U1S1, leaving Trump with a mess indeed.

The Root of the Problem: The Triffin Dilemma and Global Imbalances

What is the Triffin Dilemma?The core logic is this:

When a country's currency assumes the dual functions of international reserve currency and domestic currency at the same time, the country is caught in an irreconcilable contradiction.

Short-term demand: The growth of global trade requires the country to provide liquidity through sustained balance of payments deficits (exporting currency);

Long-term paradox: chronic deficits can weaken the credit base of the currency, eventually leading to the collapse of its status as a reserve currency.

What is happening now is

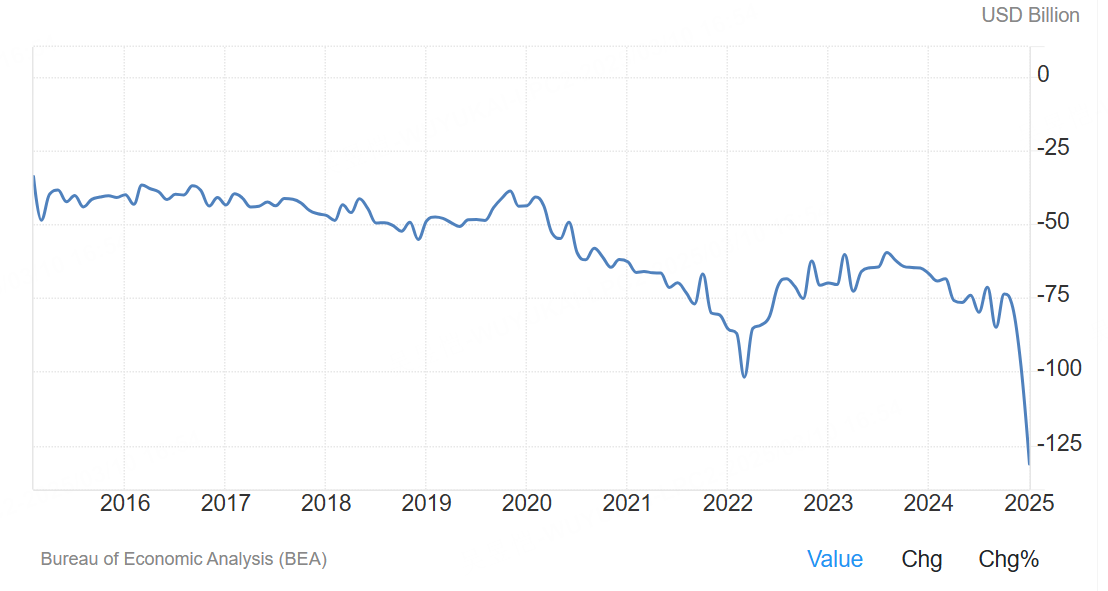

Chronic overvaluation of the dollar: The inelastic demand for the dollar as the global reserve currency has led to its chronic overvaluation, inhibiting U.S. export competitiveness and exacerbating the trade deficit.

The Triffin Dilemma: The U.S. needs to export U.S. dollar assets through persistent trade deficits in order to satisfy global reserve needs, but the burden on the U.S. is becoming increasingly heavy as the global economy expands.

Manufacturing recession: the overvaluation of the dollar has led to the loss of manufacturing jobs (600,000-2 million jobs lost from 2000-2011), with shocks concentrated in specific regions, causing social problems.

First, the core objectives of the agreement and historical positioning

Reconstruction of U.S. economic hegemony: the agreement aims to solve the U.S. long-term trade deficit, debt pressure and hollowing out of the manufacturing industry through comprehensive means, while maintaining the status of the U.S. dollar as the global reserve currency.The core objective is:

Enhance export competitiveness through the devaluation of the dollar and promote the return of manufacturing (re-industrialization);

Restructuring the $36 trillion national debt to ease interest payment pressures, and proposing a "100-year zero-coupon bond replacement" program;

Tying security commitments to economic policies, requiring allies to share military expenditures and accepting U.S.-led trade rules.

The agreement is essentially a prototype for a "new Bretton Woods", i.e., the restructuring of the global financial order through unilateralism.

Main contents and policy tools

Exchange rate intervention and dollar depreciation

- Multilateral/unilateral pressure: Demanding appreciation of trading partner currencies such as the euro, yen, and renminbi, and pushing the dollar's trade-weighted index down through foreign exchange market intervention or policy coordination.

- Inherent contradiction: The Trump administration wants the dollar to depreciate in order to boost exports, but also needs to maintain its international credibility.For example, Treasury Secretary Bessert has publicly stated that "the strong dollar policy has not changed", but White House economic advisor Milan has advocated tariffs as a hedge against inflation caused by the devaluation.

Debt Restructuring and Financial Instrument Innovation

- "Century bond" swap: Proposed swap of foreign holdings of U.S. debt into 100-year non-tradable, zero-coupon bonds; countries that refuse to participate may face tariff sanctions or loss of security.

- U.S. Debt "User Fee" Mechanism: A surcharge on foreign central banks holding U.S. debt, in effect lowering the cost of U.S. financing.

WALL STREET CONCERNS: DoubleLine warns that the move could trigger a sell-off in U.S. debt and hit the global interest rate derivatives market.

Tariffs and Trade Camps

- Differential tariff system: countries are categorized as "allies" and "adversaries," with those that cooperate (e.g., by accepting debt swaps or boosting military spending) enjoying low tariffs, and those that do not facing tariffs up to 60% (e.g., China).60% tariffs (e.g. China).

- Tariff-first strategy: use tariffs on Mexico and the EU as negotiating chips to force trading partners to accept exchange rate harmonization.

Sovereign wealth funds and asset revaluation

- Revalue U.S. gold reserves (8,010 tons) to market value ($42/oz on book → $2,900 on market), adding ~$900 billion in assets;

- Consolidate cryptocurrency reserves such as Bitcoin (207,000) and create a new type of sovereign fund to relieve debt pressure.

Core economic logic and contradictions

Attempts to "deconstruct" the Triffin Dilemma

The agreement tries to mitigate the "overvaluation-deficit" cycle of the dollar as a reserve currency by weakening the dollar, but ignores the impact of the rise of digital currencies (e.g., the expansion of the RMB cross-border payment system, BRICS local-currency settlements) on the dollar's monopoly.

Conflicting policy instruments

- Dollar depreciation and inflation risk: the experience of tariffs pushing up the dollar by 10% in 2018 suggests that, in the current high inflation environment, a weak dollar may exacerbate the rise in the cost of imports, conflicting with the Fed's anti-inflation objective;

- Debt restructuring and market trust: forced replacement of U.S. debt may be regarded as a "disguised default", shaking the status of U.S. debt as a "risk-free asset" and pushing up long-term interest rates.

Geopolitical risks

- Ally countermeasures: EU and Japan's holdings of U.S. debt amounted to $1.1 trillion and $1.2 trillion, respectively, and refusal to swap could trigger a rupture in trans-Atlantic relations;

- Rival countermeasures: China may accelerate the diversification of foreign exchange reserves, 2025 China and Russia's local currency settlement ratio has reached 65%.

IV. Wall Street Investment Banks' Assessment and Market Forecasts

Feasibility Analysis

- Low probability of landing: Citi believes the agreement lacks a basis for multilateral collaboration and faces domestic legal hurdles (e.g., congressional approval);

- Gradual penetration: some provisions are already reflected in existing policies, e.g., NATO military spending raised to 5% of GDP, 301 tariff hike on China.

Market Impact Forecast

- Short-term volatility: if the agreement moves forward, the dollar index may fall below 90, the U.S. technology sector (Nasdaq) will be hit by capital outflows, and commodities and gold will benefit;

- Long-term structural changes: may accelerate the formation of regional currency groups (such as the deepening of the euro area, ASEAN monetary mechanism), and promote the development of central bank digital currencies.

V. Historical Comparison and Implications

Compared to the 1985 Plaza Accord, the agreement presents three major differences:

Unilateralist tendencies: reliance on the threat of tariffs rather than multilateral consultations;

Debt weaponization: directly linking U.S. debt holdings to security guarantees;

Technical debt renegotiation: disguising debt burden reduction through financial engineering rather than relying on economic growth.

Comments