The recently released Q2 financial report of $Circle Internet Corp.(CRCL)$ showed strong overall performance, exceeding market expectations and highlighting the company's leading position and growth potential in the stablecoin sector.

We believe that this quarter's performance can be rated as "excellent," with the key highlight being a 90% year-on-year surge in USDC circulation, driving a 53% increase in revenue, further fulfilling previous expectations. Adjusted EBITDA also achieved a 52% year-on-year increase. However, potential drawbacks include non-cash expenses related to the IPO resulting in a substantial net loss, and distribution costs growing faster than revenue, slightly eroding profit margins, reflecting the company's cost control pressures amid rapid expansion.

Key information from the financial report

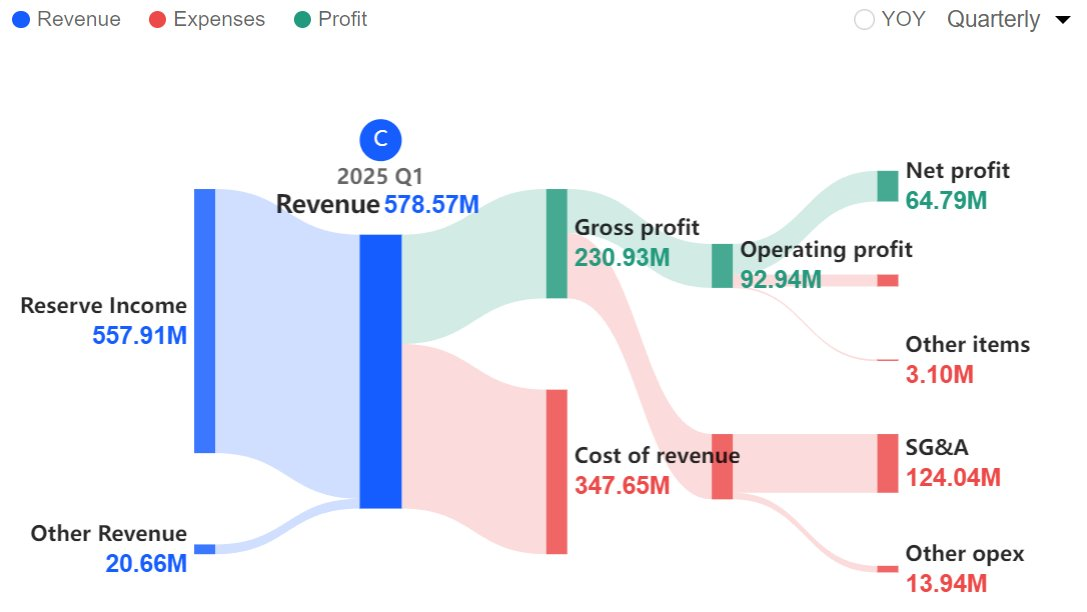

Total Revenue and Reserve Revenue: Total revenue for the quarter reached US$658 million, representing a year-over-year increase of 53% and a quarter-over-quarter increase of approximately 15%; core reserve revenue was US$634 million, up 50% year-over-year. The primary drivers stemmed from an 86% year-over-year surge in the average circulation of USDC. Despite a 103-basis-point decline in the reserve return rate to 4.1%, the overall performance benefited from the Federal Reserve's high-interest-rate environment and the recovery in demand for stablecoins. This metric exceeded market consensus (expected at $647.3 million), with signs of business structure changes evident as USDC market share rose to 28%, up 595 basis points year-over-year, indicating the company is expanding from crypto trading into traditional payments and merchant networks.

Adjusted EBITDA: $126 million, up 52% year-over-year, with a margin of 50%. The underlying logic reflects improved profitability in core business operations, with efficient operations evident after excluding non-cash expenses. This metric exceeded expectations ($121.1 million), but within the business changes, note that the RLDC (reserved revenue minus distribution costs) margin decreased from 42% in the same period last year to 38%, suggesting increased cost pressure from distribution partners (such as Coinbase's revenue share), which may indicate the need to optimize the revenue-sharing structure in the future.

USDC circulation: reached $61.3 billion at the end of the quarter, a 90% year-on-year increase, and further rose to $65.2 billion as of August 10; the number of wallets increased by 68% year-on-year to 5.7 million. Driving factors include improved regulatory clarity (such as the GENIUS Act) and expanded partnerships (such as integration with FIS's payment network), which are driving merchant and cross-border payment adoption. This metric far exceeded market expectations, with signs of structural changes in business operations indicating a shift in stablecoins from crypto trading toward global payments and DeFi applications, with market share nearing Tether's 67%.

Net loss: $482 million, a year-over-year shift from profit to loss, primarily due to non-cash expenses related to the IPO totaling $591 million (including $424 million in equity incentives and $167 million in fair value adjustments for convertible bonds). This reflects a one-time impact post-IPO, unrelated to core operations. This metric is weaker than market consensus (expected loss per share of $1), but excluding these items reveals profit potential. The business changes highlight the growing pains of the company's transition from private to public, which may impact short-term valuation stability.

Signals from the future

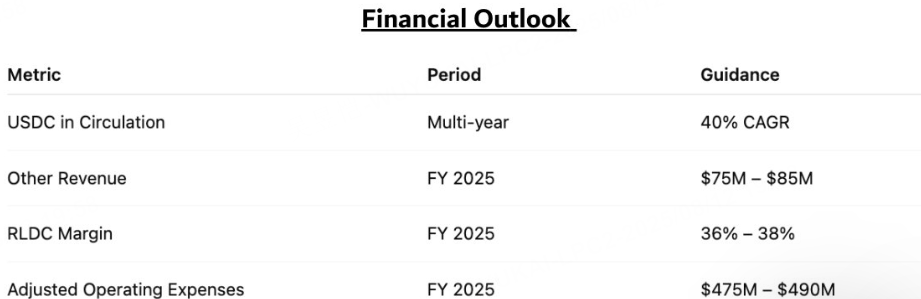

Management is optimistic about the outlook for Q3 and the full year, with USDC circulation expected to grow at a long-term compound annual growth rate of 40%, other income of $75-85 million in 2025, adjusted operating expenses of $475-490 million, and RLDC profit margins remaining at 36-38%.

Although this guidance is somewhat aggressive, it is based on the overall expansion of the stablecoin market and the company's infrastructure investments (such as the Arc blockchain and cross-chain protocols). Considering intensifying competition and regulatory uncertainty, it may slightly exceed market consensus to boost confidence.

Short-term cost pressures remain, but the overall aim is to reinforce investor confidence in the company's positioning as the "digital dollar infrastructure." Comparisons with previous quarters (such as Q1 USDC growth of 78%) demonstrate management's assessment of the trend's sustainability.

Key Investment Points

USDC has a strong scale effect

Circle's core revenue source is "reserve income," which refers to the interest income generated from the company's investment of users' USD/short-term assets. With the average circulation of USDC increasing by +86% year-over-year, reserve income rose by +50% year-over-year, driving a significant increase in total revenue. The low marginal costs associated with scale expansion are reflected in the higher adjusted EBITDA.

Cost concerns

The primary reason for the GAAP loss was not operating cash outflows, but rather non-cash accounting items resulting from the IPO, including a one-time $424 million equity incentive expense (RSU triggering) and a $167 million increase in the fair value of convertible bonds due to rising stock prices.

After removing these items, operating indicators (Adj-EBITDA) still show healthy profitability. For investors, this means that "accounting losses do not equal operational failure," but attention should be paid to future stock-based compensation, convertible bonds, and dilution dynamics.

However, distribution expenses increased by 64% year-over-year ($407 million), primarily due to the growth in USDC circulation and distribution payments associated with holding coins on channels such as Coinbase. While distribution drives scale, its growth rate exceeding revenue growth compresses the RLDC margin (38% this quarter, down 408 basis points year-over-year). The company's FY25 RLDC guidance is 36–38%, and management appears to expect this distribution rate to persist in the short term. If sustained long-term, it could erode the high-margin characteristics of the stablecoin business.

At the same time, the reserve return rate fell by 103 basis points from the same period last year to 4.1%, indicating that interest rate trends (and the returns on short-term government bonds/money market funds held by the company) have a direct impact on revenue. Even if the scale of USDC continues to expand, a decline in interest rates will compress reserve income, and vice versa. Investment decisions need to take into account both "USDC scale growth" and "interest rate environment."

Business Progress and Growth Path

The company has launched Circle Payments Network (CPN), Circle Gateway (cross-chain instant settlement), and Arc (proprietary Layer-1, with USDC as the native gas). These are key initiatives for the company to expand from "stablecoin issuance" to "full-stack financial infrastructure." If these products can be commercialized (APIs, bank/institutional access, cross-border corridors), they will amplify unit revenue and reduce reliance on the "reserve spread" alone.

This quarter, we announced partnerships with Binance, FIS, Fiserv, Corpay, OKX, and others. In the short term, these partnerships will promote liquidity and distribution, but in the long term, we need to assess the impact of distribution terms (revenue sharing/commissions) on gross profit. On the other hand, the signing of the GENIUS Act (which will establish a federal framework for payment stablecoins) is a long-term positive development, as it will help compliant market leaders expand their market share. However, the details of the bill and the regulatory requirements after its implementation still need to be closely monitored.

Valuation level

As a "network effect + scale-driven" financial infrastructure company, valuation will be highly dependent on the future growth rate of USDC, the sustainability of RLDC Margin, and the monetization path of Arc/CPN. In the short term, post-IPO dilution, RSU issuance, and convertible bond revaluation will also amplify stock price volatility. Dynamic assessments should be made based on market pricing for the IPO, investor sentiment, and analyst views (media/brokerage coverage).

The current market capitalization is approximately $36 billion (up 350% since the IPO), implying a 17x revenue multiple (PS) and a 95x EBITDA growth expectation. The market valuation is already quite robust. Assuming USDC continues to grow at a 40% CAGR, this could support further expansion. However, if yields continue to decline or Tether gains market share, there is a risk of a correction; Compared to comparable companies such as $Coinbase Global, Inc.(COIN)$ (similar market cap but more diversified revenue, valued at approximately 12x revenue), CRCL may be overvalued. When compared to Tether (unlisted but holding a 67% market share), CRCL's compliance advantages are undervalued, and USDC still has room for penetration in DeFi and merchant payments.

strategic judgment

Management's overall strategy is sound, but there are some misconceptions, such as excessively high distribution costs (up 64% year-on-year). Infrastructure investments (such as the Arc blockchain and pilot program with ICE, using USDC as collateral for traditional financial settlements) deserve greater attention, as they indicate that the company is moving toward platform expansion, transforming from a mere issuer to a full-stack service provider. Signals of horizontal expansion include partnerships with FIS and Shopify, comparable to Airbnb's expansion from accommodations to experiences. It is recommended to increase penetration into emerging markets (such as Argentina and Vietnam) to capture grassroots adoption.

Comments

Great article, would you like to share it?