Summary

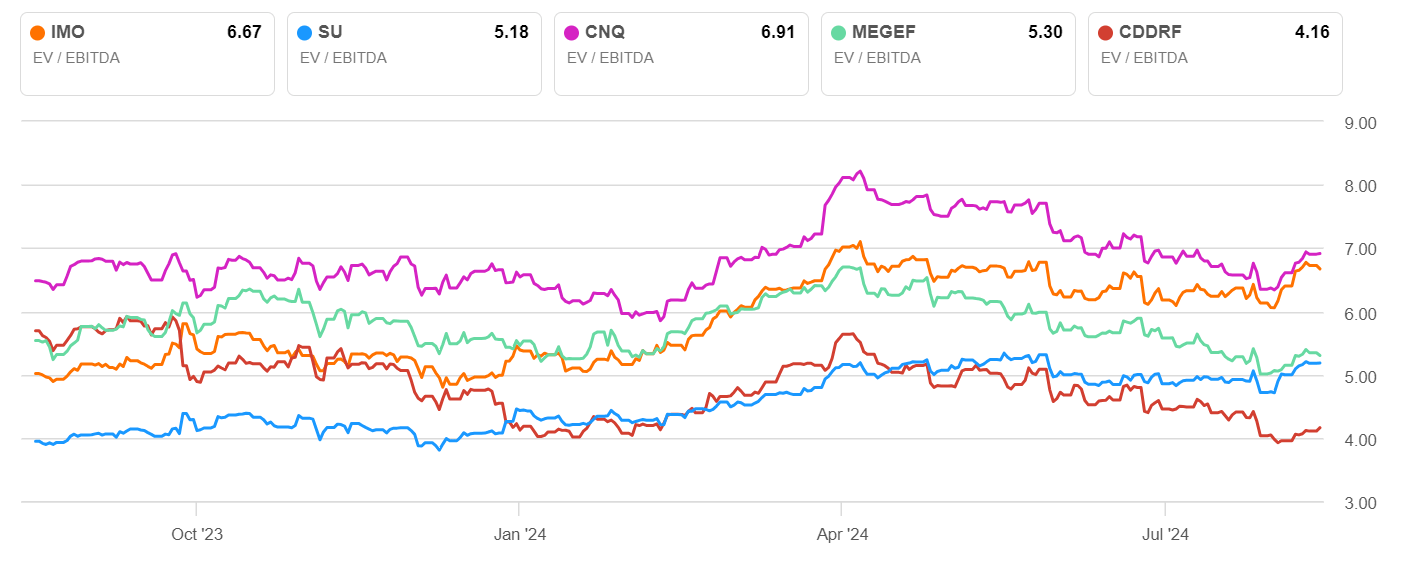

- Canadian Natural Resources and Imperial Oil Limited have outperformed smaller heavy oil cohort members on an EV/EBITDA basis.

- Imperial Oil's stock has seen significant returns, with price targets ranging from the $60s to the $80s.

- The company's production has been meeting or exceeding goals, with potential catalysts in 2025 including new projects and increased output.

- We rate IMO as a hold and think there are better opportunities in the heavy oil cohort. We discuss one briefly in this article.

Now lemme tell ya somethin...about oil sands.

Ugur Karakoc

Introduction

As illustrated by the graphic below, at least two members of the Canadian heavy oil cohort have had a good first half of 2024. I refer to Canadian Natural Resources (CNQ), and the subject of this article, Imperial Oil Limited (NYSE:IMO). On an EV/EBITDA basis they've outperformed smaller members of the heavy oil cohort, including, notably, Suncor (SU), a subject of a past favorable article that recommended SU in the twelve's (now at $40).

We have covered IMO fairly frequently and generally favorably, beginning in 2021 when the stock was in the $27's. The last time was in November of last year, with a buy rating in the upper $50's. Time has been kind to both calls with share price returns of almost 3X, and 50% respectively. Thus, we come before you now with our head held high!

Heavy oil cohort EV/EBITDA (Seeking Alpha)

The professional analyst cadre ranks IMO as a hold at current levels. Price targets range from the middle $60s-$66, to the low $80s-$83, with a median of $73.00. This strongly suggests that the company is nearly fully valued at current levels-at least using this metric, and we may find better opportunities in the smaller players.

IMO beat on EPS estimates $1.55 vs. $1.43 but missed on revenues in Q-2 by -$3.44 bn, thanks to lower prices. EPS estimates are higher for Q-3 at $1.87 which might account for the more bullish price targets in the $80's. Let's see if there are catalysts for IMO that might propel the stock still higher, or failing that, support it at current levels.

The thesis for IMO

The oil sands miners have rebounded nicely since the dark days of COVID-19. Their low decline reservoirs have meant long runways for future production without big M&A campaigns to build drilling inventory, such is common with shale players. The long awaited TMX westward pipeline is here, bringing nearly 600K BOPD of new demand. It is surely the Age of Aquarius for Canadian oil producers. That may be an overstatement of the actual condition in which the heavy oil industry finds itself, but things are better.

Technology is also playing a role as these companies look to minimize fuel costs and boiler intensity in their operations. IMO is keeping pace with the industry with its solvent assisted SAGD operations in Cold Lake and the in-pit tailings reduction project in Kearl. We have previously covered IMO in detail, and new readers are advised to read those older articles for more detail.

Given stagnant oil prices-low $70's to low $80's, much of the rally in the large heavy oil producers in Canada can be attributed to line fill on the TMX beginning, with the associated narrowing of the WCS discount-about $13.00 as of this writing. 600k BOPD of new demand seems to have just been what the doctor ordered for these companies.

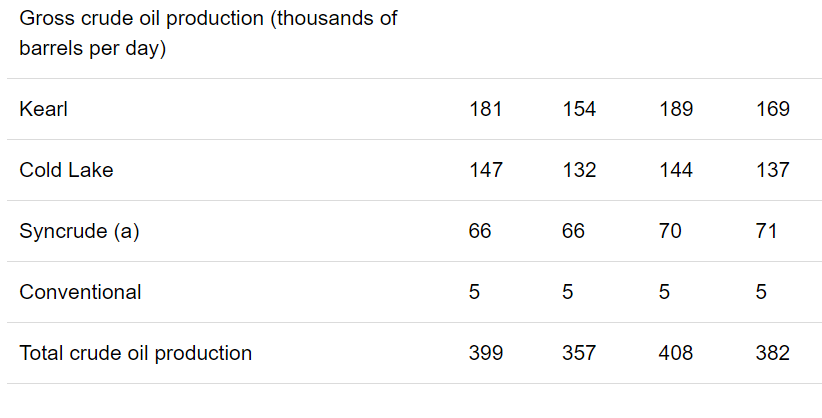

IMO has been meeting or beating output goals at its various upstream production areas. Total upstream production in the second quarter averaged 404,000 gross oil-equivalent barrels per day, the highest second quarter production in over 30 years when adjusting for the divestment of XTO Energy Canada. At Kearl, quarterly total gross production averaged 255,000 barrels per day (181,000 barrels Imperial's share), matching the asset's second quarter production record and achieving record first half production. Kearl also successfully completed its annual turnaround in record time during the quarter. Cash costs have also declined at Kearl about At Cold Lake, quarterly gross production averaged 147,000 barrels per day, including about 3,000 barrels per day from Grand Rapids Phase 1 (GRP1).

The production at GRP1 continues to ramp up, producing about 8,000 gross barrels per day in June, and is expected to achieve 15,000 gross barrels per day at full production rates. This project also lowers unit cash costs and reduces greenhouse gas intensity compared to legacy processes.

IMO didn't issue Q-3 guidance, but CEO Brad Corson put a positive spin on expectations with this comment from the call:

These results were underpinned by strong operations that included the safe and successful execution of several major planned turnaround activities across our integrated portfolio. And while we still have some scheduled turnaround work ahead, we're well positioned for a strong second half of the year.

We can extrapolate output for Q-3 based on past results and comments from the call:

IMO Production (IMO filings)

Organically, the table above shows about a 2% increase YoY. Cold Lake, Grand Rapids Phase I is now currently producing 10,000 barrels to 12,000 barrels per day as July finished up. Only about 3,000 bbls of this was counted for Q-2, so we should see a nice bump for Q-3, another 2-3%. If we add back the 7,000 bbls a day they get from Syncrude Q-3 production, lost during their turnaround, we could show a 5-6% bump from Q-2. Let's call it 420-425 BOPD as an aspirational exit rate.

On the shareholder returns side of things, IMO has recently initiated an NCIB to repurchase up to 5% (+/- 27.5mm shares) of their outstanding shares over the next twelve months beginning on the June announcement date. In the Press Release, they noted a goal of completing this authorization before the end of 2024, mentioning nothing about doing this opportunistically. With the stock at multiyear highs, it's a little difficult to fathom the urgency here, but it should be noted that IMO has reduced their share count since 2017 from 845 mm to present day ~551 mm. So props for consistency. But not perhaps for capital allocation in the last couple of years, as most of the buybacks were made when the stock was in the $30's. So why are we in a rush now?

IMO paid a 2.36% yielding dividend for the quarter.

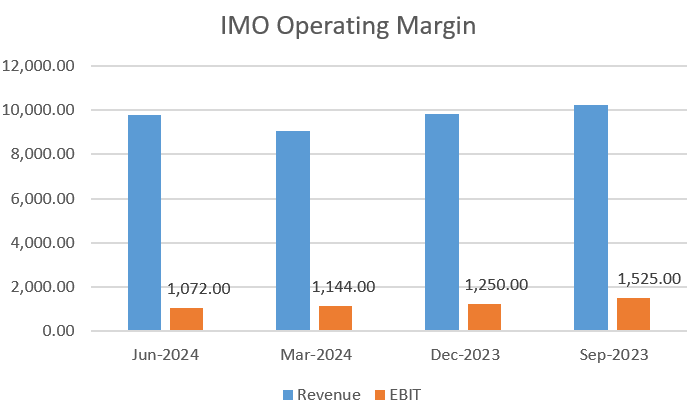

Operating margins have been declining for IMO over the last year. Lower oil prices as the halcyon days of 2022 faded into the drudgery of 2023, reduced output, variances in refining margins, and higher WCS differentials- until recently, are the primary culprits here.

IMO operating margin (Seeking Alpha- chart by author)

Potential catalysts for 2025

Grand Rapids Phase I will extend the life of Cold Lake and lower the costs and carbon footprint of the operations, with another 3,000 BOPD of production, as GRPI hits the full output target of 15K BOPD. Hot on its heels will be the Leming redevelopment, with another 9,000 BOPD targeted in 2025. All in all, IMO could be looking at another 12K BOPD in full year 2025.

The Strathcona renewable diesel refinery will also start up in 2025, putting out 20,000 BD of diesel from local green sources. This will be Canada's largest renewable diesel facility. There is also a new blended products terminal coming to Calgary for renewable diesel blending and offloading distribution terminal, which will further facilitate customers' demands for lower-emission fuels.

Risks

Revenues and margins are highly leveraged to WTI pricing and WCS differentials. WTI has moved toward the lower end of its recent range, and there are new recession related questions about demand for 2025, coupled with burgeoning production from key U.S. basins. All of this could impact the investibility of IMO at current prices.

Your takeaway

Trading at nearly 7X EV/EBITDA and $98K per flowing barrel, Imperial Oil Limited is not at an attractive entry point to new investors. If you are a big proponent of stock buybacks, their ~7% free cash yield-based on their ~$2.0 bn stock buyback plans for the year, is not particularly compelling either. I think a hold is appropriate for IMO at current levels, and would not enter the stock above $60.00 per share. At that point, the catalysts I mentioned would have a greater impact, and in a $75-80 WTI environment, justify the stock's current lofty valuation.

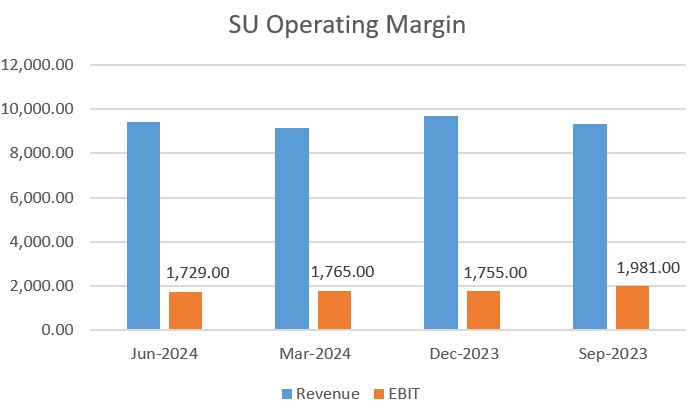

Bottom line, I think new money could be better put to work adding to our position in Suncor. Its lower valuation creates more upside, and as the graph below indicates, is generating nearly double the operating margins of its smaller competitor. SU is trading at 5X EV/EBITDA, and has received upgrades to Outperform from BMO capital based on increased cash flows. Suncor also trades at a 15% free cash yield on a full-year basis, at current prices, and ticking nearly every box on a long term "bargain hunter" investor's checklist.

SU Operating Margin (Seeking Alpha-Chart by author)

Comments