$Cisco(CSCO)$ a leading provider of networking infrastructure, released its first-quarter financial results for fiscal year 2026, ending October 25, 2025, after market hours on the 12th.

Overall, this earnings report exceeded market expectations. Driven by robust demand for AI infrastructure, the company delivered record-breaking Q1 revenue and profits, while providing optimistic full-year guidance that propelled its stock price higher in after-hours trading. However, beneath the surface of strong growth lie underlying weaknesses in traditional businesses and an unexpected decline in operating cash flow.

Specifically,

Total revenue exceeded expectations, with AI-driven "network" business emerging as the dominant force.

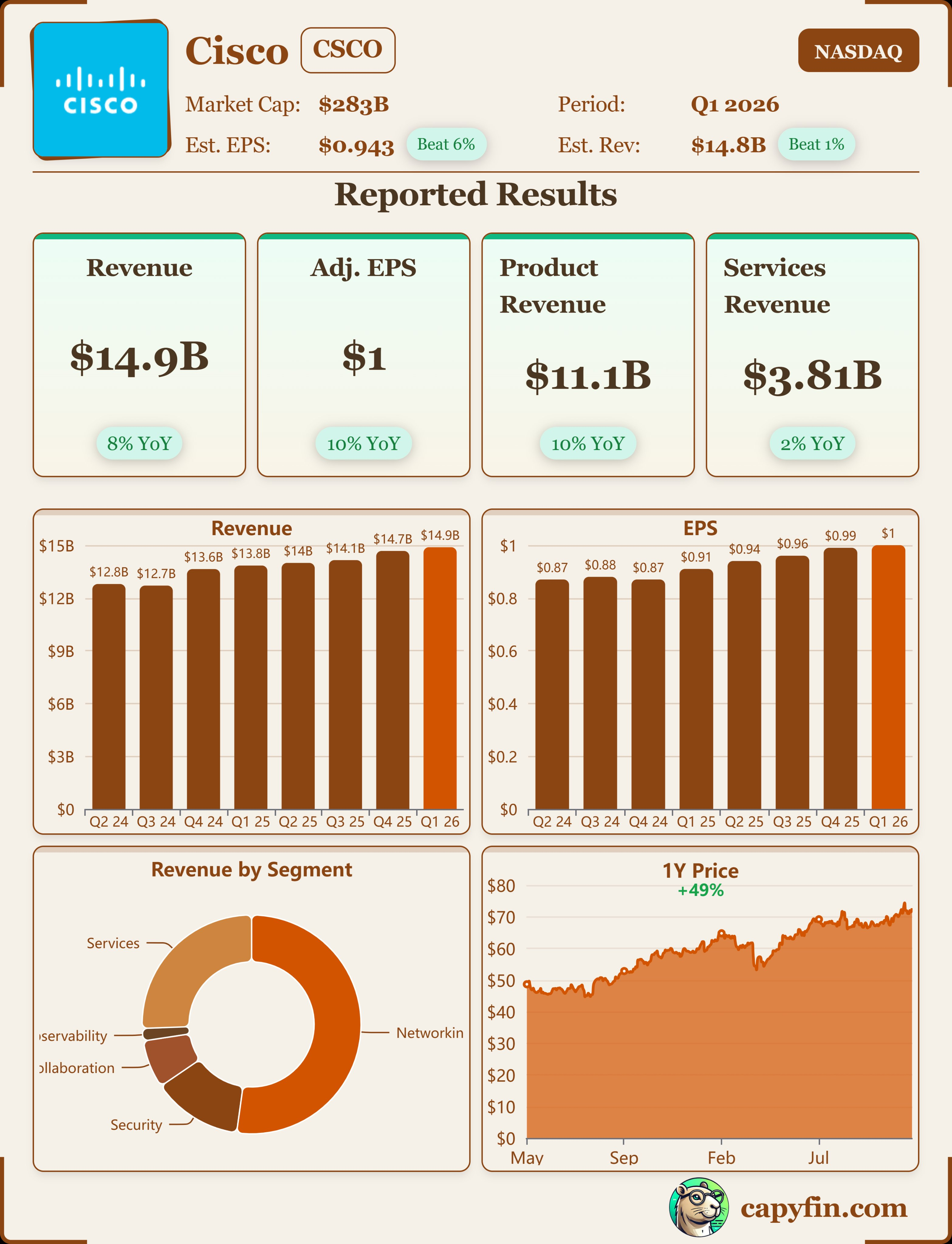

Total revenue for the quarter reached $14.9 billion, an 8% increase year-over-year, exceeding market expectations of $14.77 billion. Non-GAAP earnings per share (EPS) stood at $1.00, a 10% year-over-year increase, also surpassing the consensus estimate of $0.98.

From a structural perspective, growth drivers have shown a marked divergence:

Product revenue grew by 10% year-over-year, serving as the core driver of growth.

Services revenue grew by only 2% year-over-year, reflecting sluggish growth.

Within the product portfolio, the Networking segment delivered the strongest performance, surging 15% year over year. Management emphasized during the earnings call that this growth was primarily driven by AI infrastructure orders from hyperscale customers. This quarter, Cisco secured $1.3 billion in AI orders, demonstrating its robust momentum in AI networking hardware.

Other segments underperformed. Security revenue declined 2% year over year, while Collaboration revenue fell 3%. This indicates that despite Cisco's full-court press toward its AI narrative, its traditional software and services businesses continue to face challenges.

Profit margins showed strong performance, but operating cash flow unexpectedly sounded an alarm.

Benefiting from strong cost control and sales of high-margin products, the company's profitability exceeded guidance.

This quarter, the non-GAAP gross margin reached 68.1%, and the non-GAAP operating margin hit 34.4%, both exceeding the upper bounds of the company's prior guidance. This demonstrates the effectiveness of the company's supply chain optimization and pricing strategies.

However, a concerning signal is that cash flow from operating activities for this quarter amounted to only $3.2 billion, a significant 12% decline compared to the $3.7 billion recorded in the same period last year. Given that net profit grew by 9% year-over-year, this drop in operating cash flow appears particularly jarring. It may indicate some pressure on working capital, suggesting that its health is not entirely satisfactory.

Future orders (RPO) remain robust, with ARR growth steady.

As leading indicators of future revenue, the performance of remaining performance obligations (RPO) and annual recurring revenue (ARR) was solid.

Total RPO reached $42.9 billion, a 7% year-over-year increase. Product RPO grew by 10%, while service RPO increased by 4%. Revenue visibility for the next 1-2 years remains strong, particularly for hardware backlog orders.

Total ARR (Annual Recurring Revenue) reached $31.4 billion, a 5% year-over-year increase. Product ARR grew by 7%. The 5% ARR growth rate is not particularly rapid, indicating the company's software and services transformation remains in a steady transition phase.

Performance Guidance and Management Statements

Cisco management provided strong guidance for the future, demonstrating significant confidence in its AI business:

Q2 FY26 Outlook: Revenue is expected to be between $15.0 billion and $15.2 billion; Non-GAAP EPS is expected to be between $1.01 and $1.03.

FY2026 Full-Year Outlook: Revenue is expected to be between $60.2 billion and $61.0 billion; Non-GAAP EPS is expected to be between $4.08 and $4.14.

The median figures in the guidance exceeded market expectations, serving as a key driver for the stock price increase. During the earnings call, Chairman and CEO Chuck Robbins focused entirely on AI. We believe management is attempting to use the strong growth narrative of AI infrastructure—particularly orders from hyperscalers—to mask weakness in traditional businesses like security and collaboration. The logic behind this messaging is clear: to reposition Cisco from a mature, cyclical networking hardware company into a core beneficiary of the AI era.

Investment Highlights

Overall, this is a strong "Beat-and-Raise" earnings report, with the AI narrative translating into tangible orders and revenue.

The growth structure presents a mixed picture. On the positive side, demand for AI-related high-performance networking hardware (such as Cisco Silicon One) has proven to be a genuine growth engine. The company holds a key position through its Silicon One chips and optical products, and is expected to benefit from the shift in AI workloads from training to inference. The concern is that the security and collaboration (software) businesses, on which the company had pinned high hopes, have instead declined. This downturn in security and collaboration relies more on short-term transition factors—such as the timing impact of Splunk cloud subscriptions—than on structural decline. Once migration is complete, these businesses may return to mid-double-digit growth trajectories.

Strong profit margins are a positive factor. However, the greatest risk lies in the deterioration of operating cash flow. Investors should closely monitor whether this decline represents short-term volatility (such as changes in inventory or accounts receivable) or a trend-driven weakening, as well as the potential for future bond issuances.

Based on the closing price of approximately $71.71 on November 11, the day before the earnings release, and using the median EPS guidance of $4.11 for the company's FY26 full year, Cisco's forward price-to-earnings ratio stands at about 17.5 times.

Given the company's 8% revenue growth and 10% EPS growth, coupled with the robust AI narrative, this valuation level is not expensive. Following the post-earnings stock price increase (approximately +7% to $77 in after-hours trading), its forward P/E ratio will approach 18.7 times, remaining within a reasonable range.

Cisco is successfully capitalizing on the network upgrade cycle driven by AI, but the sustainability of its stock price hinges not only on incremental AI orders but also on its ability to stabilize its core traditional business and swiftly improve its operating cash flow.

Comments

哇。这是件大事。