Investment Highlights

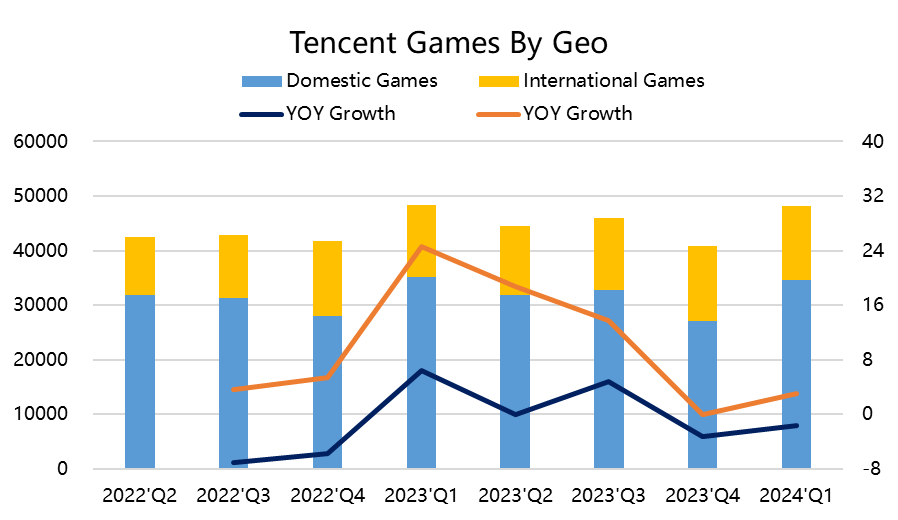

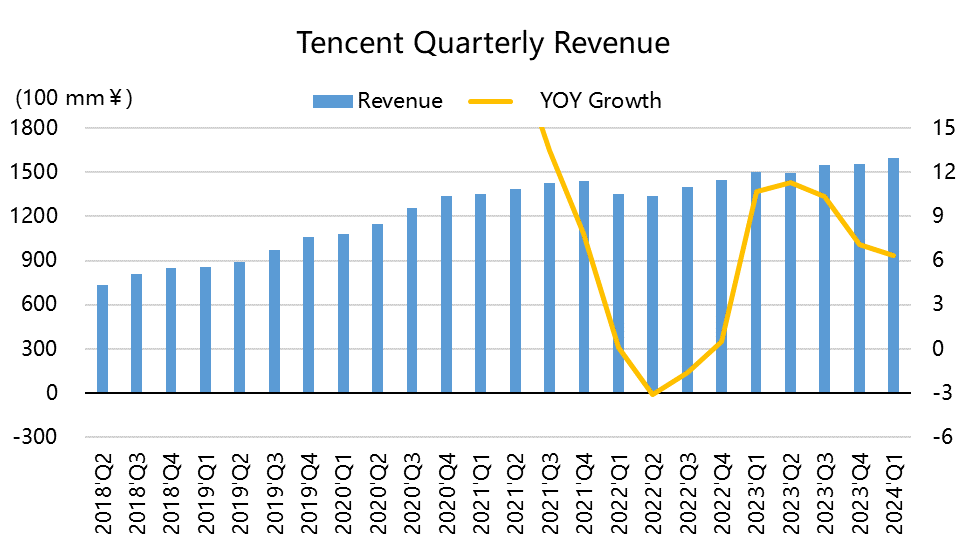

Game business "stops falling" and rebounds, old games revitalized, expectations and water flow hit three-year highs. Overall, compared with the bottom of the last quarter, Q1 game revenue of 48.1 billion, flat year-on-year, or better than market expectations.

Domestic game revenue fell by 2 points, but the water flow began to rebound. The old games "King's Honor" and "Peaceful Elite" instead regained growth because of the new, and "Golden Shovel Shovel", a number of games, exceeded the market expectations in terms of water flow and also hit a new high, which also reflects the industry-wide rebound, as well as the fact that the influence of the old IPs is still important in the absence of explosive hand travel in the industry. In addition, in last year's Q4 was criticized for smashing money in exchange for not being able to market the positioning of the young "yuan dream star", the flow of water may also be in recovery

Overseas performance was even stronger, with an overall year-on-year rise of 3%, a performance that was also realized on the basis of last year's high base. Meanwhile, Supercell's games are rising in volume and have a longer deferral cycle, so this trend could continue for longer, and overall, it could continue to be strong if there are more capable of picking up the baton of explosive titles coming online after Q2.

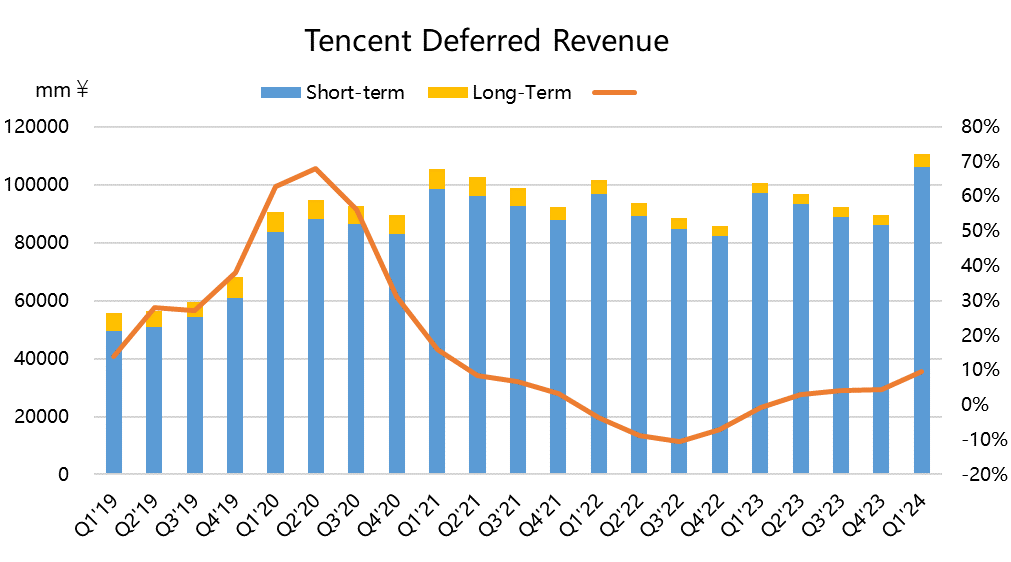

What's more, deferred revenue rose nearly 10% year-on-year and 23% sequentially, also returning to levels seen in early '21, which was achieved before the launch of a breakout hit. Combined with the launch of new games with breakout potential like Dungeons & Dragons: Origins and Call of Duty: Warzone, Tencent could be in for a mini-sunrise of gaming this year.

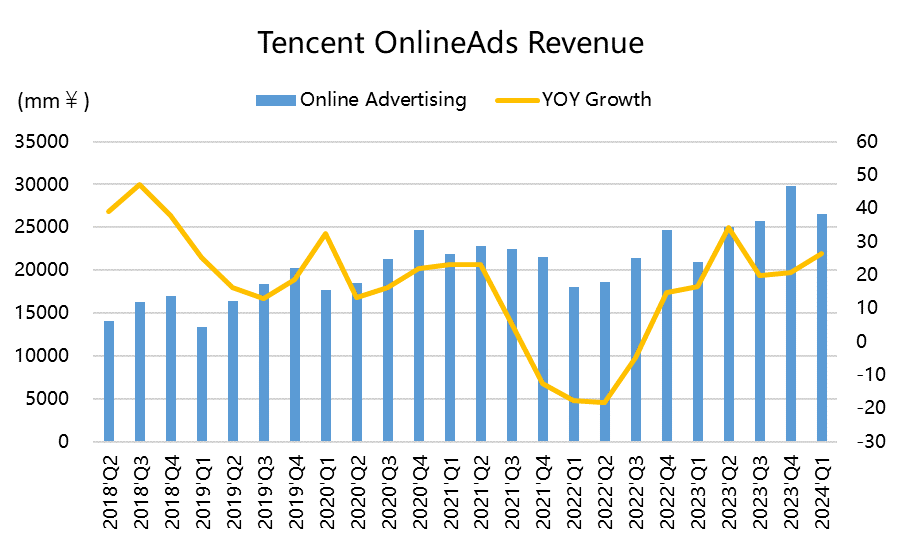

The importance of the WeChat ecosystem continues to grow. Advertising revenue of 26.5 billion yuan, a 26% jump year-on-year. Last year's Q1 growth rate of 16% for some special reasons was also the early stage of recovery, but the base is not low, while this big exceeded expectations is more of the WeChat ecosystem of the video number, small programs, public number, small games and other advertising share. All industries except new energy are growing.

I think the advertising business is picking up due to the following reasons: 1. the rebound of games brought by the new version of the new IP, 2. the involution of the online and offline consumer goods industry, 3. the Internet has survived the most difficult period and is looking for growth again. 4. the improvement of advertising efficiency brought by the use of AI technology.

Social network revenues stabilized, with $Tencent Music(TME)$ embedding in the WeChat ecosystem significantly increasing subscriptions and reaching the previously hard-to-reach middle-aged demographic, as well as generating more advertising revenues; and Tencent Video's paid memberships increased by 8% after new dramas such as "Flourishing Flowers" exploded in popularity

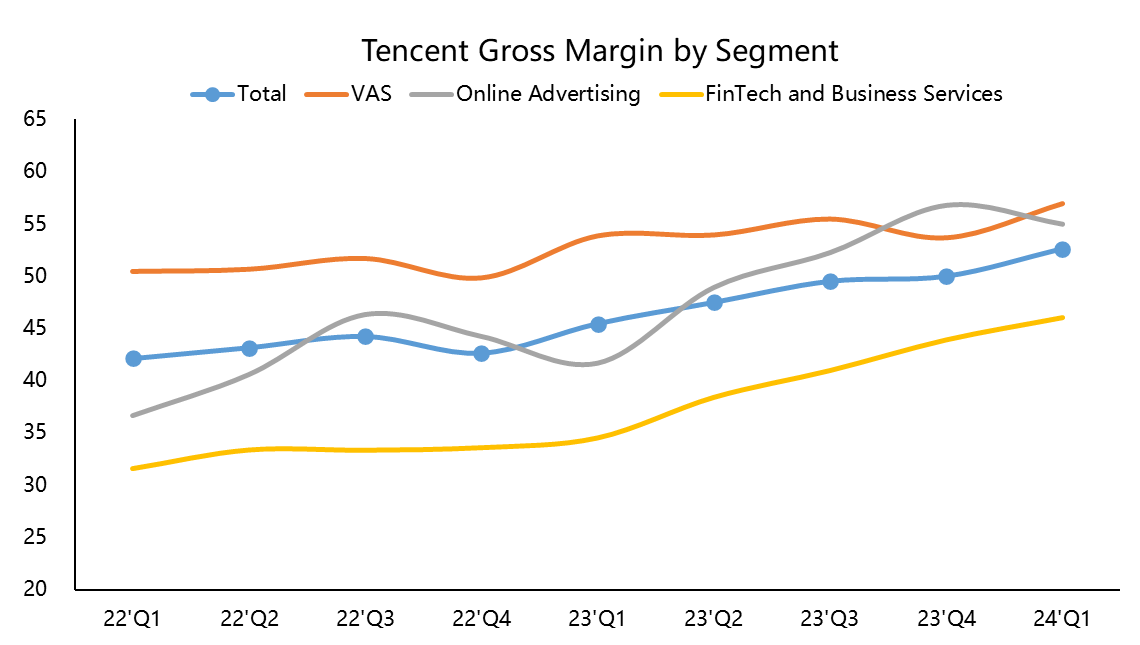

Fintech business is not bright in the east, and enterprise service focuses on efficiency improvement. While Q1 offline commercialization activities are not strong overall, resulting in consumption impairment, micro-credit withdrawals and other revenues are also reduced, but at the same time the financial income has increased significantly. And enterprise services including cloud business, video number merchant growth also benefited greatly. The reduction of low-margin subcontracting business in cloud services also further optimized server costs, resulting in a 12 percentage point year-on-year improvement in gross margin to 46% for the entire segment.

Gross profit margin hit a new high, marketing cost control to improve overall profitability. Cost reduction and efficiency enhancement is actually still ongoing, in addition to the initiative to tilt resources to higher margin businesses and reduce some low-cost businesses at the business level, as well as no amortization caused by large capital expenditures in Q1, thus the gross profit margin reached a new high of 52.6%. On the other hand, the three major expense ratios continued to contract, for example, Q1 caused a large amount of marketing expenses due to the promotion of Yuan Dream Star, which accounted for more than 24%, also contracted back to 20% in Q2. Overall operating profit was 52.6 billion yuan, with a profit margin of 33%.

Valuation basis further improved. Final Q1 realized Non-IFRS net profit of 50.27 billion yuan, up 54% year-on-year, due to the market expectations began to be more conservative, and the recent part has begun to improve, but this result is still greatly exceeded market expectations. Valuation is also further supported. Taking the closing price of HK$381.5 on May 14, the

If the adjusted EPS, valuation TTM PE's from the 20 times significantly slipped to 18 times.

In case of EBITDA, the valuation also slipped from 15.4x to 14.5x.

Shareholder $Naspers Ltd.(NPSNY)$ Reductions Continue, But Begin to Shrink Prosus' official website disclosed that it still held about 2.3 billion shares of Tencent as of May 3, with the latest position accounting for 24.39% of the total, and is currently reducing its holdings in the amount of about 2 million shares a week, accounting for 2% of the trading volume.

After previously announcing increased dividends and buybacks (HK$1 billion per day), Tencent's stock price is going to in theface of such a stellar earnings report?

$TENCENT(00700)$ $Tencent Holding Ltd.(TCEHY)$

Comments