In recent quarters, the $Meta Platforms (META)$ earnings market has been exaggerated, with swings of 10% up and down not uncommon, which means that relatively muted trader sentiment on weekdays is amplified on the day of the earnings report, making market expectations versus actual landings important.

After the 24Q2 earnings report was announced after the bell on July 31, META rose more than 7%.While the range was not low, it was still less than the implied volatility of the options (10%+), and given the rally in the broader market on that day, the overall sentiment was relatively upbeat and the volatility from the earnings report was relatively lower.

This is because Q2, while the overall results exceeded expectations, guidance is also relatively solid, and capital expenditures were not as upwardly revised as in Q1 to panic the market, thus also leading to the return of some of the previously outflowing funds.

Key investment points

Expectations not too high, guidance not too low, capex not a shock.

The company's revenue was $39.1 billion, up 22% year-over-year, mainly driven by advertising, and profits were both higher than expected, with net income of $13.5 billion, up 77% year-over-year, and EPS of $5.16, reflecting strong profitability and an indication that the main business didn't disappoint the market.Meanwhile, capex of $8.47 billion in the quarter was smaller than the consensus estimate of $9.45 billion, meaning that the pie was painted large and the actual investment was smaller than expected, and there was no further upward revision to the upper end of the range for full-year capex (only the lower end was raised slightly), although capex for 2025 was raised slightly.

What are the strengths of the advertising business?

META's biggest advantage is the high stickiness of social media users, and at the same time, it has the largest volume among all social media platforms, which in turn generates an extremely strong scale effect.

Advertising is very responsive to the macro environment, especially in the consumer goods industry.There are two big sources of advertising this year

One is e-commerce, including must-inputs to Temu, Shein, and other cross-border e-commerce players, who are extremely ROI-sensitive and will reconsider placement priorities once conversions on their platforms drop.Obviously there is still a difference between Google's search ads and ads on short-form video platforms like YouTube and Tiktok, and the conversion rates of social media platforms.

The other is election year advertising, in fact, this aspect of Facebook can not be dominated at first, but with X.com's Elon Musk after the clear support of Trump, Harris supporters are likely to switch more to other platforms, will also bring a certain amount of volume.

But overall, as the CPI declines and consumer spending (especially among low- and middle-income families) tightens, advertisers will continue to be cautious about the effectiveness of their placements to a certain extent, and the reaction to that will be a demand for greater efficiency in ad spending.Although Facebook Family has certain advantages, but the change of the general environment will make META sooner or later encounter advertisers to shrink the situation of spending.

Capital expenditures of the "expected"

Big Tech's capex has become the "AI ID", and while more and more investors are skeptical that these investments will yield equivalent returns, META confirms that it expects it to be in the range of $37-$40 billion, compared to its previous estimate of $35-$40 billion.Considering that Q2 actual spending was weaker than expected, the lower end of the range is more important.Of course, the market has already expected "high AI capex", plus $ Microsoft (MSFT) $ and $ Google A (GOOGL) $ and other companies have clearly demonstrated the determination of "must invest".The determination of "must invest".

At the same time, the full-year total expenses are expected to be 96 billion to 99 billion U.S. dollars, the same as the previous guidance, also indicates that the previous "cost reduction and efficiency" initiatives have been completed, it seems to be more into the cycle.

VR products are still waiting for the cycle, the loss is expected.

Reality Lab's revenue of $353 million, an increase of nearly 28% year-on-year, but below market expectations of $371 million.Operating loss of $4.49 billion, slightly better than market expectations of $4.53 Due to the relatively low share of the current VR industry as a whole still need to wait for more mature products to spread the developer ecosystem, $ Apple (AAPL)$ 's Vision Pro of the multiple regions of the market may bring the company also have some impact, may be able to bring a certain amount of stimulus, butIt's too early for it to become a phenomenal product.Therefore it is more realistic for the VR business to aim for loss reduction in the short term.

Expectations for existing valuations?

In terms of profit multiples, META is relatively the lowest of the Magnificent 7 at the moment, with a short-term dynamic P/E of 24x on a closing basis, or 26x on an after-hours basis at 508.87.Based on 2024 consensus estimates, the 2024 PE is around 24x, and based on current margin growth expectations (15-18%), the 2025 equivalent should be around 22.5x.

Performance Data

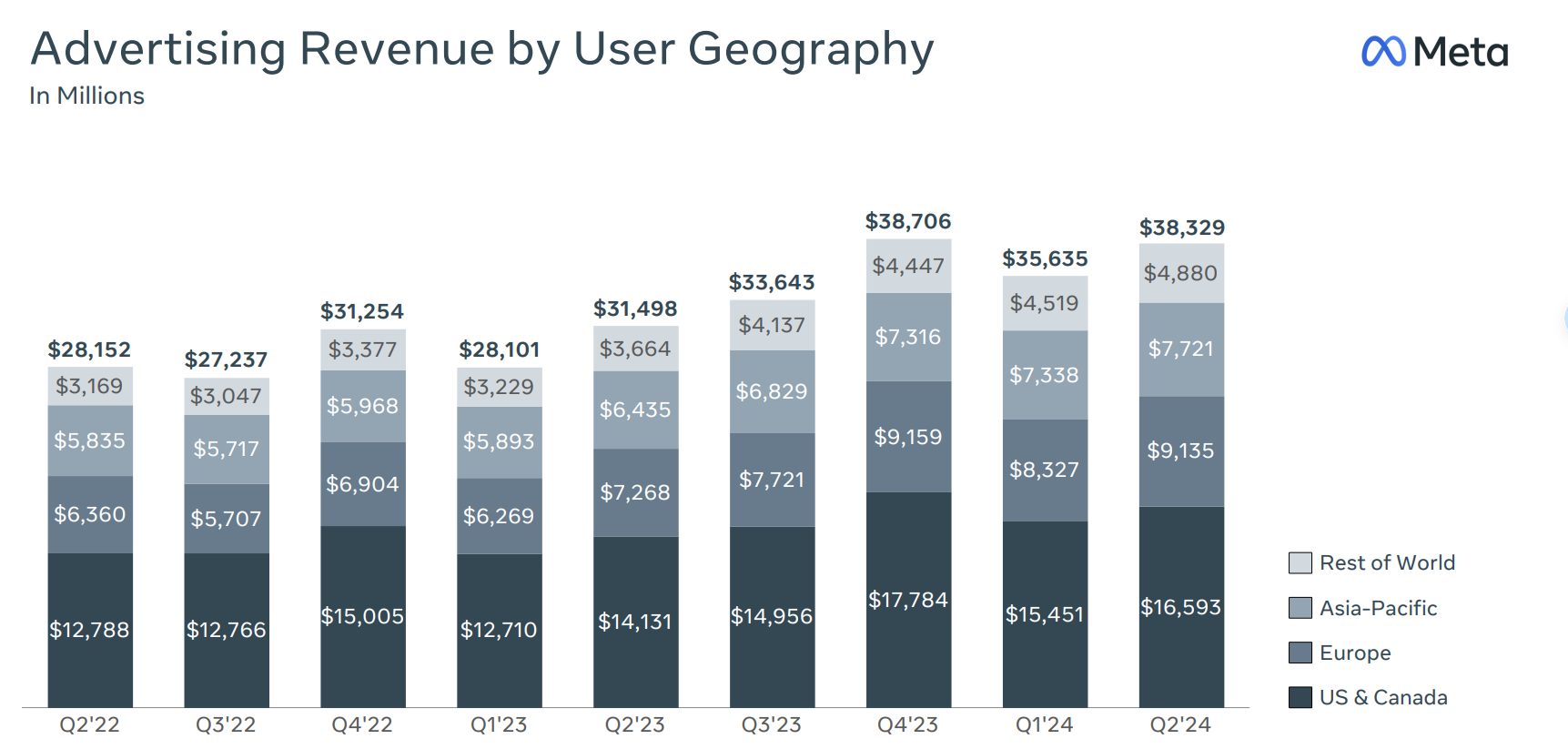

Revenue: Meta reported total revenue of $39.1 billion, up 22% year-over-year.This growth was primarily driven by the Advertising segment, which contributed $38.3 billion, also up 22 percent from the prior year.

Expenses: Total expenses for the quarter were $24.2 billion, an increase of 7 percent from the prior year.The increase was primarily due to higher infrastructure and Reality Labs inventory costs.

Net Income: Net income for the second quarter of 2024 was $13.5 billion, or $5.16 per share, reflecting strong profitability.

Capital Expenditures: Meta's capital expenditures were $8.5 billion, primarily investing in servers, data centers and network infrastructure.

Free Cash Flow: The company generated $10.9 billion in free cash flow and repurchased $6.3 billion of Class A common stock.

Advertising

The Advertising segment remains the cornerstone of Meta's revenue model.Advertising revenue was $38.3 billion, an increase of 22 percent year-over-year, driven by increased demand across verticals, with online commerce being the largest contributor, followed by gaming, entertainment and media.

Geographic Performance: The Rest of the World and Europe saw the strongest growth in ad revenue with 33% and 26% growth, respectively.Asia Pacific grew 20% and North America grew 17%.Advertiser Geographies:Asia Pacific led the way with 28 percent growth, with a high base effect of Chinese advertisers, which was down from 41 percent growth in the first quarter.

Ad Shows and Pricing: The total number of ad shows served increased by 10%, driven by growth in Asia Pacific and the Rest of the World.Average price per ad: Average price per ad also increased by 10%, indicating increased demand from advertisers and improved ad targeting capabilities. Strategic focus on AI and infrastructure.

AI Progress

Meta continues to invest heavily in Artificial Intelligence (AI) and infrastructure to enhance its advertising capabilities and overall platform performance : AI INVESTMENT : CEO Mark Zuckerberg has emphasized the importance of AI in improving ad targeting and content recommendations on Facebook and Instagram.

The company is developing more advanced AI models such as Llama 3 and the upcoming Llama 4 to remain competitive in the AI space. Operational Efficiency: Despite significant investments, Meta is committed to operational efficiency and aims to optimize its infrastructure to support future AI development.

Comments