The Federal Reserve announced at its September FOMC meeting that it would lower the target range for the federal funds rate by 25 basis points (0.25%), adjusting it from 4.25%–4.50% to 4.00%–4.25%. This marks the first rate cut since December 2024. The meeting statement and economic projections indicate officials anticipate a high probability of two more rate cuts during the remainder of 2025, with a potential additional adjustment in 2026. This move reflects the Fed's increasingly cautious approach to balancing inflation pressures with the need to address a weakening job market.

Background of the Interest Rate Cut and Immediate Market Reaction

One of the primary drivers behind the Fed's rate cut this time was the emerging trend of a moderate slowdown in the job market: hiring activity has decelerated, certain employment indicators (such as weekly hours worked and employment among marginal labor force participants) have shown weakness, and there is a risk of rising unemployment. Meanwhile, inflation remains above the 2% target level, but core PCE and overall inflation pressures have eased in certain aspects. Additionally, some price increases stemming from trade and tariffs are viewed as one-off or "transitory" factors.

The Federal Reserve characterized this rate cut as a "risk-management" policy adjustment, aimed at mitigating the risk of further deterioration in the job market while not neglecting inflation control.

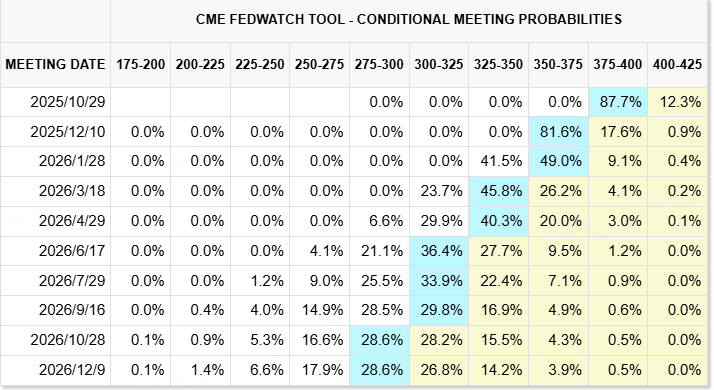

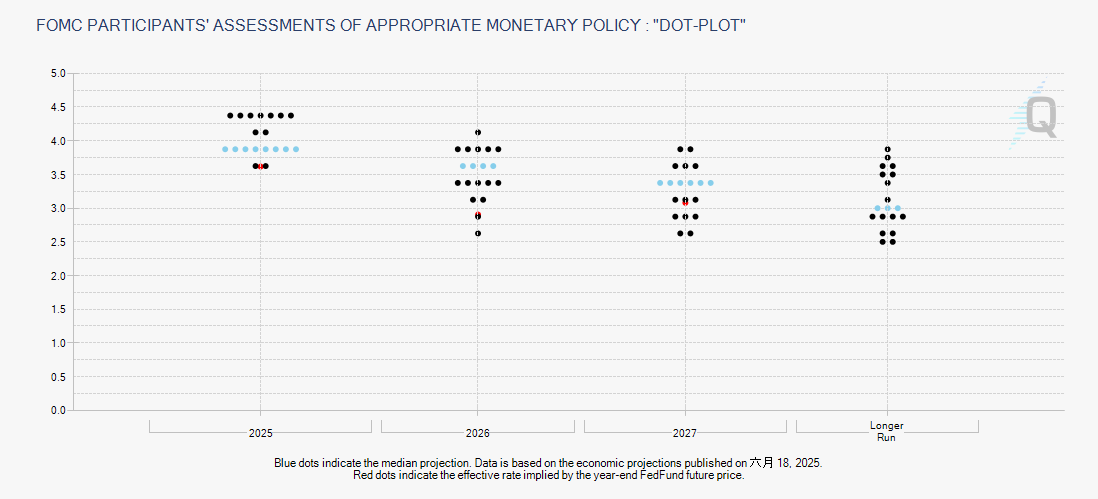

In the market, the 25-basis-point cut was largely anticipated, with many economists predicting the rate reduction ahead of the meeting. However, there is significant divergence regarding the number and magnitude of future additional rate cuts. Some market participants align with the Fed's median projection (two more cuts), while others believe more aggressive action may be necessary if employment and inflation data deteriorate further or deviate from expectations.

Following the interest rate cut announcement, market reactions were relatively subdued: stock indices saw a brief lift, but overall volatility remained muted; bond and dollar markets diverged in direction, with some spread expectations adjusting. Investors are largely awaiting key upcoming economic data—such as employment figures, payroll growth, average hourly earnings, and core inflation—to confirm whether further action is warranted.

Potential Impacts and Future Outlook

Below are the potential economic impacts and risks based on current policies and market expectations, incorporating widely held views online:

Conclusion

Overall, the Federal Reserve's decision to cut interest rates at its September meeting represented a modest adjustment in line with market expectations, rather than a large-scale stimulus. It reflects the Fed's concern over downside risks to the labor market while maintaining vigilance regarding the fact that inflation has not yet been brought back to the 2% target.

The focus for investors and policy observers going forward should be:

Employment Market and Inflation Data: Job Openings, Employment Growth, and Wage Increases; Whether Inflation Continues to Decline

Divergence Among Fed Members and Dot Plot Updates for Future Meetings

Can the global trade environment, supply chains, and tariff policies remain stable, and will they bring new inflationary pressures?

Will the market overreact to the "anticipated rate cut," leading to increased volatility in asset prices?

If a soft landing is achieved, this shift toward moderate rate hikes and expectations of rate cuts will help sustain confidence and growth. But the risks are significant: a resurgence of inflation or a steeper-than-expected deterioration in employment could force a policy pivot.

$S&P 500(.SPX)$ $SPDR S&P 500 ETF Trust(SPY)$ $NASDAQ 100(NDX)$ $Invesco QQQ(QQQ)$ $NASDAQ(.IXIC)$ $ProShares UltraPro QQQ(TQQQ)$ $ProShares UltraPro Short QQQ(SQQQ)$ $US10Y(US10Y.BOND)$ $US30Y(US30Y.BOND)$ $Cboe Volatility Index(VIX)$ $iShares 20+ Year Treasury Bond ETF(TLT)$

Comments

Great article, would you like to share it?