$Sea Ltd(SE)$ released its Q2 2024 earnings report on August 13, 2024, and shares jumped 11% after the report and nearly doubled year-to-date earnings.Reacting to the market's optimism about this earnings report.

We believe there are 3 main factors

The e-commerce business has entered a healthy competitive situation with improved guidance and is expected to turn around in Q3 (EBITDA)

Gaming weathered the toughest downturn cycle, active players as well as paying players rebounded;

Strong growth in financial business with increased margin contribution.

Q2 Review

Revenue for the group as a whole was US$3.81 billion, up 23% year-on-year, above the market consensus estimate of 20%, and essentially flat on a sequential basis.

Gross margin of 41.6% was slightly below market expectations of 43.2% and overall operating profit of $83 million was slightly below market expectations of $131 million.Adjusted EBITDA was $448 million.

From the board:

Shopee

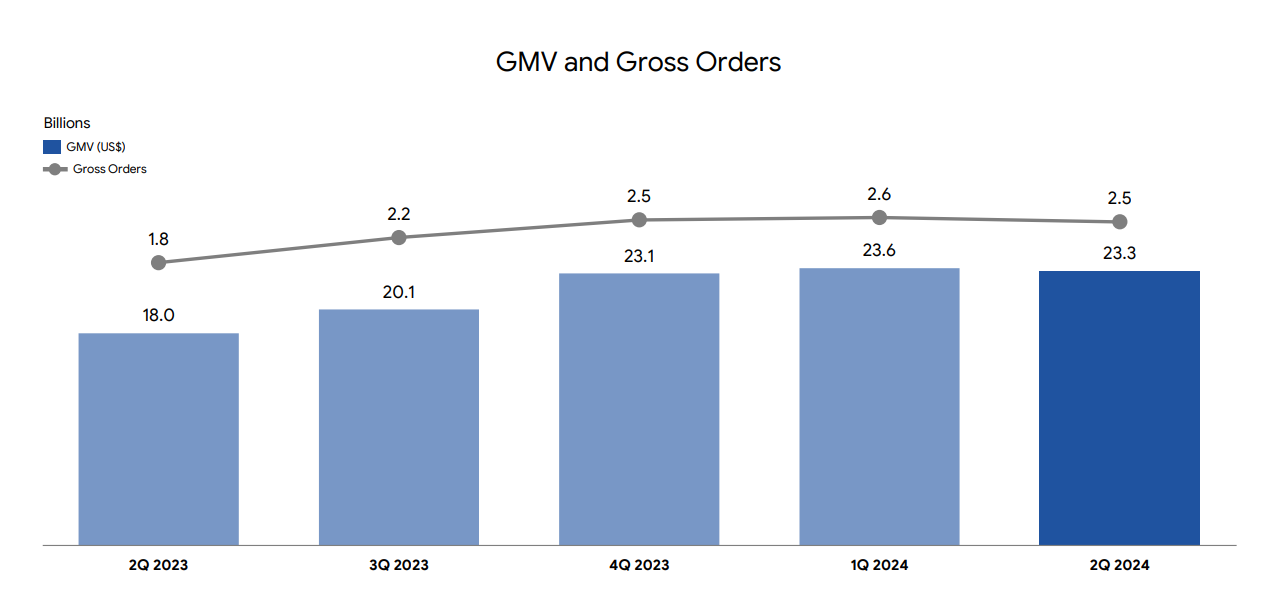

Shopee shined in the second quarter of 2024, with overall GMV growing 29% year-on-year to $23.3 billion, with orders reaching 2.5 billion, and revenues growing 34% to $2.82 billion, thanks to continued growth in the Southeast Asian e-commerce market.The realization rate of the platform business increased to 12.1%, which also led to a significant revenue growth rate.

Meanwhile, Shopee also made promising progress in terms of the number of users and active sellers.The number of active buyers grew 15.1% year-over-year to 159 million.The number of active sellers grew 24.1% year-on-year to 11 million, indicating that Shopee's ecosystem is still expanding.

Gross margins declined, however, to 24.5% from 27.2% a year ago, reflecting higher logistics costs on one hand, and increased spending on promotions and coupons amid intense competition on the other.

Garena

Garena's performance in Q2 was relatively weak, with gaming revenue falling 3.2% year-on-year to $430 million, below market expectations, mainly due to the impact of changes in deferred revenue, and adjusted gaming revenue up 16% year-on-year.The number of active users, on the other hand, rose 19% year-on-year to 648 million, and also increased by 53.3 million sequentially, a positive trend that proves that the gaming business has weathered the downturn and is starting to pick up.

Game streams continued to grow 5% YoY to $540 million in the quarter.Adjusted EBITDA margins remained high at 55.8%, thanks to its high-margin gaming business model.

SeaMoney

SeaMoney performed well in Q2 2024, with total gross payments growing 34.2% year-on-year to $8.1 billion[1].The number of paid users grew 26.7% year-on-year to 11 million, with rapid growth in the Southeast Asian digital payments market.

Revenue grew 41.2% year-on-year to $520 million, and gross margins also improved to 51.7% from 48.2% a year ago, with profitability on the rise.Uncollected loan balances under the new caliber were $3.5 billion in the quarter, up $200 million from the previous quarter, while the bad debt ratio declined to 1.3% from 1.4% in the previous quarter.

Meanwhile, SeaMoney contributed $150 million in operating profit in the quarter, offsetting weakness in Garena.Going forward, Sea Limited will continue to focus on the Southeast Asian market to further strengthen its leadership position in e-commerce, digital entertainment and digital payments.

Investment Highlights

On the e-commerce side, the overall GMV growth rate is still 24%, while the realization rate is high, which is definitely good for revenue and margin improvement, but the wool comes from the sheep's back, and there is still a cap on the revenue that can be obtained from merchants, so if Shopee wants to continue to improve its revenue or margins, it may also have to start with more advertisements and other businesses.Meanwhile, competition with platforms such as Lazada, Tiktok, Shein and Temu, including Amazon, is still fierce, and this competitive situation still needs to be maintained for a period of time, so the realization rate and profit margins have not yet reached an equilibrium state.But the company is still driving the industry towards profitability and sustainability.Management maintained its expectations for Shopee's long-term profitability targets of 2% to 3% of EBITDA.

Entertainment Business, in absolute terms is down, the game cycle decline is inevitable, but this quarter began to return to the user, Garena has also begun to self-developed games to more cooperation in the direction of the agency, from the other hand, can also improve the user stickiness, although it may be a decline in the margins, but for the whole segment of the business is a good thing.

As for the payment business, it is still in an upward growth cycle, and the risk can be controlled, which is expected to further contribute to the Group's profitability in the future.

Guidance and valuation.Sea's share price has been under pressure since the beginning of this year, mainly because of concerns about declining performance and the difficulty of improving losses in the e-commerce business, which are both positive signs at present.Meanwhile, the company has also raised the growth rate of GMV for the full year of 24, and the guidance has been revised upward from 15%-19% to possibly more than 20%.At the same time, Shopee is expected to achieve positive growth in adjusted EBITDA in the third quarter (turnaround), and is also more confident about e-commerce growth in the second half of the year.This is the main reason why the market is giving positive feedback.

Comments