Last week, we mentioned that one of the important factors supporting the continued rise of the US stock assets in 2024 is the nearly $6 trillion idle cash reserves (cash assets).

Currently, this portion of funds is enjoying a money market yield of over 5%.

If the expectation of a Fed rate cut begins, the short-term benchmark yield of this portion will decrease, and investors may start reallocating this huge amount of funds to other asset categories. The performance of the current interest rate curve indicates that this situation has already begun to emerge.

The change in financial liquidity is also a key force influencing the trend of the US stock market, and may even determine whether the Fed needs to cut rates early. This should not be overlooked, especially since we expect this impact to gradually become evident again in early 2024.

In 2023, the Fed's liquidity tightening corresponded to the volatility in the US stock market.

After the crisis at "Silicon Valley Bank" in March, the Fed "expanded its balance sheet" to release funds, and was forced to "expand its balance sheet" again, providing liquidity to banks through BTFP, while the US stock market was also rebounding after a period of extreme panic.

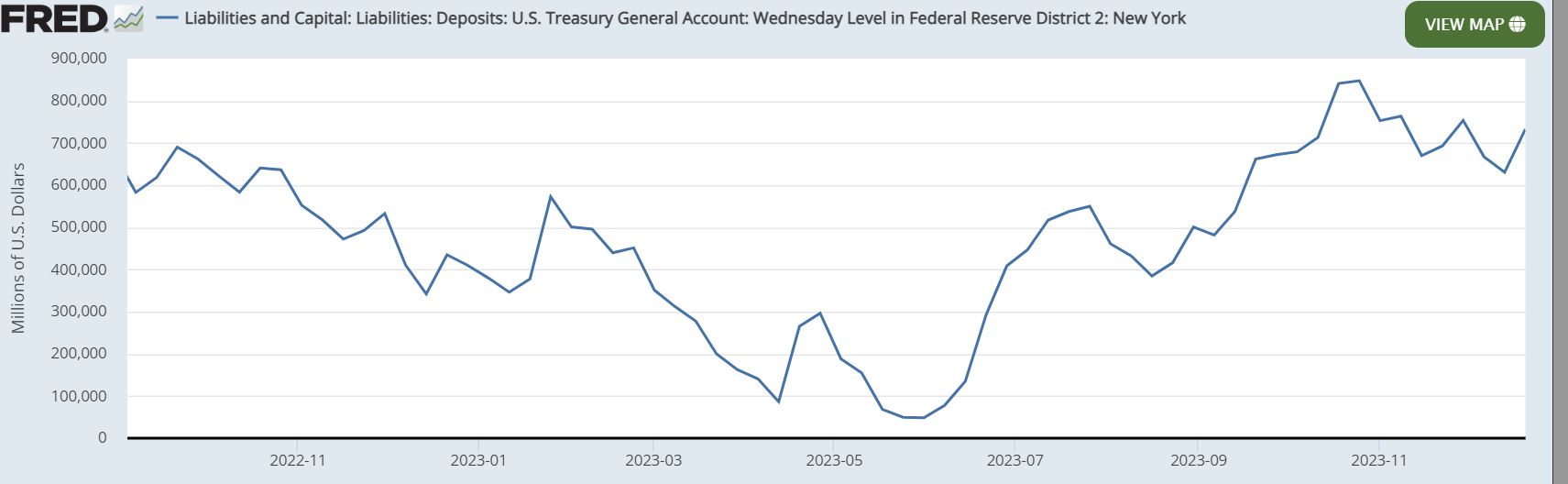

In mid-July, after the US Treasury raised the debt ceiling and continued to issue debt to replenish funds, the TGA increased from less than $250 billion to $700 billion, quickly replenishing funds. At the same time, the Fed continued to shrink its balance sheet at a pace of $600 billion in treasuries and $350 billion in MBS per month, further reducing financial market liquidity, causing the US stock market to peak in mid-July and then fall back.

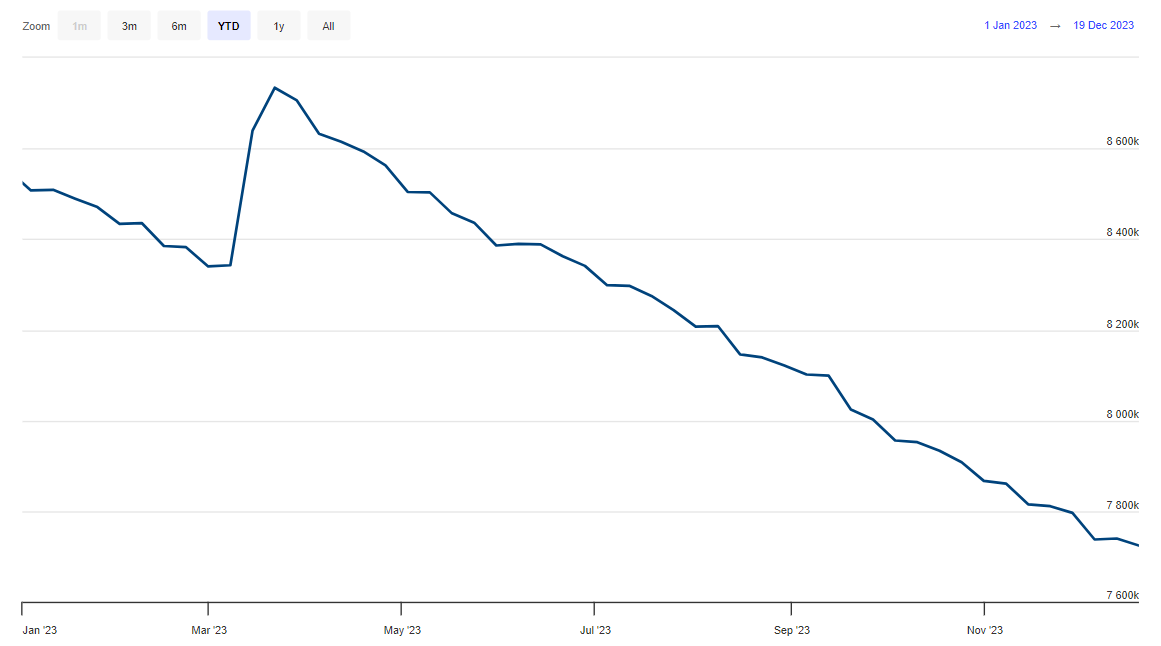

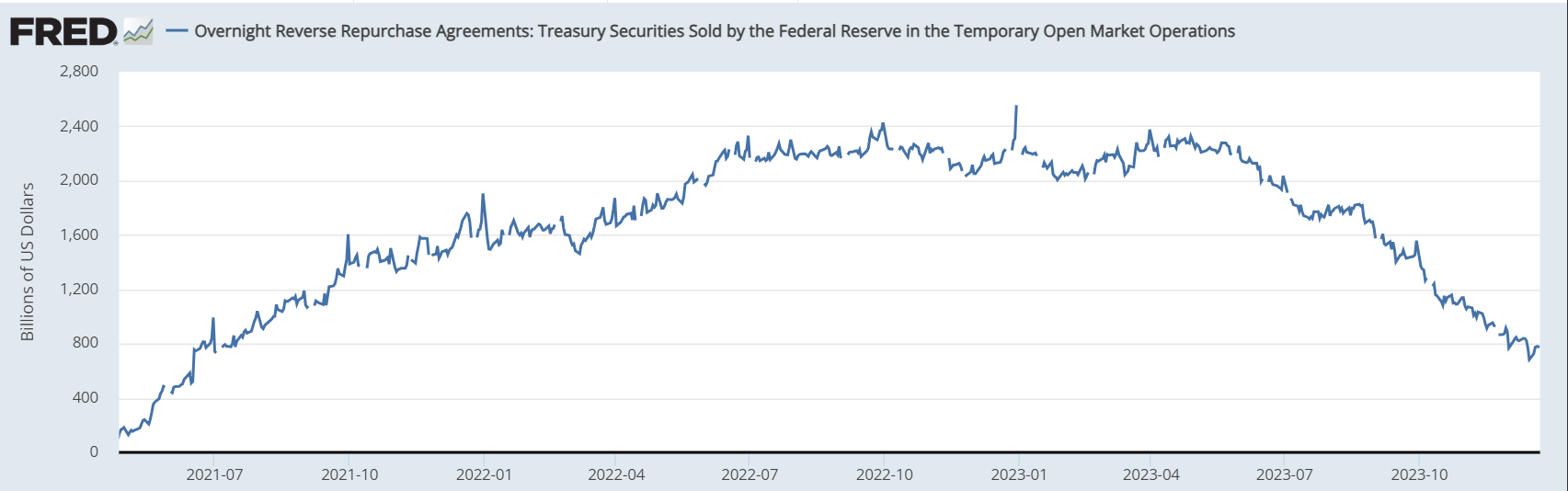

After the October elections, the TGA account replenishment was completed, no longer withdrawing funds, while the Fed's reverse repurchase accelerated release almost completely offset the impact of the simultaneous balance sheet shrinkage. Market liquidity did not decrease but instead increased from $5.5 trillion to $5.9 trillion, so in the case of declining long-term yields, US stocks were able to continue rising.

Taking money market funds as an example, their performance indicator is the seven-day yield. Since the fourth quarter, the expectation of a rate cut has been heating up continuously. For short-term debt, as long as there is no interest rate hike, there will be no significant price pressure. Yields of over 5% are also quite attractive, making money market funds more willing to repurchase US debt.

According to the current trajectory, it is estimated that the balance sheet reduction will resume in the second quarter of next year, leading to liquidity contraction and reserve depletion, which will then exert pressure on the US stock market unless the Fed stops shrinking its balance sheet at that time.

The Fed's previous unexpected turn has been largely digested by the market. Next, the major economic data at the beginning of January and the FOMC meeting may become key validations for rate-cut decisions. From the current statements of Fed officials and the rotation of voting members, there still exists some internal disagreement within the Fed. We recommend that investors closely monitor potential changes.

$Direxion Daily S&P 500 Bull 3X(SPXL)$ $S&P 500(.SPX)$ $SPDR S&P 500 ETF Trust(SPY)$ $Invesco QQQ Trust-ETF(QQQ)$ $Nasdaq100 Bear 3X ETF(SQQQ)$ $Nasdaq100 Bull 3X ETF(TQQQ)$ $Cboe Volatility Index(VIX)$ $iShares Short Treasury Bond ETF(SHV)$ $iShares 0-3 Month Treasury Bond ETF(SGOV)$

Comments