In the early hours of September 19, the Fed announced a 50 basis point rate cut, marking its first reduction since March 2020.

Since 1984, the U.S. has experienced six rate cut cycles:

1984-1986: 26 cuts over 23 months, totaling 562.5 bps.

1989-1992: 24 cuts over 38 months, totaling 681.25 bps.

1995-1998: 7 cuts over 40 months, totaling 125 bps.

2001-2003: 13 cuts over 29 months, totaling 550 bps.

2007-2008: 10 cuts over 14 months, totaling 500 bps.

2019-2020: 5 cuts over 7 months, totaling 225 bps.

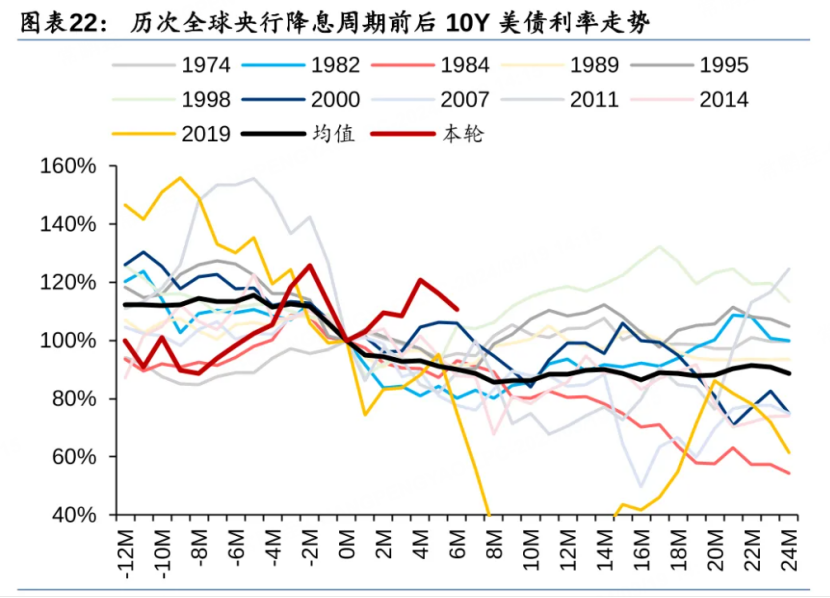

In all six cycles, the 10-year Treasury yield declined. After the rate cut cycle ended, the yield typically rebounded. Here’s how it breaks down:

First Three Months Post-Cut: Anticipation of cuts leads to a notable drop in yields, and the decline was significantly higher than that of other stages, averaging 89 bps.

During the Cut Cycle: In the six rounds of rate cut cycle, the 10Y US bond yield declined by 532bp, 196bp, 118bp, 176bp, 213bp and 117bp respectively, and the cumulative average rate of return declined by 225bp.

Three Months Post-Cut: After the cycle ends, yields bounce back, averaging an increase of 35 bps.

Now that a rate cut cycle is certain, what's the best options strategy for going long on Treasury ETFs like $iShares 20+ Year Treasury Bond ETF(TLT)$ ? The diagonal spread is a solid choice.

What is a Diagonal Spread?

A diagonal spread involves using options with different strike prices and expiration dates. Typically, the long leg lasts longer than the short leg. It can be either a diagonal bull spread or a diagonal bear spread.

Diagonal Bull Spread similar to a standard bull call spread but enhanced. In this strategy, you buy a longer-term call option with a lower strike price and sell a shorter-term call option with a higher strike price. The quantity of bought and sold options remains equal.

This strategy allows you to take advantage of the potential for U.S. Treasury yields to decline while managing risk effectively.

TLT Diagonal Spread Example

Let’s say an investor is bullish on TLT for the next year. They might buy a call option with a strike price of $100, expiring on June 30, 2025. This long leg costs $545 based on the latest market price.

Profit and Loss

Since the short leg can be executed weekly, over the remaining 285 days of the long leg, the investor could sell multiple call options. Successfully collecting premiums from these could significantly lower the initial cost of the long call, potentially making it effectively free.

The diagonal spread offers more than just buying a call outright; it generates additional premium income, reducing the net premium outlay and shifting the breakeven point to the left, enhancing the probability of profit. Additionally, the strike prices for the short legs can be adjusted by the investor, allowing for tailored risk management.

In essence, the diagonal spread is a low-cost strategy for buying call options that investors should definitely explore.

Comments