$Hims & Hers Health Inc.(HIMS)$ delivered strong revenue but faced profitability pressures in its Q3 2025 earnings report. Overall, the performance exceeded market expectations, primarily driven by rapid growth in subscription users and expansion of personalized healthcare services. Revenue surged nearly 50% year-over-year, but net profit declined and EPS fell short of analyst consensus, reflecting underlying challenges in cost control and supply chain management.

Despite this, discussions regarding a potential collaboration with $Novo-Nordisk A/S(NVO)$ on Wegovy emerged as a major highlight, potentially signaling a strategic resurgence in the company's weight loss sector. However, caution is warranted regarding risks stemming from intensifying competition and regulatory uncertainties.

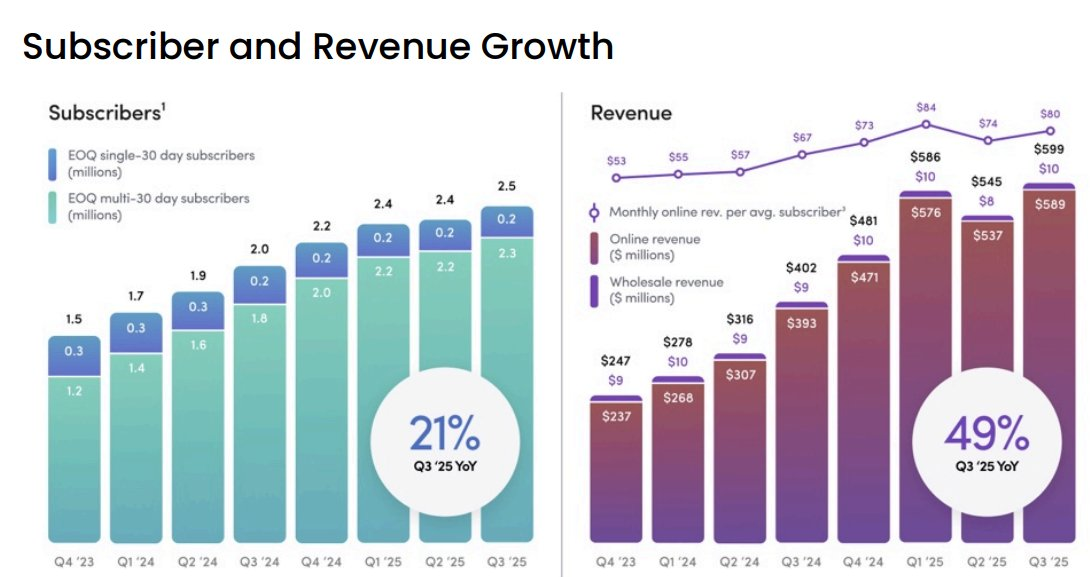

Key Financial Highlights

Revenue Performance: Quarterly revenue approached $600 million, surging 49% year-over-year and growing approximately 15% quarter-over-quarter. This growth was primarily driven by explosive expansion in subscription users (estimated to exceed 20 million) and robust demand for personalized healthcare products, particularly in weight management and mental health. Actual revenue exceeded market expectations (analyst consensus forecast of $580 million), highlighting the resilience of the company's platform model while also exposing structural risks associated with reliance on high-growth businesses.

Net profit and EPS. Net profit was approximately $15.87 million, equivalent to $0.06 per share, representing a significant year-over-year decline (compared to $75.99 million and $0.32 per share in the same period last year) and falling short of market consensus ($0.10 per share). The underlying reasons include supply chain disruptions and increased marketing expenditures, particularly affecting the weight-loss product line due to the earlier termination of the Novo collaboration, which exerted slight pressure on gross margins. Despite this, the company maintained profitability, demonstrating improved operational efficiency. However, this weakness may reflect challenges from short-term cost inflation.

Adjusted EBITDA exceeded $78 million, marking a significant year-over-year increase that reflects enhanced profitability driven by economies of scale. Key drivers included improved subscription renewal rates (estimated at over 70%) and the realization of operating leverage. This metric exceeded expectations, indicating the health of the company's core business. However, it is important to note that increased volatility in the weight-loss product line could potentially drag down future profit margins.

Subscription users continue to expand, with quarterly additions potentially exceeding 3 million, representing a year-over-year growth rate of approximately 40%. This shift signals the company's successful structural transition from a focus on male health to encompassing women's and comprehensive healthcare. However, the increased proportion of weight loss services (accounting for about 30% of revenue) also implies greater reliance on external supply chains, such as GLP-1 drugs. The weaker-than-expected performance partly stems from earlier supply disruptions of Wegovy.

Gross margin stood at approximately 76%, remaining flat quarter-over-quarter but slightly declining year-over-year, primarily due to rising costs of combination drugs. While this metric did not exceed expectations, it indicates the company's potential for recovery through supply chain optimization (such as potential collaboration with Novo). Structurally, the increased contribution from personalized medicine signals long-term profit potential.

Guidance

Management expressed a relatively optimistic outlook for the fourth quarter and full year of 2025, projecting Q4 revenue between $605 million and $625 million. The full-year revenue target has been raised to $2.335 billion to $2.355 billion, representing a 58%-59% year-over-year growth rate. This guidance leans aggressive, implying an assumption of accelerated sequential quarterly growth and exceeding market consensus expectations (approximately $2.3 billion for the full year). It reflects confidence in user growth and product line expansion.

During the earnings call, CEO Andrew Dudum emphasized: "We are actively discussing with Novo Nordisk to introduce Wegovy injections and the oral version (pending FDA approval) to the Hims & Hers platform, which will further enhance consumer choice."

Key Investment Considerations

HIMS' personalized healthcare and subscription model represents a sustainable long-term growth track, particularly in mental health and chronic disease management. These domains rely on data-driven platform operations, akin to Airbnb's ecosystem building in the lodging sector, enabling repeat purchases and cross-selling through user retention. In contrast, while weight loss services exhibit rapid growth, their reliance on GLP-1 drugs and short-term trends like obesity epidemics resembles the 2023-2024 AI hype cycle. Should the Novo partnership falter or competition intensify (e.g., $Eli Lilly(LLY)$ 's Zepbound), this sector could transform into a volatile asset class. We believe the sustainability of the weight loss sector hinges on supply chain diversification rather than purely being topic-driven.

Management's current strategy centers on platformization (e.g., integrating multiple categories within the app). The application of data AI deserves amplified focus, as it enhances personalized recommendations—similar to Airbnb's algorithm optimization. However, a pitfall lies in overreliance on weight-loss services while neglecting international expansion (e.g., the European market, akin to Ctrip's globalization). Signals indicate the company is moving toward platformization (e.g., discussions with Novo suggest horizontal collaboration), potentially signaling a shift from DTC to a B2B2C model. We recommend increasing exposure to sectors with high AI penetration to mitigate single-track risks.

HIMS currently has a market capitalization of approximately $10 billion, implying an expected 30% revenue growth by 2026 (based on an EV/Sales multiple of about 4x). The market has priced in its platform expansion potential, but valuation divergence stems from fluctuations in its weight loss business. Some investors view it as the next $Teladoc Health Inc.(TDOC)$ However, HIMS' valuation remains reasonable, and its weight loss segment may be undervalued. Should the Wegovy partnership materialize, it could drive a re-rating.

Comments