$ASML Holding NV(ASML)$ Q1 earnings would burden the market?

Let’s see how the report said.

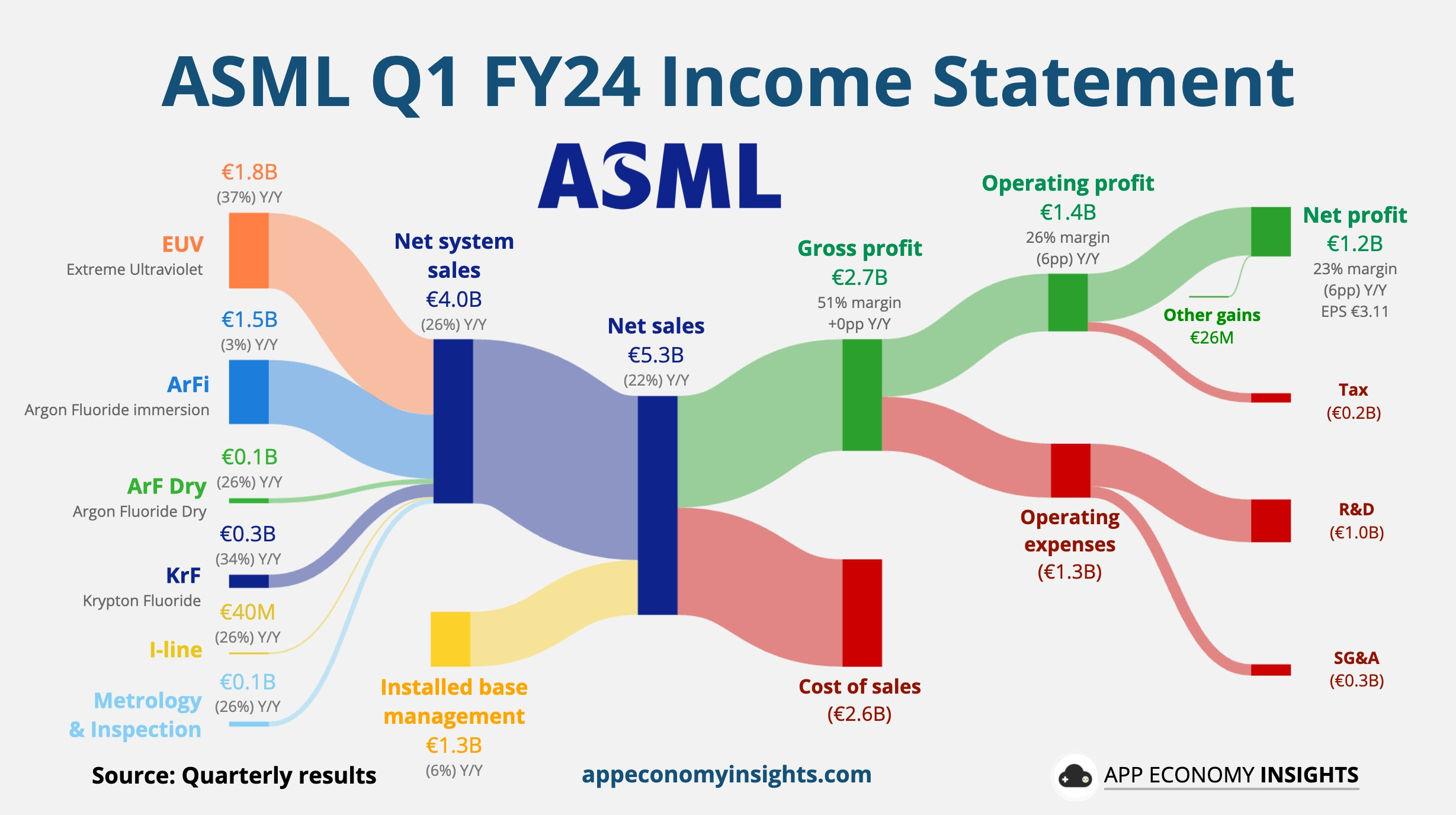

Revenue 5.29 billion euros, a year-on-year decrease of 20.9%, lower than the expected 5.47 billion euros. A

mong them, EUV machine revenue 1.8 billion euros, selling 11 units, slightly exceeding the expected 1.67 billion euros.

GAAP earnings per share were 3.11 euros, higher than the market's expected 2.84 euros.

At the same time, it is expected that the Q2 revenue in 2024 will be between 5.7 and 6.2 billion euros, lower than the market's expected 6.4 billion euros.

Takeaways

Decline in orders is the main reason for miss, but not in EUV orders (est 9 units vs actually 11), shortfall was in the DUV;

Increase in gross margin boots profit margin, consensus 48.8% vs actual 51%, expecting the same level in next few quarters;

Company expects the revenue in 2024 to be comparable to 2023, that is, there will still be year-on-year growth after Q2 to offset the shortcomings of Q1, considering the expansion of $Taiwan Semiconductor Manufacturing(TSM)$ , these targets should not be difficult to achieve;

In the medium to long term, as long as the market supply and demand situation does not change, the profit margin is still easy to maintain, which can further support the valuation even in cases where revenue falls short of expectations.

Will it crash the market?

The night market plummeted 12% after the release of the financial report, but the trading volume during the night market is small and the liquidity is not very good, causing some excessive fear.

An increase in profit margin indicates that the company is still in an industry upturn cycle. Short-term market sentiment is declining, not due to a lack of confidence in the AI business, but only concerns about revenue figures.

Considering that more and more large companies will independently develop chips (reducing the weight of $NVIDIA Corp(NVDA)$ does not mean reducing demand), the mid-term outlook remains positive.

Comments