$Pinterest, Inc.(PINS)$ released its financial report after the market closed. In addition to exceeding expectations in terms of current user numbers, revenue, and profit levels, the company expressed great confidence in doubling its full-year profit margin and mentioned multiple times the help of AI in the company's performance. A few days prior, $Snap Inc(SNAP)$ lso announced strong Q3 performance.

PINS Q3 Earnings

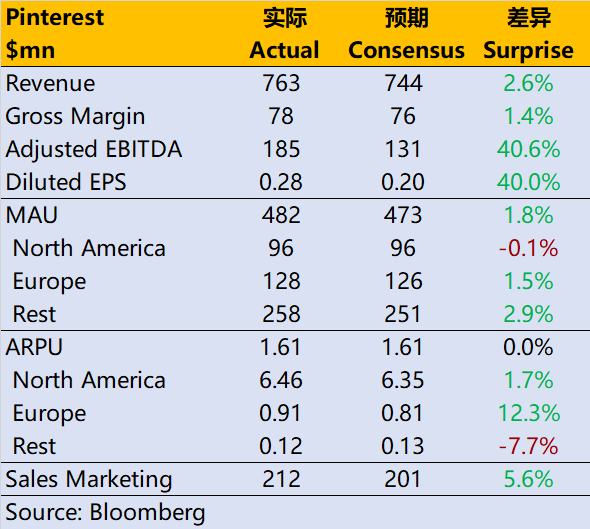

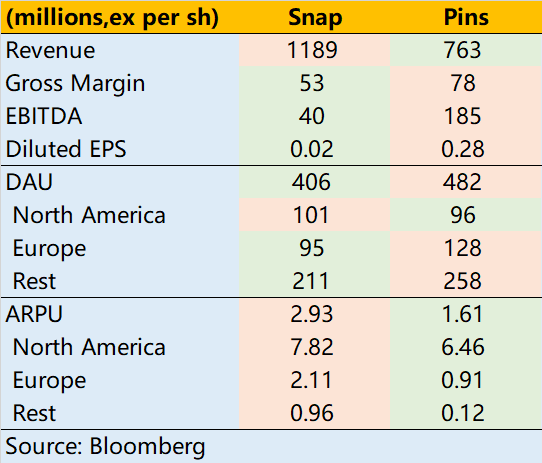

Revenue unexpectedly achieved double-digit growth of 11%, reaching $763 million, exceeding market expectations of $744 million.

Adjusted EBITDA was $185 million, higher than the market's expected $135.1 million; net profit went from a loss of $65.2 million in the same period last year to a profit of $6.7 million.

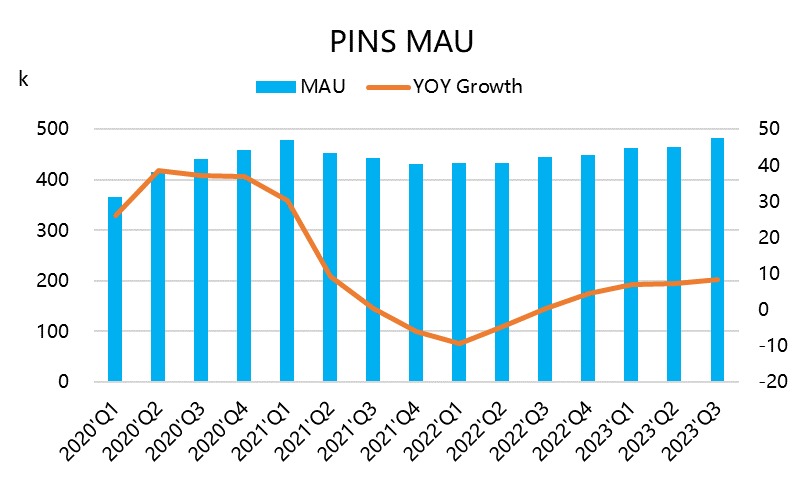

In terms of users, global MAUs increased by 8% to 482 million, higher than the market's expected 473 million; North America had 96 million, which was in line with expectations, Europe had 128 million, higher than the market's expected 126 million, and the remaining regions had 258 million, higher than the market's expected 251 million.

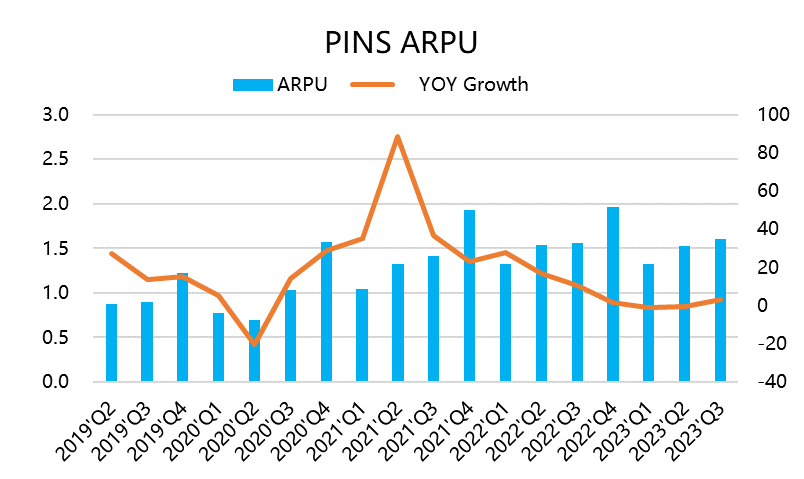

ARPU overall was $1.61, up 3.21% from the previous quarter, which had declined for two consecutive quarters, and in line with expectations; North America had $6.46, higher than the market's expected $6.35.

Q3 continued to accelerate business development. We achieved strong revenue performance, rapid growth in global monthly active users, and a significant expansion of profit margins. With differentiated advantages, we are finding the "best product/market fit" in years.

Looking ahead to Q4, revenue is expected to grow by 11% to 13%, and non-GAAP operating expenses are expected to decrease by 9% to 13% YoY. Adjusted EBITDA margin is expected to increase by 400 basis points in 2023, doubling the planned 200 basis points at the beginning of the year.

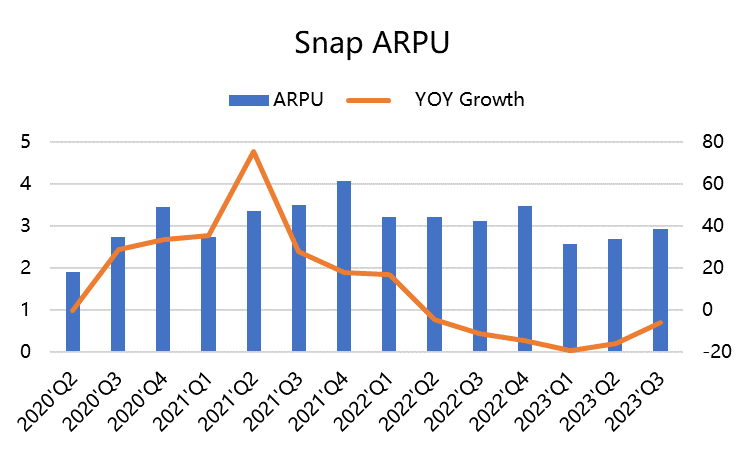

SNAP Q3 Earnings

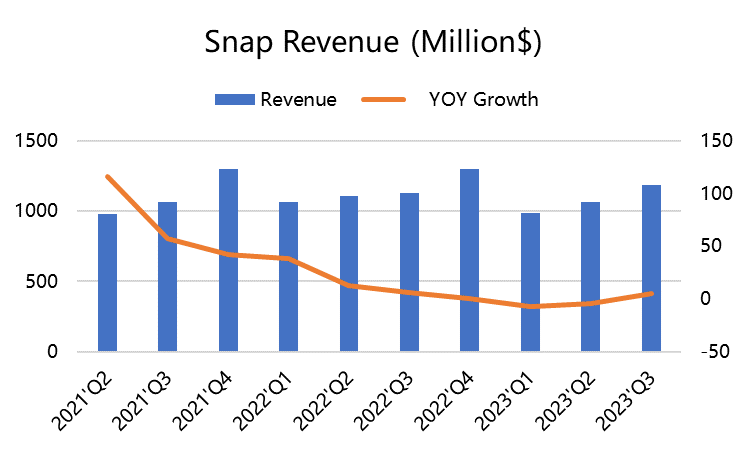

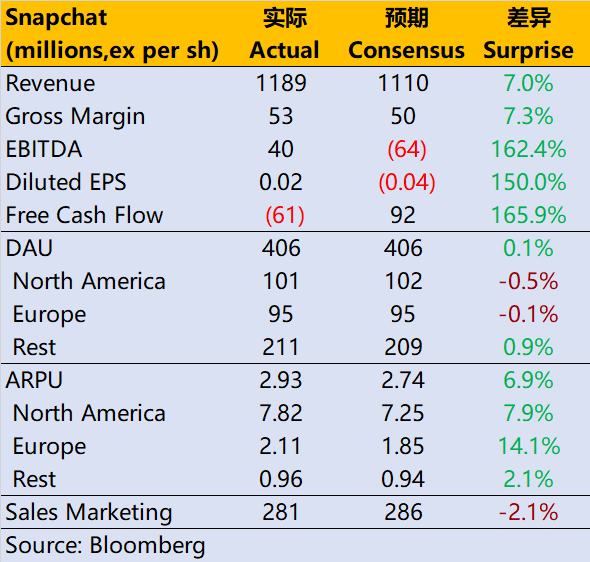

Revenue was $11.9 billion, a YoY growth rate of 5.3%, exceeding the expected $11.1 billion.

Adjusted EBITDA was $40 million, higher than the market's expected loss of $64 million; earnings per share were 2 cents, exceeding analysts' expected loss per share of 5 cents.

Looking ahead to Q4, the company expects revenue to be between $13.2 billion and $13.8 billion, higher than the market's expected $13.3 billion.

Comparison

PINS has achieved a higher revenue completion rate and higher profit margins. SNAP's revenue may have more dynamic fluctuations.

SNAP's profit level is still lower than that of PINS, but this quarter's EBITDA has returned to positive territory, showing some signs of recovery, but it is uncertain how long it will last.

SNAP's free cash flow continued to flow out in Q2, while PINS' free cash flow has been positive since 2021.

When Q2 performance was announced, both companies stated that they expected Q3 revenue growth to drop to "mid-single digits," but PINS was just being polite while SNAP actually did achieve mid-single digits. This also illustrates the attitudes of both companies' management teams; SNAP's Evans sets some higher goals but does not achieve too many surprises when it comes to implementation.

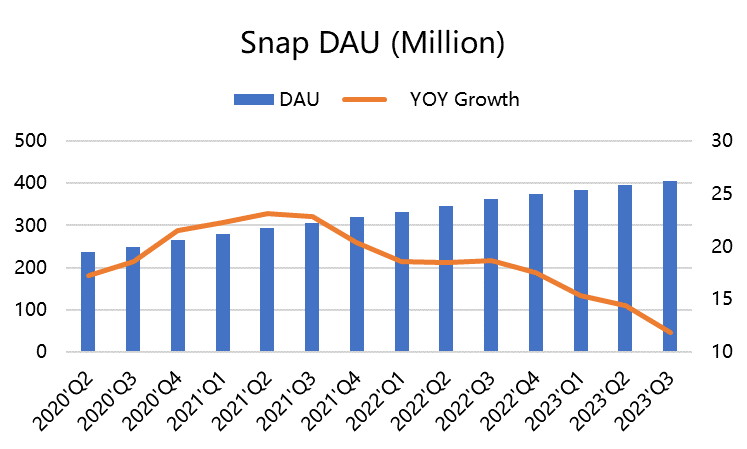

Therefore, Snap hopes that DAUs will reach 475 million by the end of next year, which may be a challenging goal.

Both companies are now at a point where they can improve their performance through business diversification and technological advancements, and both have mentioned integrating AIGC into their own products to enhance the overall ecosystem.

Furthermore, more business models can be developed, especially in gaming, payment, and other areas.

Of course, we should be more cautious about Snap, as it faces various challenges, including but not limited to:

1. Progress with major clients in the United States (a test of competition), needing to prove its ability to expand ad purchases to a broader customer base.

2. Sustained success in its ad product line to drive faster growth.

3. Reducing reliance on Temu and Pinduoduo (PDD), which is very interesting.

Comments