$Lululemon Athletica(LULU)$ The company reported FY2024 Q3 results after the bell on Dec. 5, jumping 10% after the bell.The company's stock has been rebounding since bottoming out in August of this year, and although YTD earnings are still negative, having been over $500 at the end of last year, the company has performed relatively strongly in this year's overall consumer environment, with results exceeding expectations while lifting full-year guidance.

It also increased its share repurchase program by another $1 billion.

Financials and Market Expectations

Overall Financials

Revenue was $2.4 billion, up 8.7% year-on-year, beating market expectations of $2.36 billion;

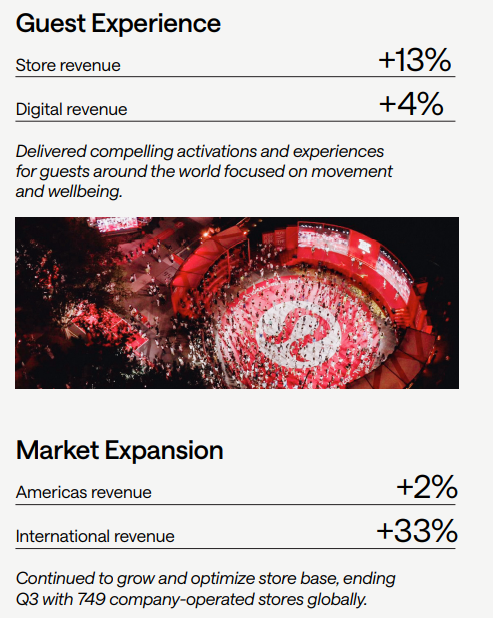

Its Central America region remained Lululemon's largest source of revenue, with revenues reaching $1.77 billion, compared to expectations of $1.74 billion, but the growth rate slowed to just 2%, driven by increased competition and changing consumer preferences in the North American market;

In contrast, international sales grew 25 percent, with sales in China up 34 percent year-over-year, driving overall revenue growth.

Gross margin increased 150 basis points to 58.5 percent, while operating profit margin increased 520 basis points to 20.5 percent.

Diluted EPS was $2.87, up significantly from $2.53 a year ago and ahead of market expectations of $2.71.

Opened 28 new stores in the past quarter, half of which came from the acquisition of the Mexican business

Earnings Outlook

For Q4, the company expects revenue to be between $3.475 billion and $3.510 billion, up 8% to 10% year over year, compared to the market's general expectation of $3.5 billion;

EPS is expected to be in the range of $5.56 to $5.64, compared to market expectations of $5.62.

For 2024, the company expects revenue to be in the range of $10.452 billion to $10.487 billion, up from the market's expectation of $10.43 billion and up from previous guidance of $10.38 billion to $10.48 billion

EPS was raised to $14.08 to $14.16 from initial guidance of $13.95 to $14.15, above market expectations of $14.04.

Earnings Analysis

Lululemon's third quarter results exceeded expectations primarily due to:

Strong international markets: Rapid growth in China and Southeast Asia, in particular, provided strong support for overall results.

New store openings: The Company actively expanded its store network globally, increasing sales channels.

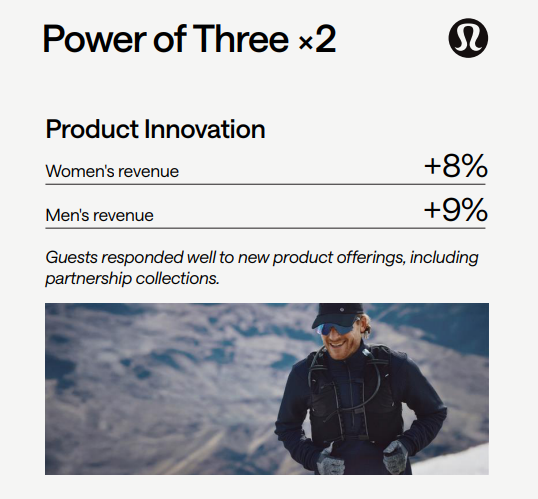

Product innovation and branding activities: Continuous introduction of new products and related branding activities effectively attracted consumers' attention.

Of course, one issue to note is the weak performance of the North American market, especially the sales decline in the women's apparel category, which may affect future results.

Investment highlights

Reasons for Lululemon's success, including

Superior marketing strategy: focusing on a "direct sales" model that maximizes online sales and physical store tie-ins;

Increased social attributes: physical stores are not only a place for sales, but also a social place for consumers to connect with the brand, providing free fitness classes, yoga activities, and community exchanges to increase consumer stickiness and loyalty, leading to stable revenue growth.

The online business is growing rapidly: e-commerce accounts for nearly 30% of total revenue, with a website that offers a convenient shopping experience and personalized recommendation system, as well as successful marketing on social media platforms.In addition, the brand's popularity among young consumers is increased through collaborations with online celebrities and influencers.

Product innovation and technology are also driving its market leadership, such as "Luon" fabrics with excellent stretch and breathability, and the possibility of launching more high-tech materials for sportswear in the future.

Lululemon faces challenges.

On the one hand, it has to compete with strong rivals such as $Nike(NKE)$ $adidas AG(ADDYY)$ $Under Armour(UA)$ and face greater competitive pressure in emerging markets such as China.Under Armour is facing greater competitive pressure in emerging markets such as China $LI NING(02331)$ $ANTA SPORTS(02020)$ and needs to expand its influence and cope with competition from local brands;

On the other hand, it is concerned about the global economic environment and changes in consumer behavior, such as global inflation and central bank interest rate hikes may affect the purchasing power of consumers, even high-end brands may face a decline in consumer demand.

Investor Feedback

Based on the after-hours performance, investors are generally optimistic about the company's international scalability and holiday season sales, so weakness in the Americas is not to be feared, while the company's buybacks will also boost investor confidence.

Throughout Q4, investor expectations for consumer companies are not high, so LULU in North America only 2% increase in the case can also slightly exceed expectations.Coupled with the previous performance of some apparel stocks after the earnings report "right bias", the market's expectations for LULU is also relatively good.

At the same time, the shopping season market investors also have quite strong expectations, so the overall surge is also expected.

Comments

Lulu is popular among young consumers in China.