E-commerce companies generally have continuous profitability and decent cash flow, so the valuation of their profit multiples are fair.

Although the market value of $Pinduoduo Inc.(PDD)$ has reached $135 billion, which is twice as high as $JD.com(JD)$ s $42.6 billion, many people think it is expensive.

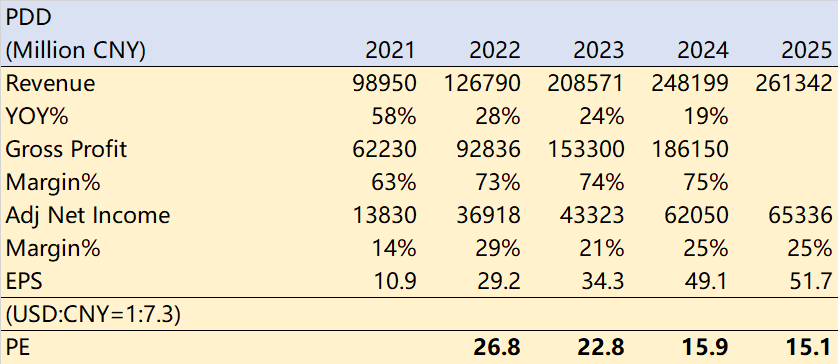

Regarding at PDD's performance and expectations, it cannot be considered "expensive". By estimating its revenue and profit levels based on the current market expectations and then adjusting it with Pinduoduo's better-than-expected performance.

With a closing price of $107.13, the PE ratio based on the EPS for 2023 is 22.8 times, and for 2024 it is 15.9 times.

Many investors may still think that PDD is the company that burned money and suffered losses due to "billions of subsidies".

Speaking of which, let's talk about why JD.com is declining.

Firstly, the macroeconomic is not in its favor. Whether it's "downgrading consumption" or increasing precautionary income, there has been a shift in JD.com's users who were once "not too sensitive to prices" becoming more price-sensitive.

Secondly, JD.com's positioning is incorrect. The emphasis on speed and quality while neglecting cost-effectiveness has allowed Pinduoduo and Douyin's e-commerce platforms to rise, and JD.com has become a "price target" for others, leading to the formation of a fixed impression among consumers.

Thirdly, they have brought this upon themselves. After playing with coupon strategies for over a decade, they have not only wasted time and reduced efficiency but also lost consumer reputation. Now, Pinduoduo and Douyin's live streaming have exposed their shortcomings.

Comments