Regardless of earnings reaction, the longer-term trend still appears bullish. Yesterday, a trader was quietly accumulating 20,000 contracts of the $180 strike calls expiring in late 2025 - $AAPL 20251219 180.0 CALL$

Multiple smaller-sized buys allowed this to fly under the radar of conventional large order analysis.

I'm not anticipating a major earnings disappointment from Apple this quarter. Their results tend to be relatively stable. I've taken an aggressive put sale approach into the event:

Sell $AAPL 20241101 230.0 PUT$

$20+ Year Treasury Bond ETF - iShares (TLT)$

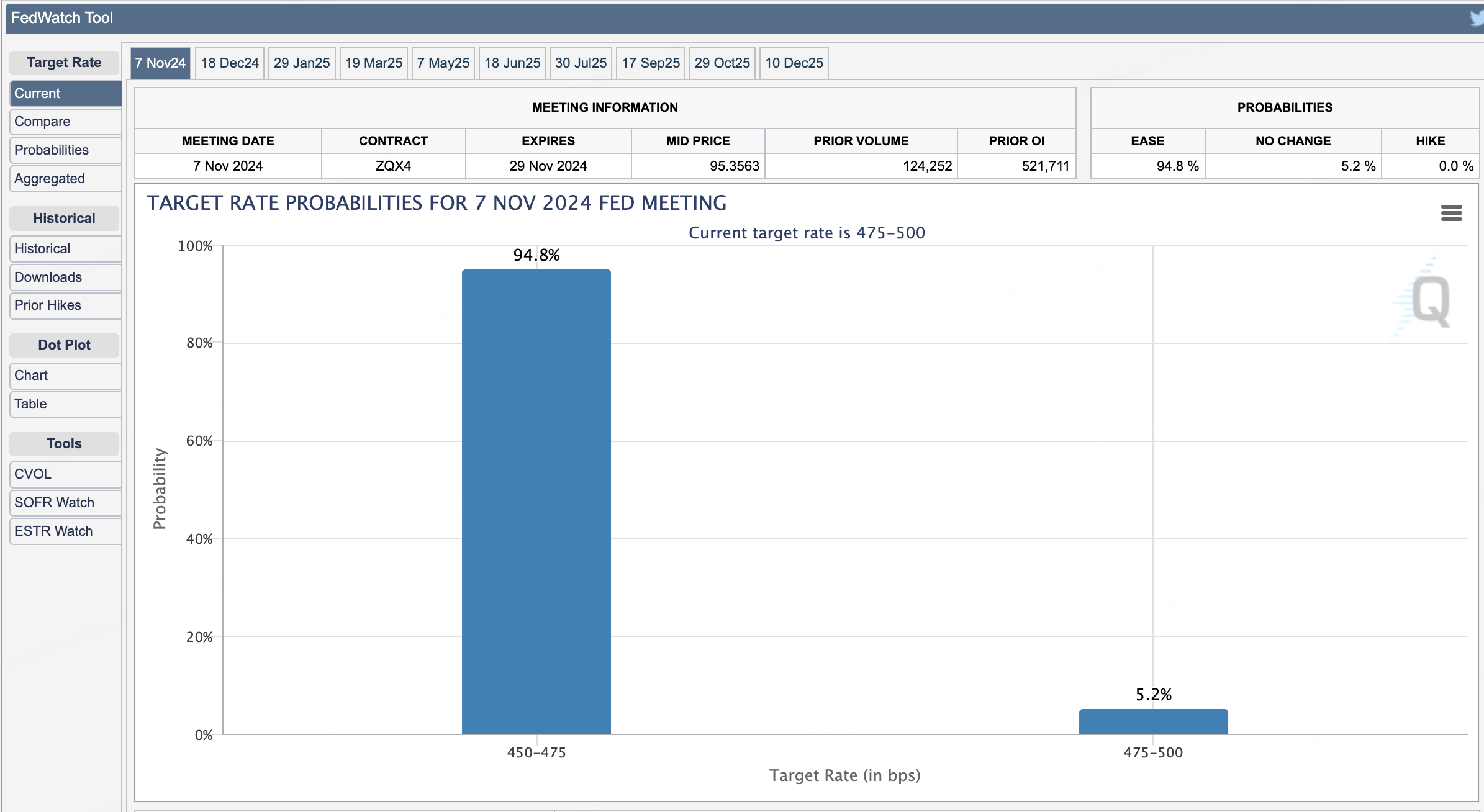

TLT has been in an exceptionally bearish trend recently, to the point where I'm questioning if the FOMC meeting on 11/8 will deliver a rate hike instead of the expected 25bps cut that interest rate markets are pricing in.

Powell places heavy emphasis on transparent communication with markets. He's unlikely to blindside in a direction significantly divergent from current pricing. Ahead of the last 50bps hike, he overtly reset expectations in advance.

While policy errors can occur in either tightening or easing cycles, an unforced disastrous overtightening akin to the BOJ's recent misstep seems unlikely given electoral risks. Powell can't afford carrying that burden into the 2024 elections.

That said, the upcoming FOMC decision may not spark an immediate rally in TLT. Substantial call selling has emerged in the December 6 $92 strikes:

Sell $TLT 20241206 92.0 CALL$ with 53,900 contracts opened

This flow implies TLT is expected to remain below $92 through early December expiration. The $90.5 strikes also saw sizable call selling:

Sell $TLT 20241206 90.5 CALL$

With TLT's lower volatility and higher carrying costs, call selling tends to be a more optimal structure for expressing outright bearish views compared toput buying.

Overall, I continue monitoring developing flows, but the price path appears to favor lower TLT prices into year-end. Cutting losers and redeploying capital into other earnings-related opportunities.

$Trump Media & Technology Group (DJT)$

Based on residual open interest, it appears institutional players were actively getting short last Thursday and Friday. The preceding ramp was likely peak dumb money mania. Not the first time retail has successfully pushed out a larger holder, but with misaligned motivations and disjointed exchange halts, it becomes difficult to maintain a coherent rhythm.

On Monday, new put spread interest emerged looking for downside back towards the $10-$15 range by December expiration. Tough to infer directional bias from the mid-market prints, but both legs signal a low conviction for any further upside:

Buy $DJT 20241220 15.0 PUT$ for 8,344 contracts

Sell $DJT 20241220 10.0 PUT$ for 12,000 contracts

More broadly, both strategies reflect an expectation the party may be over for this squeeze candidate.

Comments