$Netskope, Inc.(NTSK)$ This IPO has finally taken center stage. With the latest disclosures laid out, the market immediately grew restless. The ticker is "NTSK," listed on the Nasdaq.

The company plans to issue 47.8 million Class A common shares at a price range of $15 to $17 per share. If priced at the upper end, the offering could raise up to $813 million, targeting a valuation of $6.5 billion. Compared to the $7.5 billion valuation from its 2021 private placement, this represents a slight downward adjustment—essentially reflecting market conditions that no longer permit overly "lofty" valuations.

What about the fundamentals?

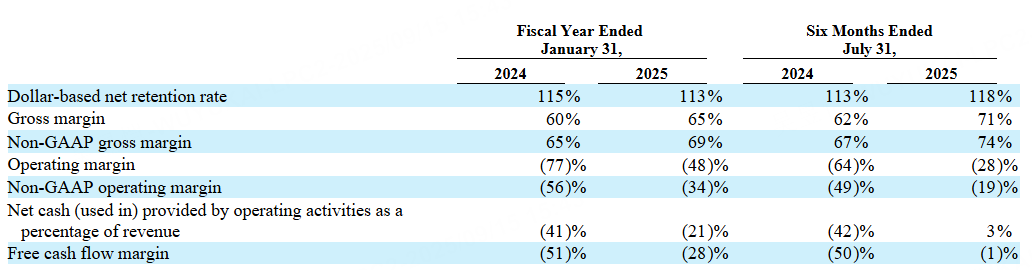

Netskope's growth trajectory remains smooth. By July 2025, its ARR reached $707 million, marking a 33% year-over-year increase and demonstrating solid momentum. Revenue for the first half of fiscal year 2026 grew by 30.7%, remaining comfortably above the 30% threshold. While the company remains unprofitable, losses have narrowed compared to last year: the net loss for the first half was $169.5 million, significantly lower than the $206.7 million loss in the same period last year. The full-year loss is projected to be approximately $354.5 million. Gross margin has also improved to 71%. The company now serves over 4,300 customers, including major Fortune 100 clients, with a net retention rate of 118%. These figures would certainly impress investors during roadshows.

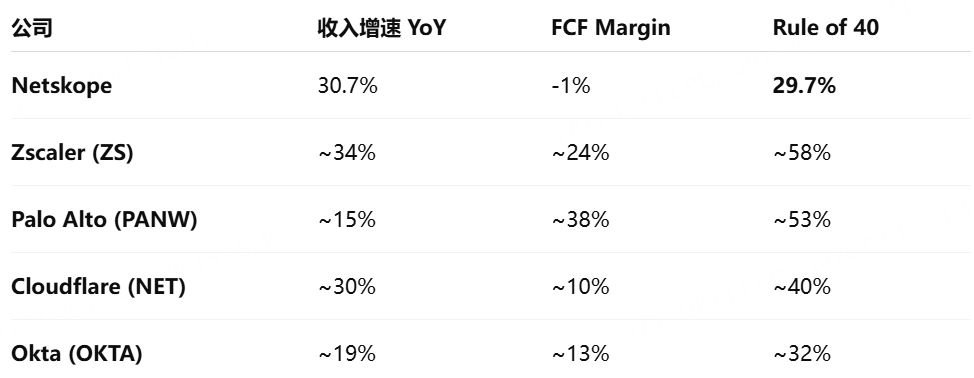

Calculating the Rule of 40 based on FCF Margin, Netskope's valuation appears relatively reasonable compared to its peers, with the Rule of 40 for H1 FY2026 ≈ 29.7%.

707 million ARR, corresponding to a 6.5 billion market cap, translates to a 9.1x ARR multiple. This multiple sits squarely in the middle of the 8–12x range—neither making investors feel it's overpriced (leaving room for an IPO) nor appearing too cheap. In plain English: this price is the "market-acceptable middle ground." Stop nitpicking.

Netskope enters the market with a script of "stable growth, narrowing losses, and high customer retention," appearing more grounded after its valuation compression. Barring market turbulence, this stock could genuinely reignite the long-dormant cloud security IPO market.

Comments