$Nike(NKE)$ plummeted over 11% in after-hours trading on December 21st due to disappointing performance in its FQ2 financial report ending in November.

Weak performance in North America dragged down overall revenue and profit margins, casting a shadow of consumer malaise and causing a loss of confidence among investors.

The company also lowered its guidance for the second half of the fiscal year, with revenue growth of only 1%, lower than the previously indicated mid-point (approximately 4-6%) and below market expectations of 3.8% growth.

Q2 Earnings Review

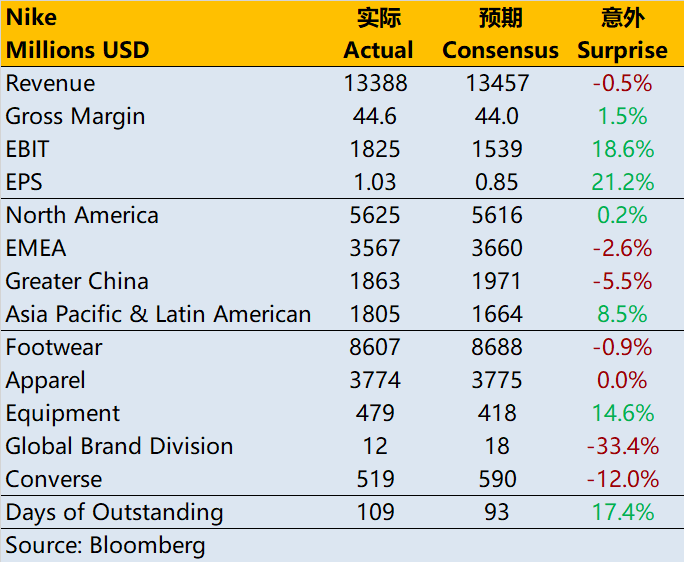

Q2 revenue was $13.39 billion, a mere 1% increase, falling short of the market's expected $13.46 billion. This marks the second consecutive quarter of Nike's revenue falling short of expectations.

Looking at regional performance, revenue in Greater China increased by 4% year-on-year, reaching $1.86 billion, but still below the market's expected $1.97 billion.

In this quarter, revenue in the Asia Pacific and Latin America regions increased by 13%, and in Europe, revenue increased by 2%.

However, revenue in the key North American region declined by 4% to $5.62 billion, mainly dragged down by footwear sales.

In terms of product categories, overall footwear revenue increased by 1% year-on-year to $8.61 billion, below the market's expected $8.69 billion; apparel revenue decreased by 1% to $3.77 billion, below the market's expected $3.78 billion; and equipment revenue increased by 17% to $479 million.

Nike's direct sales increased by 6% year-on-year to $5.7 billion, falling short of the market's expected $5.88 billion, with a currency-neutral basis increase of 4%.

Converse's sales performance was weak in this quarter, with an 11% year-on-year decline, mainly due to weakness in the North American and European markets.

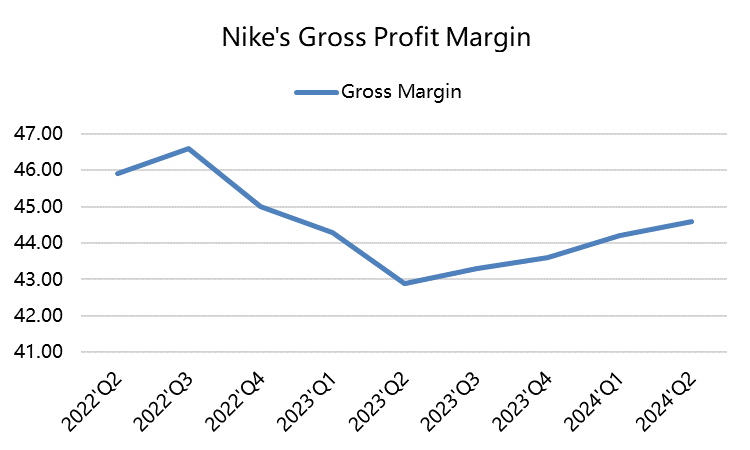

In terms of profitability, the gross margin increased by 140 basis points to 44.6% year-on-year, exceeding the market's expected 43.9%, mainly driven by strategic pricing actions and reduced shipping rates, partially offsetting adverse changes in net currency exchange rates and rising product costs.

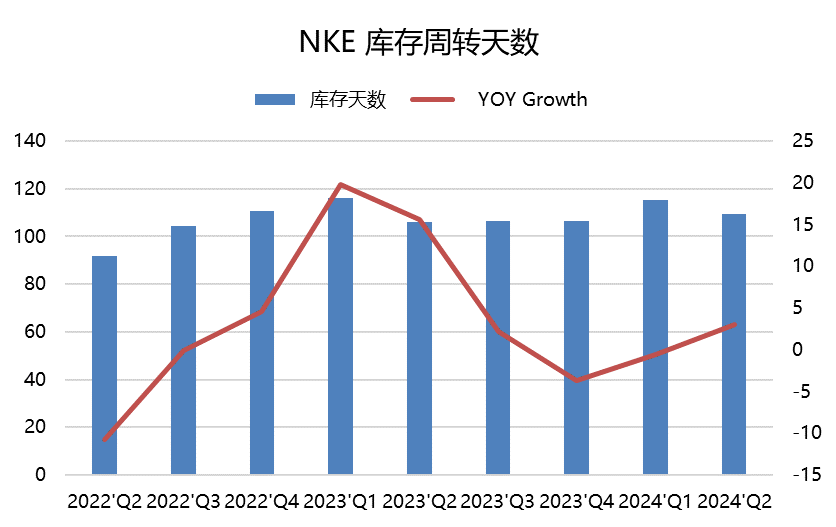

In addition, inventory decreased by 14% year-on-year to reach $8 billion. Cash at the end of the quarter was $9.9 billion, compared to $10.6 billion in the same period last year.

Investment Highlights

1. Weak consumer demand in North America and poor guidance are the main reasons why investors are pessimistic about consumer goods.

2. Shipping costs may rise due to the Red Sea crisis, further affecting sales and costs in Southeast Asia, the Asia-Pacific, and the Middle East in Europe.

3. The company is pushing for cost reforms in hopes of achieving higher profit margins. Although the company intends to achieve cumulative cost savings of up to $2 billion in the next three years, this may still lead investors to question the company's weak growth and lack of competitiveness in the market.

If a company's profit growth is driven by cost reduction, its growth potential is clearly questionable.

4. Comparison with competitors. In contrast, the recently record-breaking $Lululemon Athletica(LULU)$ not only continues to drive online sales in North America, lifting profit margins, but also shows strong growth in product sales in Greater China, and the Asia-Pacific region.

Therefore, even investors interested in investing in sports consumer goods may consider allocating more positions to companies with better prospects.

Pair trades like "Long LULU, Short Nike" may become increasingly popular among investors.

Comments