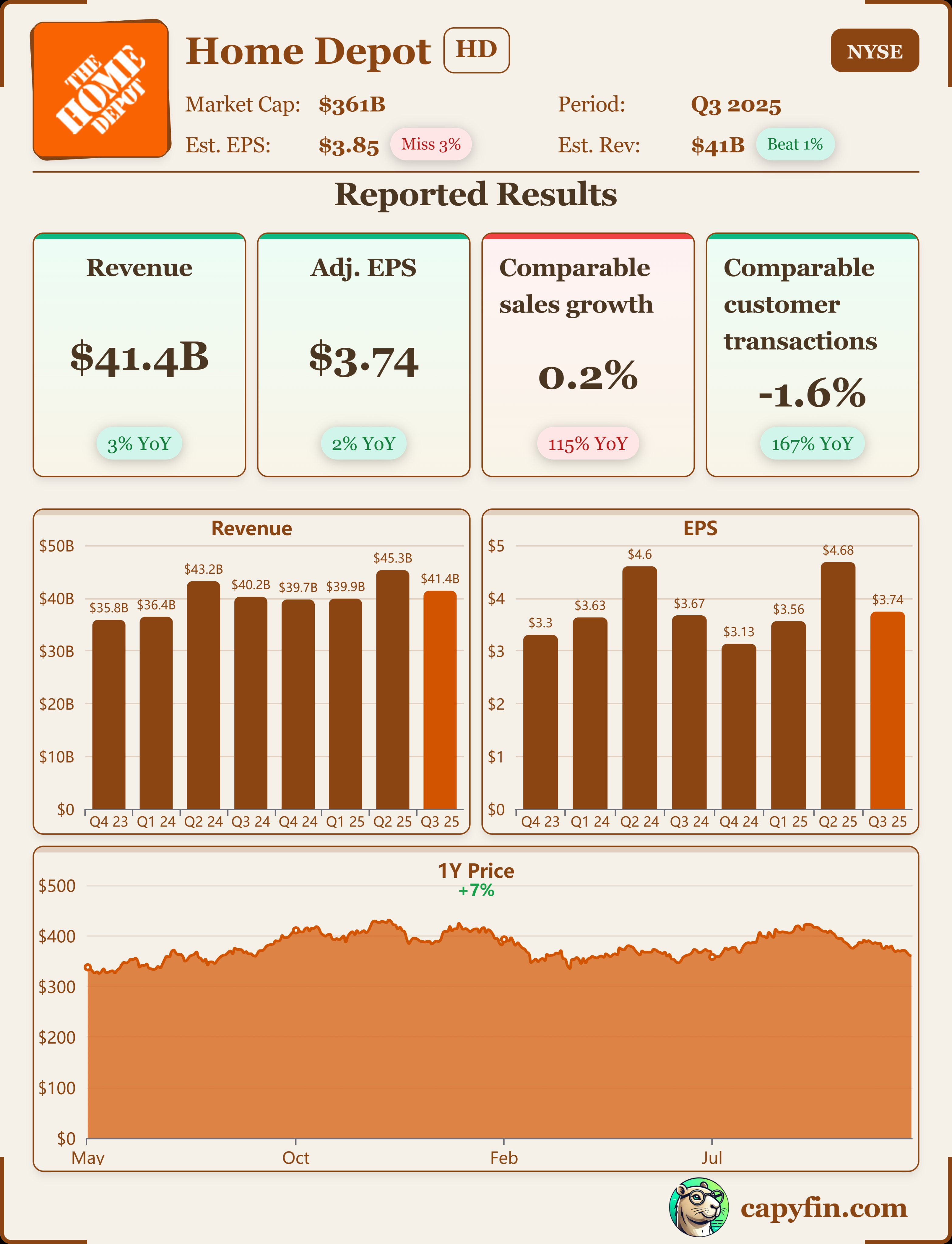

$Home Depot(HD)$ released its third-quarter fiscal 2025 earnings report on November 18, 2025, covering the period ending September 30, 2025. Overall, the company achieved total sales growth, but core comparable store sales remained nearly flat, and profitability declined slightly.

From a macro perspective, the home improvement sector continues to be weighed down by a weak U.S. housing market, high interest rates, and weather-driven demand shortfalls. Specifically: The company's total sales for the quarter reached $41.4 billion, representing approximately 2.8% year-over-year growth; however, comparable store sales increased by only about 0.2%. Diluted earnings per share (EPS) reached $3.62, while adjusted EPS stood at $3.74, slightly below the $3.78 recorded in the same period last year. The company also lowered its full-year earnings guidance, reflecting a cautious outlook on downstream demand. Below is a breakdown of key operational metrics.

Financial Information

The company's total sales for the quarter reached $41.4 billion, representing approximately 2.8% year-over-year growth. Approximately $900 million of this figure stems from the recent acquisition of GMS Inc. (GMS, contributing within 8 weeks), amounting to roughly $900 million. Comparable store sales growth was only 0.2%, with U.S. comparable sales at 0.1%. While total sales achieved positive growth, the core "same-store" business is nearly at a plateau. The contribution from the acquired GMS business was a significant driver of this quarter's growth. Excluding this acquisition impact, comparable growth was nearly negligible, reflecting pressure on the demand side. The home improvement market has yet to show a significant rebound amid high interest rates and a sluggish housing market.

Net income was $3.6 billion, or $3.62 per diluted share, slightly below the $3.67 per share reported in the same period last year. Adjusted earnings per share were $3.74, representing a year-over-year decline of approximately 1.1% (compared to $3.78 per share in the prior-year period). The company disclosed full-year operating margin guidance of approximately 12.6%, with adjusted operating margin guidance around 13.0%. While earnings remained largely flat, they showed a slight decline, with margins facing pressure. From a volume-price perspective: comparable sales volume remained nearly stagnant, and any price increases were insufficient to offset the volume shortfall. Additionally, the short-term impact of merger and acquisition integration (GMS) may lead to increased expenses or diluted profitability, further challenging margins.

GMS sales contributed approximately $900 million over roughly eight weeks this quarter. Management noted during the earnings call that GMS and SRS Distribution, Inc. (SRS) will become growth engines in the future, but face near-term margin compression. For example: Management indicated that following the SRS/GMS integration, the "parent company" margin structure will be compressed by approximately 80 basis points in gross profit and about 40 basis points in operating profit. The acquisition strategy reflects the company's intent to expand further through the "Professional Contractor (Pro)" channel. However, in the near term, integration costs, seasonal fluctuations, and climate-driven demand gaps may delay the realization of promised benefits. Investors should closely monitor the pace of profit realization in these channels.

Management explicitly stated that Q3 results "primarily failed to drive the expected increase in repair/renovation demand due to the absence of storm activity." The company further noted: "We believe consumer uncertainty and persistent pressure in the housing market are disproportionately impacting home improvement demand." The earnings call also highlighted that three key indicators—homeowner turnover rates, home price appreciation, and household formation—are currently under pressure. The home improvement industry is driven by three key cycles: replacement, repair, and new construction. Currently, both new construction and replacement cycles have weakened significantly, while repair demand remains heavily dependent on extreme weather events. Home Depot's underperformance this quarter due to weather-driven demand underscores its business sensitivity to external variables. The macroeconomic environment—characterized by high interest rates, a weakening housing market, and cautious consumers—is exerting pressure on long-term trends.

Full-Year Guidance Update

The company has adjusted its guidance for fiscal year 2025 (52 weeks) as follows:

Total sales are projected to increase by approximately 3.0%. Within this, GMS is expected to contribute an incremental amount of approximately $2 billion.

Comparable sales growth is projected to be "slightly positive."

Gross profit margin is expected to be approximately 33.2%, operating profit margin approximately 12.6%, and adjusted operating profit margin approximately 13.0%.

Tax rate approximately 24.5%; net interest expense approximately $2.3 billion

Diluted earnings per share are expected to decrease by approximately 6% year over year (compared to $14.91 in fiscal year 2024); adjusted earnings per share are projected to decline by about 5% (from $15.24 in fiscal year 2024).

The guidance indicates the company maintains a conservative outlook on full-year profitability, with comparable sales growth remaining modest despite slightly stronger overall sales volume, and potential profit declines. Management also emphasized that the fourth quarter faces triple headwinds from seasonal factors, weather conditions, and a sluggish housing market. Investors should note: the current guidance is based on "slightly positive" comparable sales growth and does not imply accelerating growth.

Key Investment Considerations

Overall, Home Depot remains a leader in the home improvement sector with competitive and scale advantages, but its current performance reflects structural challenges. Our view is as follows:

I. Volume-price structure remains within a cautious range

Comparable sales grew by a mere 0.2%, indicating near-stagnation in core operations. Without M&A activity, growth momentum remains weak. Price increases may be limited as consumers remain cautious about significant renovation expenditures. Should the residential investment cycle fail to improve, the company's growth could remain sluggish for an extended period.

II. Costs and M&A Integration Exert Downward Pressure on Profits

Profit margins have declined slightly, with the acquisition of GMS and integration of SRS operations temporarily weighing on performance. While the company emphasizes market share gains, profitability pressures may persist until "profit realization" occurs. Should subsequent integration efficiency fall short of expectations, risks could rise accordingly.

III. Macroeconomic Risks Cannot Be Overlooked

High interest rates, declining home turnover rates, reduced new construction projects, and fluctuations in weather event frequency all pose potential headwinds to the company's growth. Home Depot's revenue partially relies on repair/renovation demand, which is significantly influenced by weather conditions. Management has explicitly stated that the lack of storm activity has weighed on this quarter's performance. Should such drivers continue to be absent, they will constrain growth over the long term.

IV. Valuation and Investment Logic Require Caution

Assuming the company's adjusted earnings per share (EPS) for fiscal year 2024 is $15.24, with an estimated decline of approximately 5% to around $14.48 for fiscal year 2025. If the market valuation maintains a price-to-earnings (P/E) ratio of approximately 18–20 times, the reasonable share price range would be approximately $260–290 (in USD). Should the valuation compress to 15–17 times, the range would shift to $217–246. Given current housing market risks and slowing growth, valuations may lean toward the lower end. Investors who believe the market has fully priced in risks may consider a medium-term holding; those concerned about further deterioration in the residential cycle should maintain a wait-and-see approach.

In summary, from a structural perspective, Home Depot currently finds itself in a phase of "robustness tempered by underlying concerns." While its scale advantages and brand positioning remain significant, the company is highly susceptible to macroeconomic and industry cyclical influences. Our recommendation is as follows: If you anticipate a mid-cycle recovery in the housing market or believe its Pro channel expansion narrative will materialize, long-term positioning may be considered. If you prioritize short-term earnings stability and growth certainty, we advise maintaining caution or awaiting clearer signs of a market bottom.

Comments