$Snowflake(SNOW)$ surge 9%+ after earning release on Nov.29th.

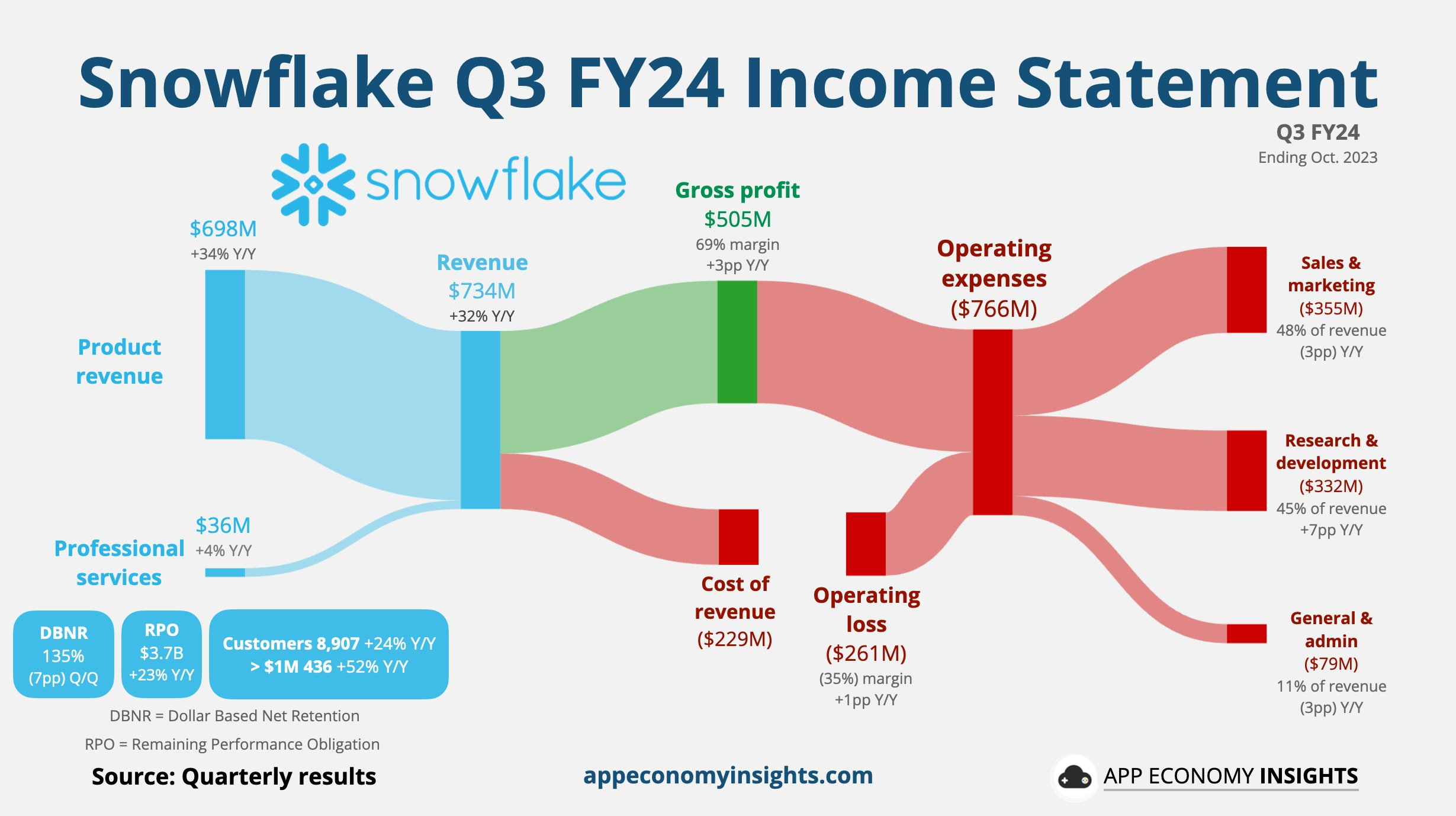

As the leader of a growing cloud service company, its business is also attracting a lot of attention from investors with a high risk preference. Q3 performance exceeded expectations, with revenue of $734.2 million, a year-on-year increase of 35%, higher than the market's expected $675.3 million, mainly due to the unexpected growth in product revenue, and it is also one of the fastest growing companies in the growth sector. At the same time, adjusted earnings per share were $0.25, higher than the expected $0.16.

It is worth noting that the company has begun to turn a profit, with EBITDA increasing from a loss of $31 million a year ago to $185 million. It also led the company's free cash flow to reach a new high of $239 million.

Of course, this also means that in the future, more attention needs to be paid to operational efficiency. Investors will pay attention not only to growth but also to profit margins. This means that these companies have also entered the second half of the competition.

In terms of guidance, product revenue for Q4 is expected to be between $716 million and $721 million, a year-on-year increase of 29% to 30%, and the expected adjusted operating profit margin is about 4%. At the same time, full-year revenue is expected to be $2.65 billion, up from the previous estimate of $2.6 billion, and the full-year adjusted operating profit margin has been raised from 5% to 7%.

Although the growth rate can still maintain at 30%+, the downward trend will still have an impact. The net income retention rate has increased, but the operating profit margin is still relatively low. In addition, competition from Databricks and cloud computing giants is also worth noting.

Comments

The potential is great and the risks are not small, so be cautious.

I really like investing in the cloud computing field, thanks for sharing

SNOW is definitely worth our long-term holdings.

Do you have a target price for SNOW?

Its revenue gave me a big surprise haha