Over the past few weeks, the market has oscillated between "soft landing" and "policy inflection point".Has the tech sector, one of the biggest winners so far this year, reached the end of its valuation expansion?

Interest rates and growth expectations double suppression, TMT volatility rise

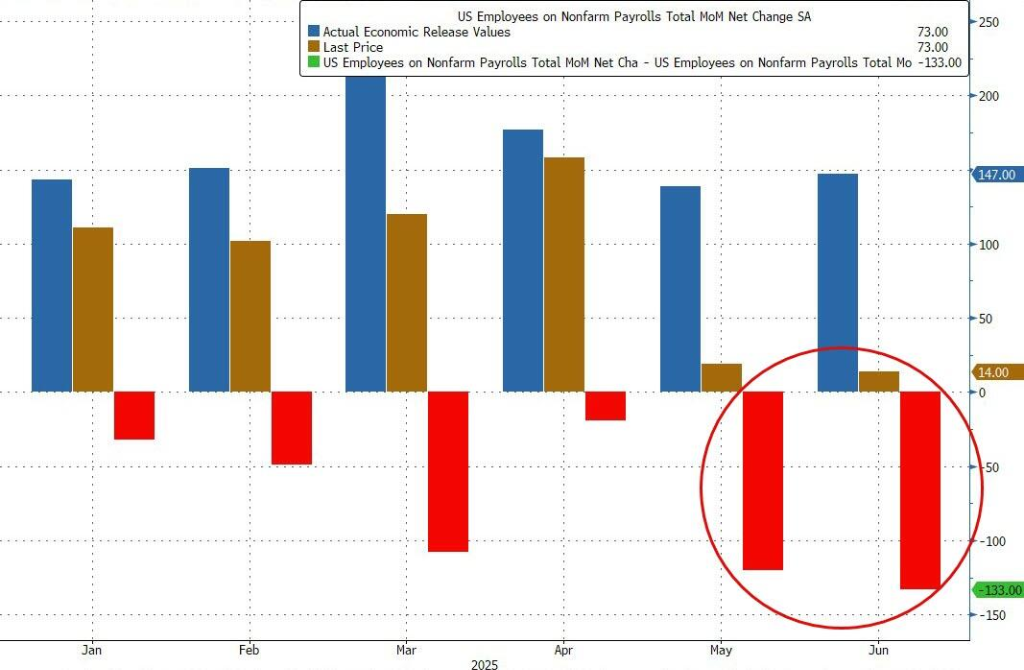

Goldman Sachs pointed out that the current technology sector is still significantly constrained by interest rate volatility.In particular, in the context of the Federal Reserve officials on the path of interest rate cuts during the year there is disagreement, 10-year U.S. bond yields rise slightly enough to trigger a valuation adjustment in the TMT sector.At the same time, the sensitivity of TMT to economic growth is also rising, such as manufacturing PMI and other data on the marginal impact of growth-oriented technology stocks is strengthening.

This means that technology stocks have evolved from "univariate (interest rate) driven" to "multivariate (interest rate + macro growth) resonance" under high volatility.

Active capital has turned conservative, and retail trading is declining.

At the funding level, Goldman Sachs tracked ETF and active fund flow data showed that TMT inflows started to turn marginally weaker at the end of July.In particular, daily inflows into some AI-themed ETFs slowed significantly.At the same time, data from hedge funds shows a clear trend: a reduction in holdings of growth tech stocks, especially higher-valued AI chains.

More noteworthy is the ebbing of retail trading fervor. The decline in the share of active tech stocks traded on the $Robinhood(HOOD)$ and $Fidelity platforms reflects a weakening of retail investors' pursuit of "high Beta + high expectations" combinations.

Earnings season results diverge, expectations pull back, market tolerance decreases

In the just-concluded Q2 earnings of large technology companies, although the overall performance is not bad, but the market reaction is quite cautious, and even part of the good was "cash that is the top" sentiment masked.

Google $Alphabet(GOOG)$ $Alphabet(GOOGL)$ Search advertising business exceeded expectations, but capex guidance was revised upward due to AI training and reasoning needs, and shares retreated.

$Meta Platforms, Inc.(META)$ Solid ad growth, but CapEx lift worries market on near-term profitability.

$Microsoft(MSFT)$ : Azure cloud revenue misses estimates as market begins to revisit CoPilot commercialization pace.

$Amazon.com(AMZN)$ Cloud business picks up, but consumer business falls slightly short of optimistic market expectations.

$NVIDIA(NVDA)$ (no earnings yet): Market expectations are too high, and short-term gains have price-in very high earnings expectations, so any small deviation could trigger an adjustment.

Goldman Sachs pointed out that the market is now more concerned about the achievability of "Q3 and full-year guidance" rather than the actual performance of Q2.The focus of earnings reaction is shifting from current performance to forward guidance, and investor tolerance is declining.

Valuation and Earnings Expansion Narrow, ROIC Returns Become the New Anchor Point

Current valuations of large-cap tech stocks remain at historically high levels.Goldman Sachs pointed out that although the overall technology sector's earnings estimates have been revised upward, but the extent of the upward revision is significantly less than in 2023, the momentum of valuation expansion is decaying.

The chart shows that Mega Cap Tech's 12-month expected price-earnings ratio is still higher than its five-year average, especially "AI pure concept stocks" in the absence of obvious earnings realization, the risk of valuation repair rises.In contrast, companies with higher ROIC (return on investment) and AI capital expenditures that can directly drive revenue growth are starting to gain more weight in the market.

How to respond?

Select high-quality growth stocks and reduce purely thematic exposure.In the current environment, it is recommended that more emphasis should be placed on the ability to deliver on performance and the margin of safety in valuation, rather than continuing to bet on valuation inflation.

Reduce holdings of AI concept stocks with excessive valuation and lack of earnings support;

Increase holdings of core technology leaders with clear AI application landing and good cash flow;

Interest rates are still likely to oscillate upward, and growth stocks with high interest rate sensitivity should be moderately hedged;

Style preference "high earnings / low valuation" combination, reduce high Beta risk exposure.

In conclusion - a tipping point for style switching?Focus on inputs and outputs

The valuation-driven market is failing in stages, and profitability and capital expenditure efficiency have become the new anchor points.For investors chasing themes, this may be a "style switch" tipping point, while for those who adhere to the fundamentals of stock selection, may be ushering in structural opportunities.

Focus on fundamentals and ROIC, in order to traverse the ups and downs of the AI narrative.

Comments