Recently, there has been some volatility in several ongoing M&A (mergers and acquisitions) cases, and the overall market is definitely not the main reason. For cash acquisitions, a general market downturn may actually highlight their attractiveness. The main reason for the volatility is the rejection of the $JetBlue Airways(JBLU)$ acquisition of $Spirit Airlines(SAVE)$ by a judge.

The judge believed that this merger could affect industry pricing and harm the interests of some consumers, and thus it was rejected for antitrust enforcement reasons. This is considered an important victory for antitrust enforcement and may have an impact on future cases.

The affected companies include: Hawaiian Holdings (HA), $Silicon Motion Technology(SIMO)$ $iRobot(IRBT)$ $GAN Limited(GAN)$ Albertsons Companies ( $MiX Telematics(MIXT)$ $U.S. Steel(X)$ Capri Holdings Ltd (CPRI), Cerevel Therapeutics Holdings, Inc. (CERE), and Macy's (M).

I think there are three relatively stable cases at the moment $Macy's(M)$ $Hawaiian(HA)$ $Albertsons Companies, Inc.(ACI)$

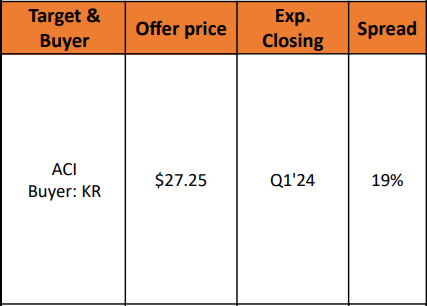

1. ACI

The FTC will hold a closed-door meeting next week, reportedly to discuss either IRBT or ACI. If it's about ACI, there is still a 19% upside potential at the moment, making buying a short-term call option very cost-effective.

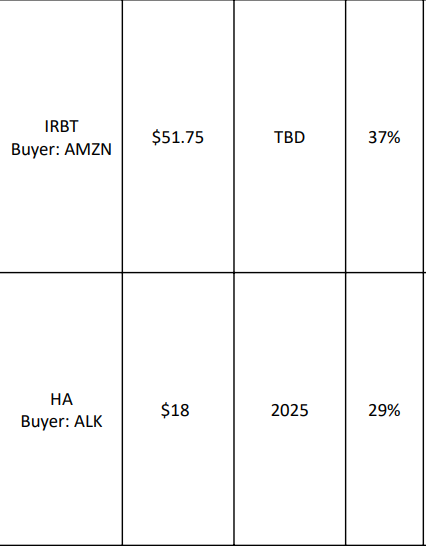

But if it's about iRobot, the company's quality is similar to SAVE, and if it's not acquired, it's basically game over. This is also an important reason why Amazon has not shown much determination to help it out. European regulations are different from those in the United States, with significant influence from various regional laws, and opinions may not be unified, so there are still some variables.

However, with a current acquisition price of 51 and the stock trading at just over 27, there is still a large upside potential, which is also the reason for the very high implied volatility of its options.

Regardless of the outcome, there is a possibility of an IV Crash, so if you are not prepared to accept a one-way outcome, using an options spread strategy may be more prudent.

2. Hawaiian Holdings

It's basically being wrongfully penalized because it doesn't have the same issues as SAVE, and both are not budget airlines. They also have very few overlapping destinations, which makes them highly synergistic. It is expected to pass regulatory scrutiny with little pressure.

Selling PUT options at the current time position is also a good consideration.

3. Macy's

Although the current premium space is not large, the recent decline has created an opportunity.

Generally, when a private equity group proposes privatization, there are basically no issues, and regulation cannot control this. The only uncertainty may be the price and the possibility of an upward surge. Therefore, it is not advisable to sell CALL options.

Selling PUT options is quite stable.

Comments