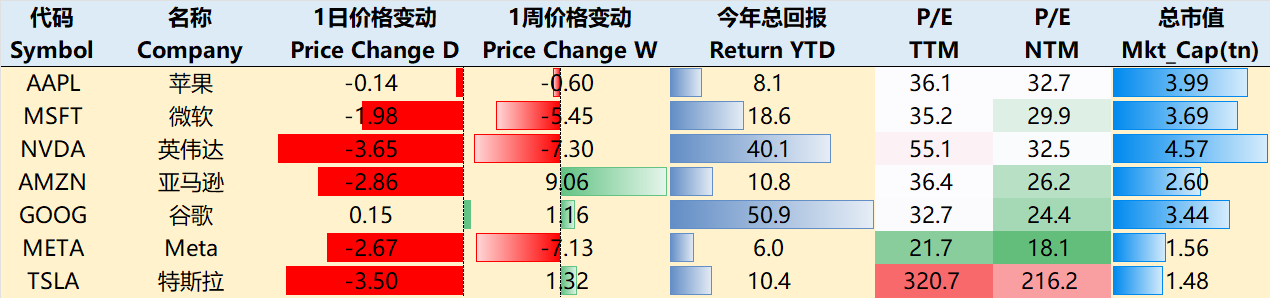

Big-Tech’s Performance

Macro Headlines This Week:

Prolonged U.S. Government Shutdown Adds to Policy Uncertainty

The ongoing U.S. government shutdown has now become one of the longest on record. The policy backdrop remains characterized by a triple squeeze: loose expectations, weak macro data, and rising institutional risks. Although the Fed still has room to cut rates, the path forward remains unclear.

U.S. Economy in a “Structural Caution” Phase

Employment remains weak and layoffs are rising, though the service sector continues to show resilience. The government shutdown has created data blind spots, complicating policy assessment. Meanwhile, trade and tariff uncertainty remain key external risks. For both policymakers and investors, the medium-term environment suggests slower growth, inflation that hasn’t yet fully eased, and elevated policy and institutional risk.

Equities Show Signs of Fatigue

U.S. equities pulled back from highs this week, showing classic late-cycle behavior—momentum fading and awaiting confirmation of a turning point. Tech stocks, the engine of this bull market, are showing signs of rotation. The sector remains vital but is shifting from growth in quantity to quality of earnings. Investors should focus on firms with stable profitability, clear business models, and reasonable valuations rather than chasing AI hype. Near term, the pullback looks more like a structural correction than an end of cycle—but return expectations should be recalibrated.

As of November 6 close: $Apple(AAPL)$ -0.6%, $Microsoft(MSFT)$ -5.45%, $NVIDIA(NVDA)$ -7.3%, $Amazon.com(AMZN)$ +9.06%, $Alphabet(GOOGL)$ $Alphabet(GOOG)$ +1.16%, $Meta Platforms, Inc.(META)$ -7.13%, $Tesla Motors(TSLA)$ +1.32%.

Big-Tech’s Key Strategy

Google Cloud: Positioned for 50%+ Revenue Growth by 2026

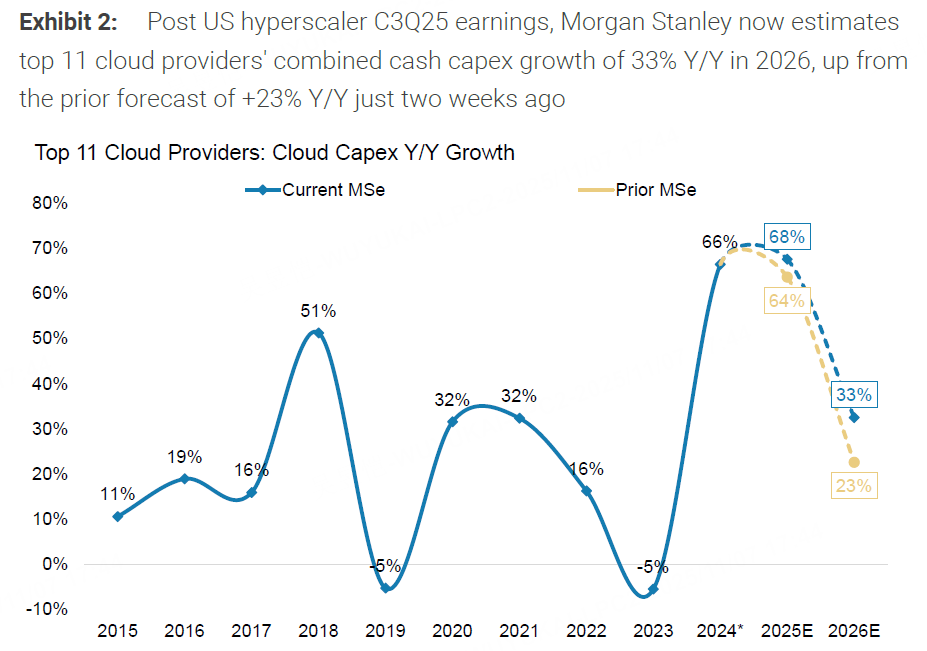

AI-Driven Capex Expansion Across Global Cloud Providers

The surge in AI infrastructure demand is fueling a sustained upward revision in capital spending among hyperscale cloud providers (CSPs). The top 11 CSPs are projected to invest $621 billion in Capex by 2026, up 33% YoY, and 10 percentage points higher than just a quarter ago.

Among the “Big Four” U.S. CSPs, Google’s Capex is expected to hit $123.4 billion in 2026, nearly doubling (+92.7%) from initial 2025 forecasts.

Google Cloud’s token processing volume has grown exponentially—from ~300 trillion in April 2024 to 1,500 trillion in September 2025—driving revenue acceleration. Aggregate cloud revenue among the top four CSPs is expected to rise from +21% YoY in Q3 2024 to +27% in Q4 2025.

Google’s Capex intensity will likely reach a record 22.3% in 2026, as the company pushes toward NVIDIA CEO Jensen Huang’s long-term goal of a $3–4 trillion annual AI infrastructure ecosystem. Suppliers like NVIDIA—whose exposure to cloud Capex exceeds 80%—stand to benefit significantly from this buildout.

Backlog Model Suggests Over 50% Revenue Growth Potential

A new Cloud Backlog Model by Morgan Stanley splits Google Cloud revenue into Backlog and Non-Backlog portions.

As of Q3, Google Cloud’s Backlog stood at $158 billion, with 55% expected to be recognized within two years (historically 45–50%).

This implies a 50%+ revenue growth potential for GCP by 2026, compared with the previous base forecast of +44%.

If net Backlog rises by $50B and Non-Backlog by 15%, overall revenue growth could hit 52%.

Even in a more conservative scenario (Backlog +$20B, Non-Backlog +25%), growth would still exceed 50%.

In the base case, total 2026 revenue growth would reach +44% YoY, with Backlog share climbing to 60%.

Each $20B increase in Backlog could add roughly 340bps to revenue growth; every 1,000bps acceleration in Non-Backlog adds about 500bps.

Capex-Revenue Synergy: The Key to AI Monetization

Google’s Capex expansion translates directly into revenue through backlog growth and AI-driven product adoption.

Recent acquisitions such as Anthropic and Wiz further strengthen its AI capabilities.

Backlog is projected to reach $199 billion by 2025, adding $106 billion YoY and accelerating 2026 growth.

Consensus now expects Google’s 2026 Capex to rise 98% YoY (+$61 billion), and analysts anticipate further upward revisions.

Overall, Google Cloud’s 2026 revenue growth potential exceeds 50%, supporting a target price of $330 and Overweight rating.

The main risk: timing of AI monetization—if token growth decouples from revenue, downside pressure could emerge. However, historical data show that 50–55% of backlog converts to revenue within two years, underpinning a constructive outlook.

Emerging Hardware and Robotics Opportunities

Google’s robotics division (formerly Everyday Robots) was integrated into DeepMind in 2023. The new Gemini Robotics-ER 1.5 model, launched in late September, enables developers to build multimodal, task-adaptive physical agents.

Meanwhile, Waymo continues its global expansion—entering London and adding San Diego, Detroit, and Las Vegas to its U.S. markets by 2026.

With weekly rides exceeding 250,000, Waymo could generate over $5 billion in annual AV revenue, while DeepMind’s robotics AI models could unlock $3 billion in household and industrial applications by 2026.

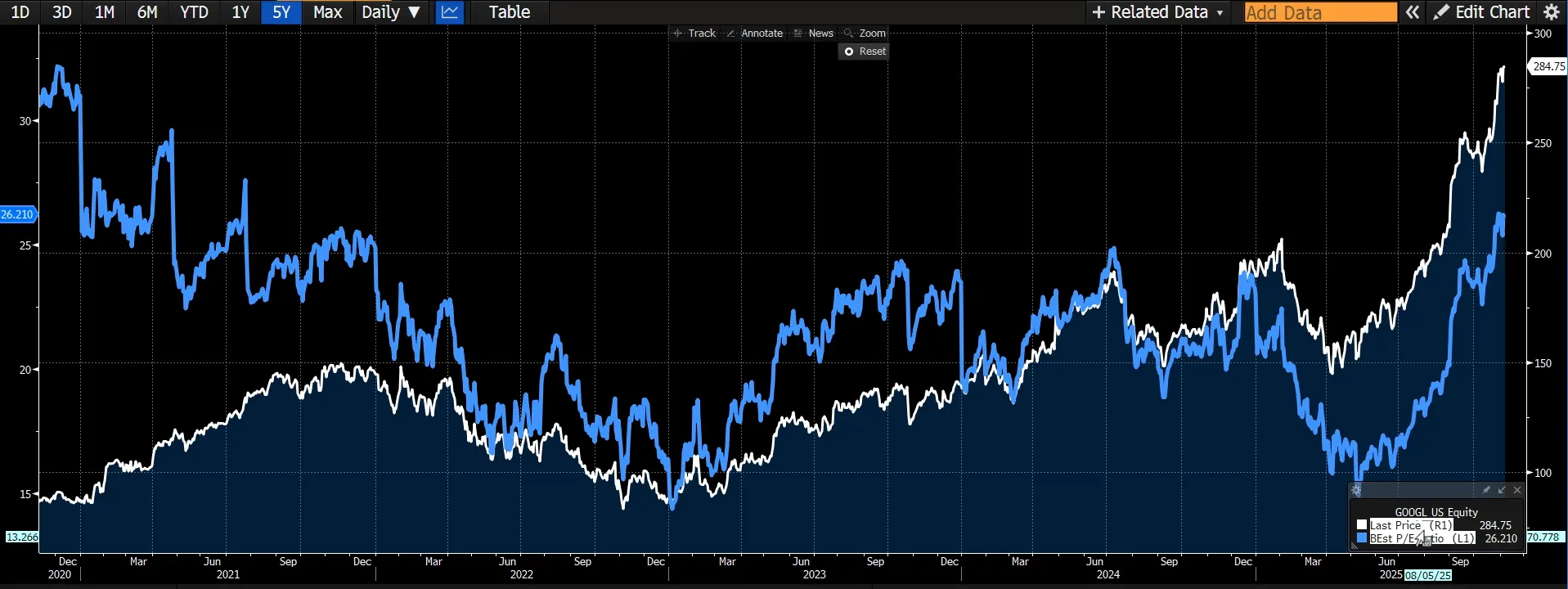

Despite GOOGL’s share price hitting record highs, valuation remains reasonable—back to early-2022 forward PE levels.

Assuming steady growth in Search, accelerated Cloud expansion, and durable AI-driven monetization, a 16x multiple on 2027 EBITDA supports a $330 price target.

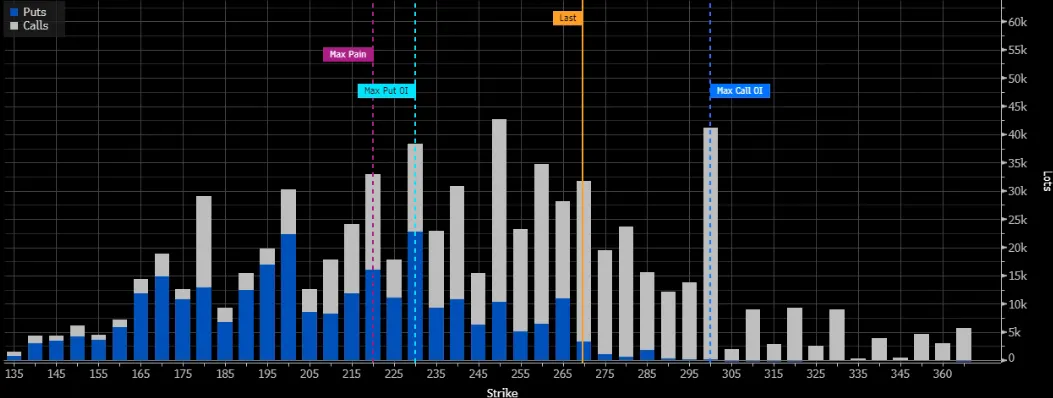

Big Tech Options Strategies

This week’s standout: NVIDIA volatility steals the show, but Apple remains resilient in the recent pullback—supported by robust cash flow and heavy buybacks.

Apple also struck a $1B-per-year deal with Google for customized Gemini model access, enhancing the next-gen Siri/Apple Intelligence capabilities in language understanding, summarization, and planning.

From an options standpoint, the current spot price sits well above the “max pain” level, with traders remaining cautious for the next month.

December open interest shows a heavy concentration of calls around the $300 strike, with notable volumes between $250–270—suggesting continued choppy trading into year-end.

Big Tech Portfolio

The so-called “TANMAMG” equal-weight Big Tech portfolio—tracking the Magnificent Seven (TSLA, AAPL, NVDA, META, AMZN, MSFT, GOOGL)—continues to outperform the S&P 500 by a wide margin.

Since 2015, this basket has delivered a 3,075% total return, versus 292% for the SPY, an alpha of 2,783 percentage points.

In 2025 YTD, Big Tech is again leading the market—+23.77% vs. SPY’s +15.37%—demonstrating that quality growth and balance sheet strength continue to command a premium, even amid rotation and macro uncertainty.

Comments