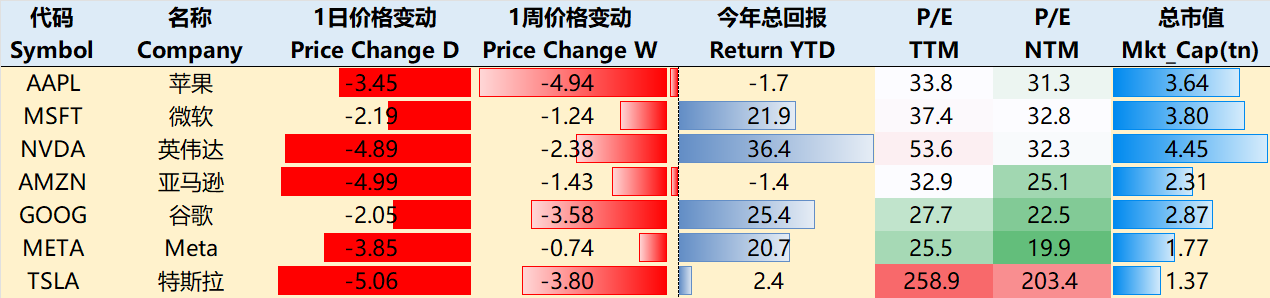

Big-Tech’s Performance

Macro Headlines This Week:

The U.S. government shutdown continues to ripple through the economy. Since entering shutdown mode on October 1, select federal agencies have halted normal operations, delaying data releases and curtailing government contracts and project spending. Key economic indicators—like employment and manufacturing reports—are proving hard to release on time, reducing market visibility. That said, CPI data is still slated for release on October 24, thanks to the Labor Department recalling some staff to compile it (to avoid unduly influencing the Fed). Meanwhile, several state economies are showing contraction signals, with heavyweights like California and New York nearing inflection points.

Tariff threats are reigniting tensions. Trump posted on social media, warning that China's restrictions on rare earth exports could trigger 100% tariffs on Chinese goods if unresolved—stoking fears of a U.S.-China trade war reboot. Markets may now enter a "Tariff Tumble" phase: an upward cycle prone to abrupt interruptions from policy shocks. In this downturn, tech and growth stocks are taking the biggest hit.

The current market rally still carries "high-quality" underpinnings. The gains are primarily driven by large-cap, profitable, AI-powered companies rather than broad speculation. AMD and Dell announced major deals with OpenAI, underscoring ongoing market favoritism toward tech AI plays.

Big Tech showed a pattern of initial gains followed by pullbacks this week. NVDA hit new highs before retreating; as of the October 10 close, the past week's performance included $Apple(AAPL)$ -4.94%, $Microsoft(MSFT)$ -1.23%, $NVIDIA(NVDA)$ -2.38%, $Amazon.com(AMZN)$ -1.43%, $Alphabet(GOOG)$ $Alphabet(GOOGL)$ -3.57%, $Meta Platforms, Inc.(META)$ -0.74%, and $Tesla Motors(TSLA)$ -3.80%.

Big-Tech’s Key Strategy

The Bigger the Storm, the Steadier Microsoft?

Macro IT budgets remain fertile ground for Microsoft's growth. MS's CIO survey indicates stable IT budget growth expectations of +3.6% for 2025, with the software subsector leading at +3.8%. Early glimpses of 2026 show overall acceleration to +3.8%, with software surging even more to +3.9%—well ahead of hardware (+1.5%), communications (+2.5%), and services (+2.3%)—affirming the cloud migration megatrend. AI/ML, security, and digital transformation top the priorities, all Microsoft strongholds least likely to face cuts.

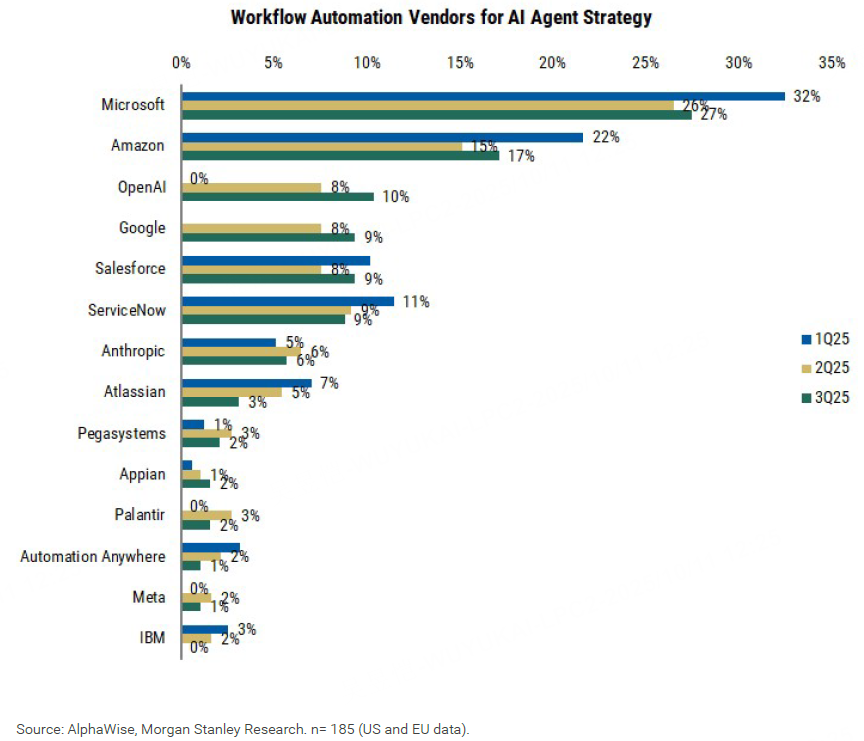

From a growth perspective, GenAI is the killer app. Markets expect Microsoft to capture the largest GenAI incremental share in 2025, far outpacing Amazon's 14%; over three years, it's projected at 37%, leading OpenAI's 12%. Why does Microsoft stand out? Four core drivers:

Microsoft's tight alignment with CIOs' pragmatic themes like AI/ML, security, and digital transformation, which play to its product strengths (e.g., Copilot and Azure AI);

Deep integration within its software ecosystem, enabling seamless GenAI embedding into existing workflows and minimizing enterprise switching costs;

A vast product portfolio spanning the full chain from cloud infrastructure to enterprise apps, reaching billions of users;

Massive investments in AI infrastructure—including data center expansions and chip procurements—that have built competitive moats. By contrast, OpenAI excels in innovation but lacks Microsoft's end-to-end execution prowess.

Source: Alpha Wise

Moreover, Microsoft's penetration in GenAI agent strategies hits 27%, versus Amazon's 17% and OpenAI's mere 10%, with Google, Salesforce, and ServiceNow forming a long tail. This means Microsoft isn't just leading at the infrastructure layer—it's building an "AI agents" ecosystem at the application layer to drive automation shifts.

Recent surveys show Copilot licenses up 400% year-over-year, with early users shifting from "full automation" fantasies to prompt engineering education; Studio tools are a highlight, embedded in Power BI and Azure. This also reflects Microsoft's pivot post-OpenAI mega-deal to broader enterprise clients, yielding higher long-term ROI.

Azure's cloud growth momentum is the strongest among the big three, buoyed by small and medium-sized businesses (SMBs) as a key growth engine. Leveraging product bundling and customized AI agents, Microsoft is steadily gaining share. Azure's platform clocked 30% growth, beating distributor expectations and highlighting SMBs' growing urgency for cloud migration; modern workplace suites (including Teams and Office 365) advanced steadily at 18-22%, supporting remote collaboration needs.

Notably, while Azure's growth is robust, it lags slightly behind Microsoft's official earnings guidance—due to SMBs' "lagging effect" in AI adoption. Generative AI requires enterprises to build advanced infrastructure like data pipelines and skills training. This isn't a structural Microsoft issue but a natural SMB maturity phase; as education and incentives kick in, the gap should close quickly.

On the macro front, with Fed rate cut expectations lifting SMB confidence and IT spending appetite, headwinds persist from sudden 100% tariff announcements, which spike probabilities of escalated U.S.-China trade friction. Expanded tariffs and export controls could disrupt critical raw materials (rare earths), high-end chips, and software exports, adding costs and procurement hurdles to AI infrastructure (GPU/ASIC buys, servers)—pressuring SMB IT budgets. Hyperscale cloud providers (AWS, Google Cloud, Microsoft Azure) and players with in-house ASICs or bulk buying power will better weather these shocks.

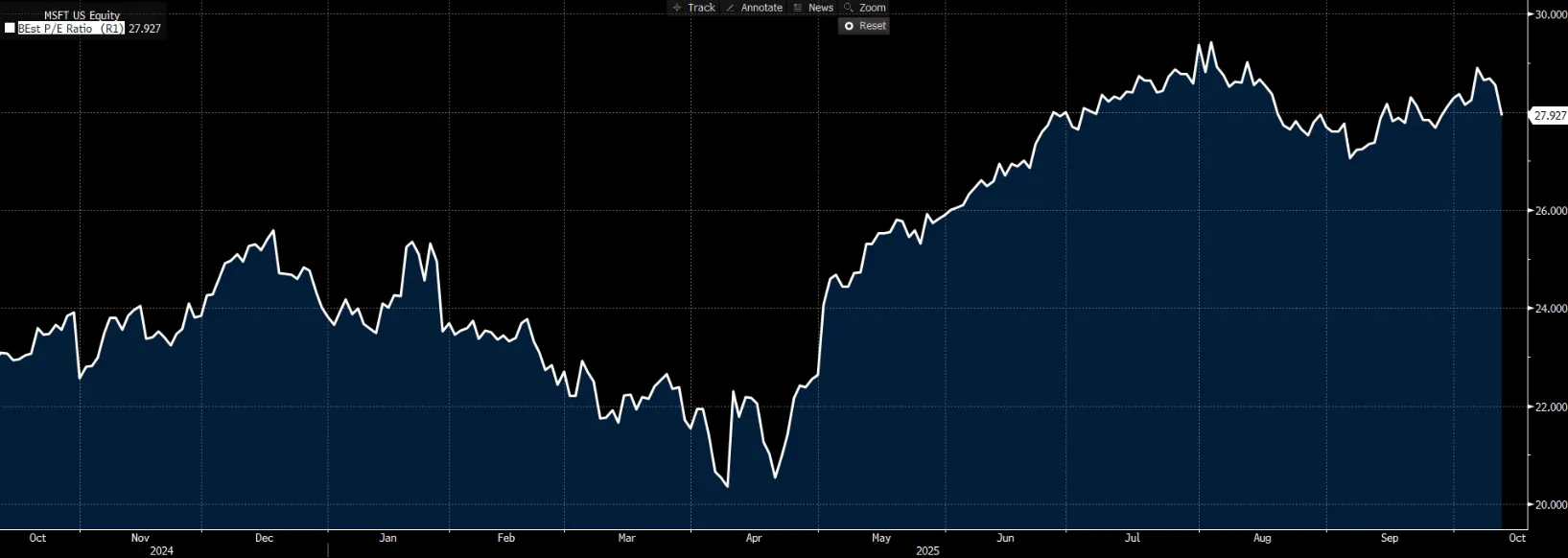

Finally, on valuations, Microsoft trades at 33x NTM forward P/E, in line with the broader market's non-GAAP average. But based on 2027's projected $19.73 GAAP EPS, it's just 28x—leaving room for upside over the next year.

Big Tech Options Strategies

This Week We Focus On: Can Oracle Break Through the Doubts?

$Oracle(ORCL)$ has undergone a stunning transformation over the past year. From a traditional software giant once seen as lagging in digital transformation, it's now riding bold long-term guidance, massive AI contracts, and positioning as an AI infrastructure leader. The recent earnings surge stemmed from uplifted OCI (cloud infrastructure) revenue guidance (from $10 billion in FY2025 to $144 billion in FY2030) and a quarter-over-quarter leap in remaining performance obligations (RPO) (from around $100 billion to $317 billion). Yet amid this rebound, skeptical news reports and sell-side research have sown investor confusion, zeroing in on margin pressures and customer concentration risks.

The Information cited alleged internal documents claiming AI sales tripled year-over-year but with gross margins around 16%—dipping below 10% in spots. Oracle's trajectory mirrors Microsoft's Azure: During its aggressive global expansion in FY2016, margins cratered to -68%, with compute asset intensity at 341% of IaaS/PaaS revenue. But as growth moderated and efficiencies kicked in, margins rebounded to 32% in FY2019 and hit 62% in FY2022. Thus, Oracle must address key questions:

Can it scale into a hyperscaler, driving long-term EPS and FCF expansion?

Can it evolve from AI bystander to core player?

Next week's FAM conference (October 16) will bring more transparency—not direct margin disclosures, but emphasis on revenue profitability's lift to EPS and EBIT. Updates to FY2029 total revenue guidance (beyond OCI) could reaffirm steady non-AI growth in SaaS and multi-cloud databases (20%+).

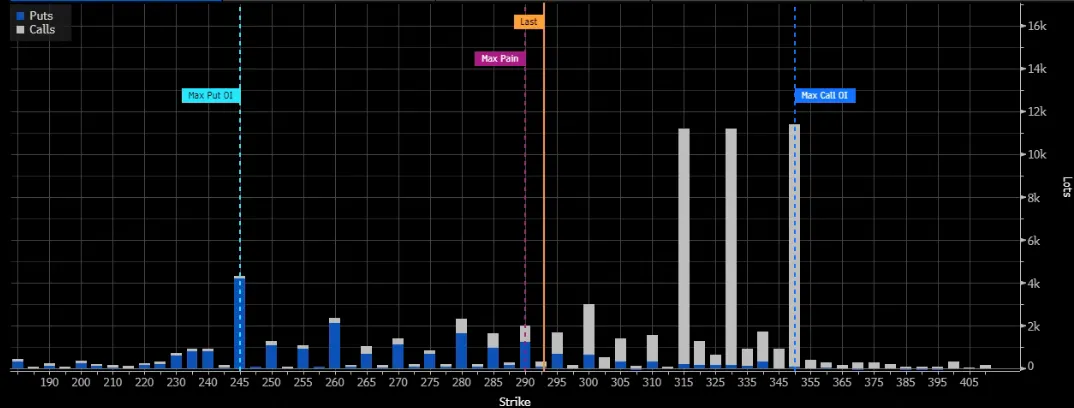

Despite the broad tech selloff on October 10, ORCL (-1.35%) outperformed the market, signaling non-trivial bullish forces. From an options lens, ORCL saw heavy 300-350 strike volume as closing orders in late October and November weeks, with unusual large trades at 315-330-350 for the week of October 24.

Big Tech Portfolio

The Magnificent Seven—forming an equal-weighted "TANMAMG" portfolio, rebalanced quarterly—have delivered backtested results far surpassing the $S&P 500(.SPX)$ since 2015: total returns of 2,915.53% versus $SPDR S&P 500 ETF Trust(SPY)$ 's 282.01%, for excess returns of 2,633.52%, and still trading at elevated levels.

Year-to-date, Big Tech's gains have hit new highs at 17.54%, topping SPY's 12.4%.

$Invesco QQQ(QQQ)$ $NASDAQ 100(NDX)$ $NASDAQ(.IXIC)$ $ProShares UltraPro QQQ(TQQQ)$ $ProShares UltraPro Short QQQ(SQQQ)$

Comments