Big-Tech’s Performance

This week, the broad market consolidated at a high level, due to the rising expectations of Trump's election, the dollar is strong again, and the U.S. bonds downward. 30-year U.S. bond yields once again rose to above 4.5%.But at the same time, the general market did not therefore under pressure, which Trump concept of industries and sectors once led.

Tesla, which announced its earnings this week, was a snowball, exceeding expectations on a number of key indicators such as profit margins, and giving investors hope again on new car expectations, soaring more than 20% on the day, the best in 11 years.

With major big tech companies reporting earnings next week, analysts' focus is sure to include Apple's iPhone 16 sales and commercialisation expectations for AI, MSFT/GOOGL/AMZN's comparative growth rates for cloud services and progress on AI-related capex, MSFT's cooperation with OpenAI, and Google's progress on search ads in the age of AI,META's election year results and the progress of its short video business, among others.

By the close of trading on 25 October, there was a gap in performance for all of the big tech companies so far this week. $Apple(AAPL)$ -0.68%, $NVIDIA Corp(NVDA)$ -0.61%, $Tesla Motors(TSLA)$ +17.92%, $Microsoft(MSFT)$ +1.92%, $Meta Platforms, Inc.(META)$ -1.59%, $Alphabet(GOOG)$ -0.01% and $Amazon.com(AMZN)$ -0.61%.

Big-Tech’s Key Strategy

Might Amazon's surprise not come from the performance itself?

The recent Amazon controversy has come from two main sources:

On the one hand, how much room is there for AWS in MaaS (Model-as-a-service), given the resurgence of enterprise cloud services globally?

On the other hand, how will market share fare as retail sales grow at an increasingly flat rate and come under pressure from more low-priced platform competitors?

In addition, e-commerce may continue to face antitrust lawsuits, including from the FTC and the EU region.

On the bright side, the growth rate of cloud services will continue to grow along with AI big model training, and AWS has a natural first-mover advantage as the platform with the first-highest market share. In addition, the fall in inflation is relatively favourable to retail services, especially the more intense competition from three-way merchants, as the platform may have unexpected benefits.

But on the bad expectations front, the possible lack of sufficient data disclosure on Prime Day sales just past October means that GMV growth may not necessarily be optimistic and could be in the range of 15-20% at most, compared to around 35% reached in the same period last year.Although the overall consumer trend of US retail is not as pessimistic as previously expected by the market, the competition among merchants has gradually intensified, with promotions on online platforms like $Wal-Mart(WMT)$ , a traditional supermarket, becoming the main competition, in addition to the impact of low-priced platforms like $PDD Holdings Inc(PDD)$ s Temu.

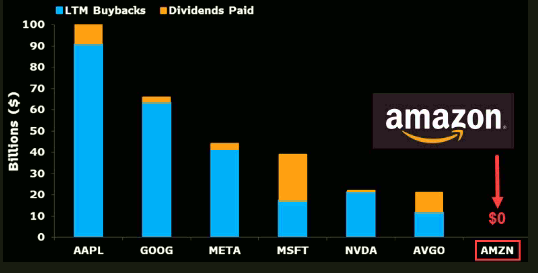

But Amazon's results this quarter may not be the source of surprise, potential buybacks/large dividends are.

Compared to the rest of the Mag6 (Tesla doesn't have a history of large dividends/buybacks), Amazon falls slightly short on shareholder returns.The most recent buyback programme also dates back to March 2022, when a $10bn buyback programme was approved, but only $3.9bn has been bought two years on.

With profits thickening (and margins improving) and the company's free cash flow reaching a record $52.97 billion at the end of Q2, and expected to exceed $62 billion by the end of 2024, it is clear that the capital allocation has become unreasonably "cash-heavy".If the company doesn't have any other bigger capex plans or acquisitions in the pipeline, then a buyback/large dividend would be a good way to give back to shareholders without putting a burden on the company's leverage.

Big-Tech Weekly Options Watcher

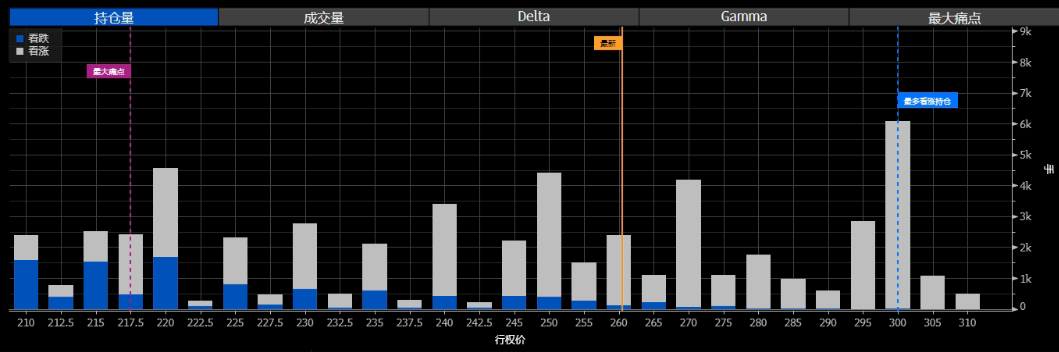

The Tesla earnings report pulled almost the entire market and, looking at the options separately, as the most chalked up positions for Calls due the week of October 25 were in the 230-250 range and the price rose to 260 after the earnings report, that sent the implied shares to be purchased skyrocketing to 2.46 million, well over the usual 200,000-300,000 share range. In other words, there will be an extra 0.1% of the outstanding share capital from Call options alone once this week passes.

As the election is coming up on the 5th of November, Tesla is again a weighted Trump concept stock.Considering that the market is already heavily Price-in Trump's victory, it cannot be ruled out that investors will lower some of their positions or do some hedging.

The biggest variable to look at at the moment is the election, from the largest Call position of 232.5 on the 25th of October, up to 300 on the 8th of November (at the same time, 290 is also a huge amount).This shows that a lot of investors are also banking on the opportunity of this election for TSLA to jump above 300.On the other hand, PUT's open position is very small and the maximum amount is at 217.5, suggesting that many cautious investors do not want to participate in this tail-risky event.

Big-Tech Portfolio

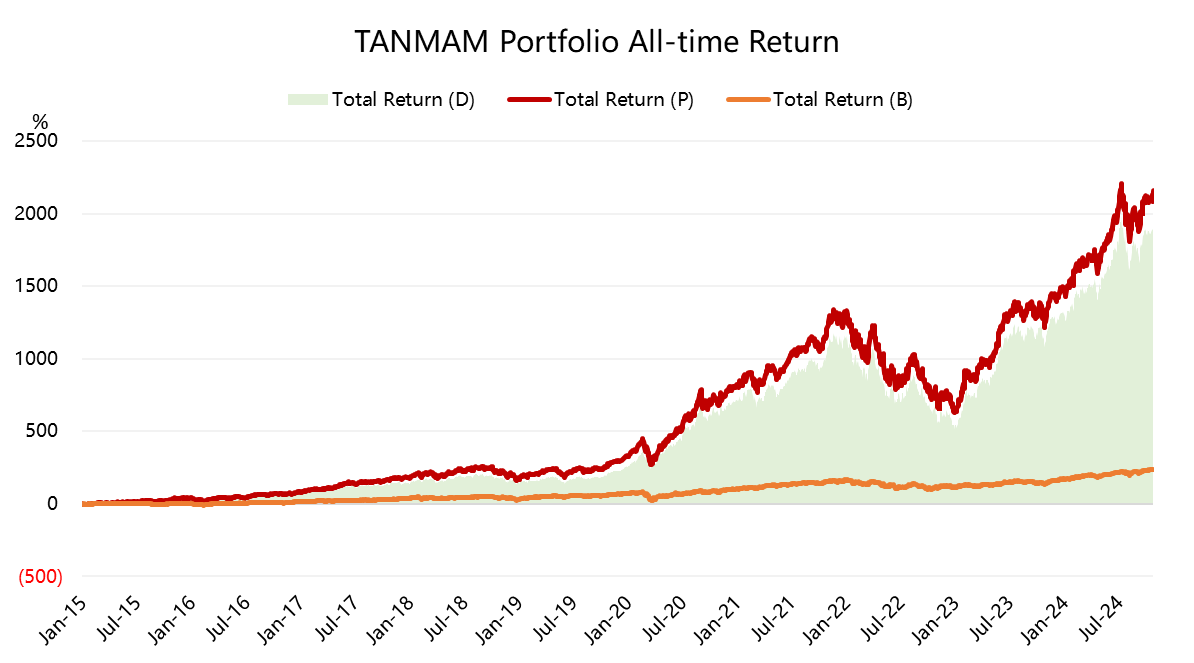

The Magnificent Seven form a portfolio (the "TANMAMG" portfolio) that is equally weighted and reweighted quarterly.The backtesting results are far outperforming the $.SPX(.SPX)$ since 2015, with a total return of 2,161.49%, while the $SPDR S&P 500 ETF Trust(SPY)$ returned 234.62% over the same period, once again pulling ahead, with the excess return rising to 1,926.87%.

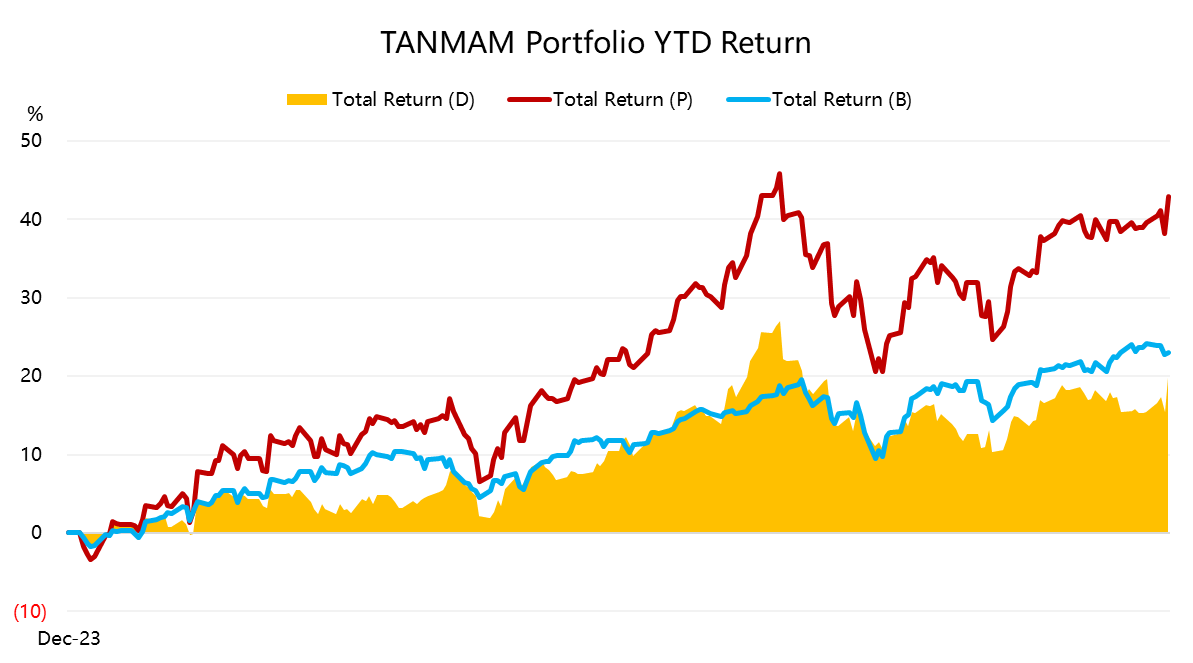

This week big tech rose to 38.97% for the portfolio year-to-date thanks to the strong performance of dangling Tesla, outpacing the SPY's 23.68% and rising the excess return to 19.94%.

The portfolio's Sharpe ratio over the past year has rallied to 2.55, with the SPY at 2.8 and the portfolio's information ratio at 1.25.

Comments