retail operating profit margin rose from 2.9% in Q2 to 3.9% in Q3, and international revenue growth was 16%, with an operating profit margin rebounding from -3% to -0.3%. However, the current consumption environment is affected by macro events such as inflation, high interest rates, rising commodity prices, and strikes, and Amazon does not have strong Q4 guidance, but rather more uncertainty.

AWS services still maintain a share of around 13%, although it cannot compare with Microsoft and Google, but it is considered stable, after all, its size is the largest. Through expected management, the company stated on its conference call that the opportunity for AI will bring "billions of dollars" in revenue to AWS in the next few years, and the stock price rose nearly 5% after the market closed.

Q4 revenue guidance median is $163.5 billion, lower than the market's expected $166.6 billion, but the operating profit guidance range is $7-11 billion, a significant increase from $5.5-8.5 billion in the previous quarter, and the overall year will turn from loss to profit, exceeding market expectations. Therefore, cost control will be the main support for performance.

At the current post-market stock price, the expected profit for 2023 is about 46 times PE, and for 2024 it is about 36 times PE.

Q3 Earnings Review

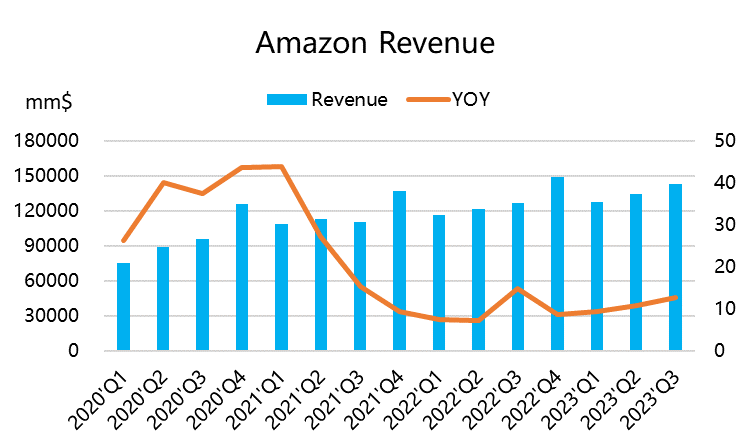

The company's total revenue was $143.1 billion, a year-on-year increase of 13%, exceeding market expectations of $141.4 billion.

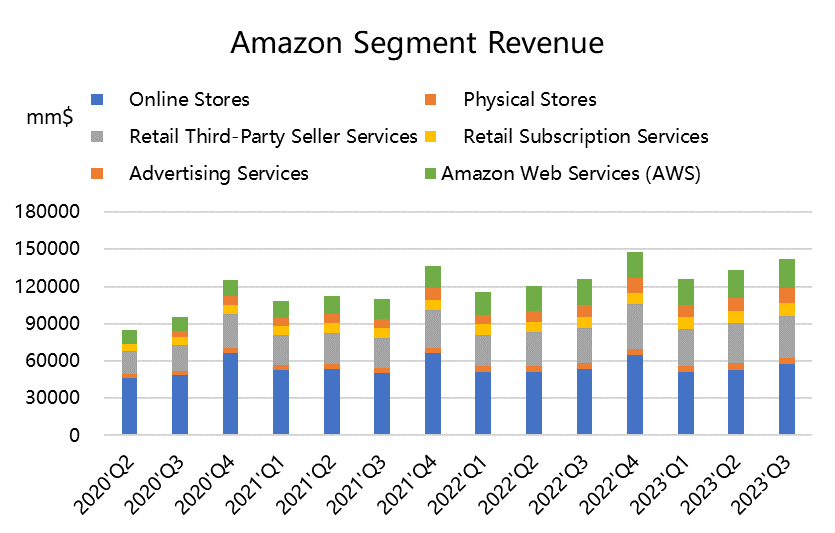

By business segment,

online store revenue reached $57.27 billion, a year-on-year increase of 7.1%, higher than the market's expected $56.82 billion;

physical store revenue reached $4.96 billion, a year-on-year increase of 5.7%, slightly higher than the market's expected $4.99 billion;

third-party seller services revenue reached $34.34 billion, a significant year-on-year increase of 19.8%, exceeding market expectations of $33.40 billion;

subscription services revenue reached $10.17 billion, a year-on-year increase of 14.2%, higher than the market's expected $10.13 billion;

advertising revenue was $12.06 billion, a year-on-year increase of 26.3%, higher than the market's expected $11.62 billion.

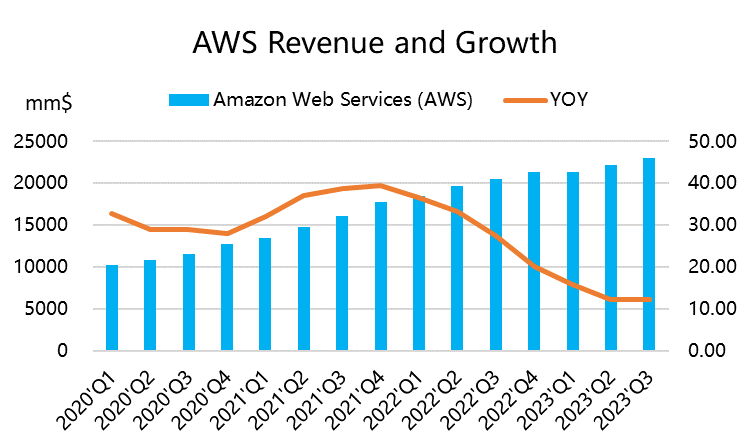

AWS business revenue increased by 12% year-on-year to $23.01 billion, lower than the market's expected $23.13 billion;

In terms of profit,

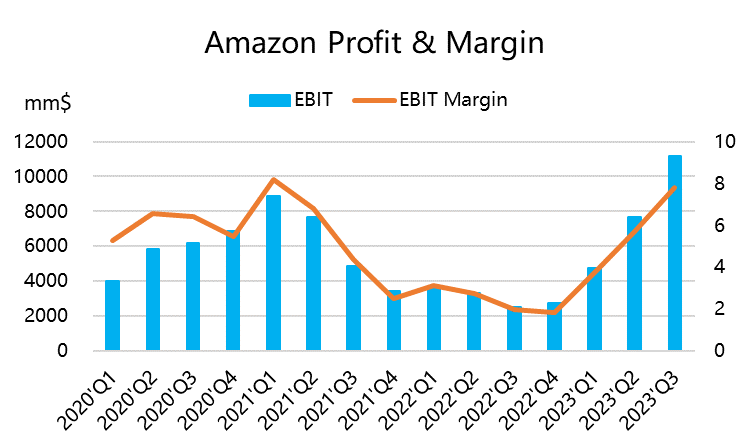

the gross profit margin was 47.57%, higher than the market's expected 45.38%,

and the operating profit margin was 7.82%, higher than the market's expected 5.46%; among them, the operating profit margin in North America increased to 3.9%, and the loss in international regions rebounded from -3% to -0.3%;

Diluted EPS was $0.94 (excluding the impact of $Rivian Automotive, Inc.(RIVN)$ ), while the market expected $0.6.

In terms of cash flow,

free cash flow was $21.43 billion, exceeding market expectations of $13.9 billion.

Looking ahead to Q4, the company expects revenue to be in the range of $160 billion to $167 billion, with a midpoint expectation of $163.5 billion, which is less than the expected $166.6 billion, and a year-on-year growth rate of less than 10%.

Retail business leverage is increasing, and profits are expanding.

In terms of Amazon's retail business, the growth rate of online stores returned to positive in Q2, and the growth rate of third-party seller services continued to increase by nearly 20%, which is the effect of price increases and has become the main incremental driver of retail business.

The growth rate of offline stores is still in the mid-single digits, indicating the sluggishness of offline business under high inflation. Amazon's membership services support its online shopping and become an important moat by connecting merchants and buyers. Even low-cost competitors like Temu find it difficult to break through the Prime membership system surrounded by a huge logistics system. Therefore, Amazon's online retail advantages are more obvious.

Since Q1 of this year, the operating profit in the United States has returned to positive and increased to 3.9% in Q3, and the rise in marginal profit margin will continue to increase future profit margins. However, looking at the Q4 guidance, the company appears to be relatively conservative. Although it is the shopping season, under the high inflation, high interest rate environment, and the impact of strikes and other events, it did not increase revenue indicators, but increased profit margins more from cost management.

AWS growth stabilizes, and imagination and expectation management are very important.

The growth rate of Amazon Web Services remained at 12-13% this quarter, close to $23.1 billion, which is basically in line with expectations and the first stabilization in the past seven quarters.

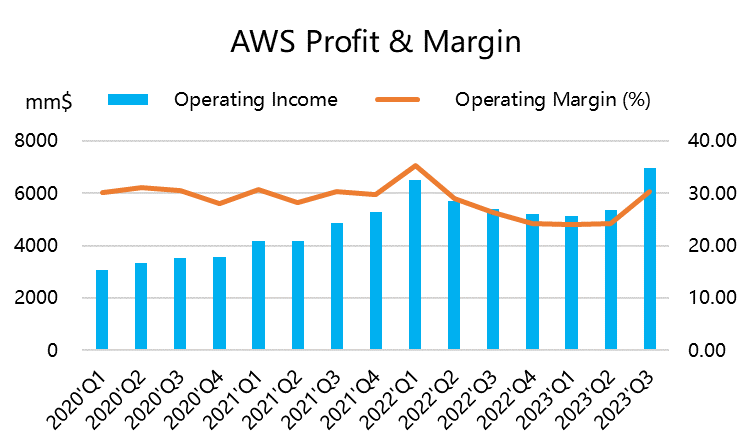

However, the operating profit of $7 billion surged by 29% year-on-year, exceeding expectations by $1.3 billion, and the profit margin soared to 30.25%, which was also surprising to the market.

Overall, the demand for cost reduction by enterprises in a high inflation environment also to some extent affects Amazon Web Services, and the incremental demand for AI may need to be reflected continuously over several quarters. However, on the conference call, the company stated that generative AI is already a relatively large business for Amazon. AWS continues to make breakthroughs in innovation and rapid delivery, making the combination of customized AI chips and Amazon Bedrock the simplest and most flexible way to build and deploy generative AI applications. Currently, companies working with AWS on AI-related services include adidas, Booking.com, GoDaddy, LexisNexis, Merck, Royal Philips, and United Airlines.

In addition, advertising revenue was $12.06 billion, exceeding $10 billion for two consecutive quarters, with a year-on-year growth rate of 26.3%, higher than the market's expected $11.62 billion.

Although there is still uncertainty in the macro environment, merchant advertising has become Amazon's next growth driver. Amazon's online advertising has developed into a profitable business for this online retailer, with revenue accounting for approximately 7.3% of the global digital advertising market, which further confirms that economic activity is higher than expected.

Of course, the performance of $Alphabet(GOOG)$ and $Meta Platforms, Inc.(META)$ a few days ago also proves the recovery of the industry, but the Q4 guidance is relatively conservative under more uncertainty trends, and Amazon should also follow this trend.

Valuation

After Q3 earning report, there is still room for further increase in profit margin. Although revenue growth may continue to decline, the overall cash flow from AWS and retail business will help it return to normal valuation levels.

Currently, its trailing twelve-month price-earnings ratio has returned to 56 times, which is expected to correspond to a profit expectation of about 46 times PE in 2023, and about 36 times in 2024.

The post-market volatility also reflects the current market divergence. On the one hand, there is selling pressure on the overall pullback of large technology companies, and on the other hand, there is a rebound after "Sell The Fact" and stronger expectations for Q4 AI business.

If AMZN can lead the market to rebound on Friday, it may temporarily alleviate the current market's pessimistic sentiment.

Comments