$Novo-Nordisk A/S(NVO)$ Is the ~40% drop in Novo Nordisk ($NVO) justified? 📉

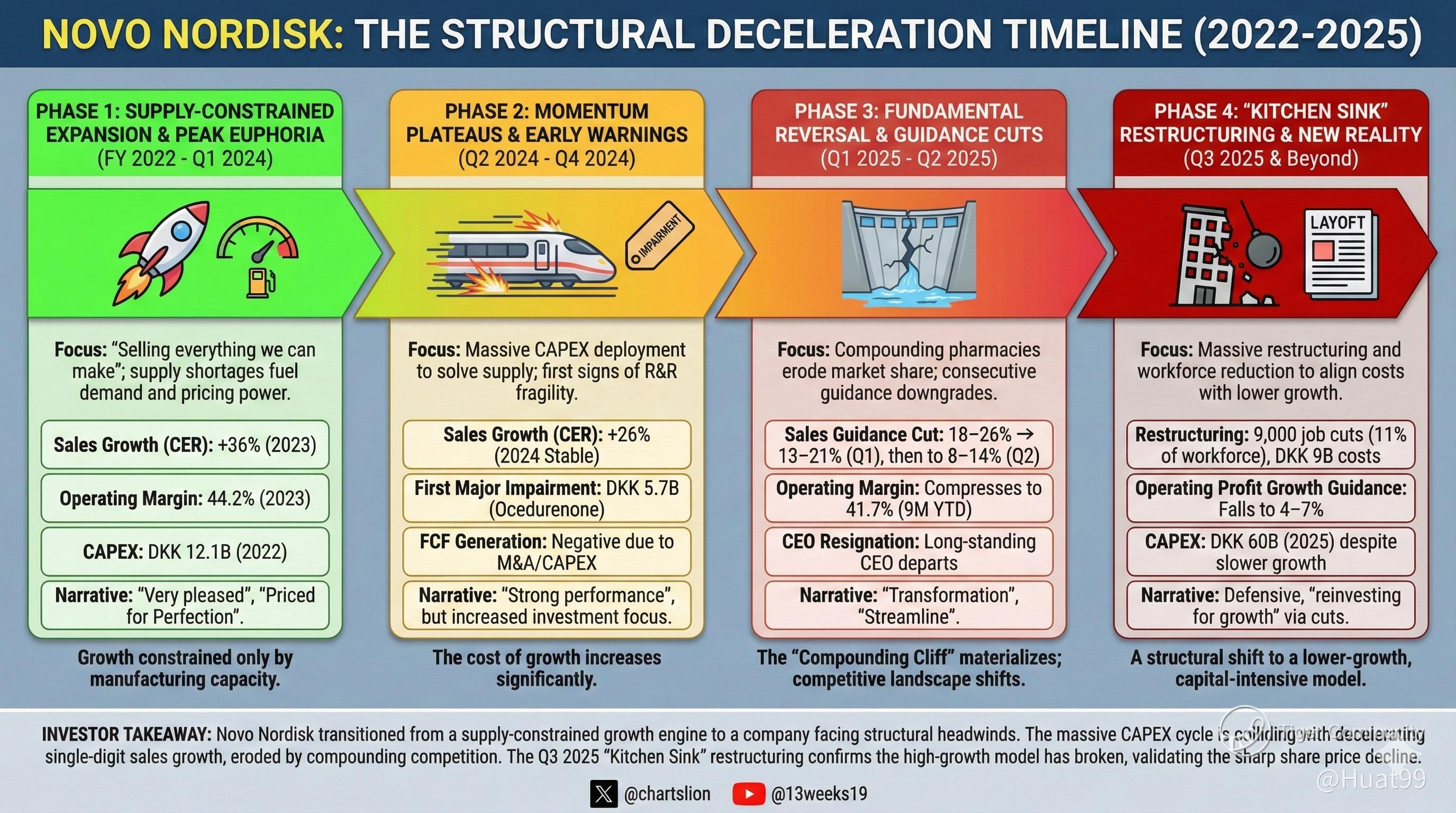

The data confirms a massive "Structural Deceleration."

The timeline from GLP-1 euphoria to a "Kitchen Sink" reality check is brutal:

🚀 Phase 1 (2023): "Priced for Perfection" with +36% sales growth.

🚩 Phase 2 (2024): The "Bull Trap." Sales slow to 26% while impairments (ocedurenone) signal R&D risks.

⚠️ Phase 3 (Early 2025): The "Compounding Cliff." Consecutive guidance cuts start.

🏗️ Phase 4 (Late 2025): The "Reset." 9,000 layoffs and DKK 60B CAPEX collide with single-digit growth.

The high-growth monopoly thesis is broken.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Comments

🚨 6 Jan UPDATE: The $NVO Bear Case just broke.

The Jan 5th launch of Oral Wegovy at $149/mo forces an immediate pivot. The "Compounding Cliff" is dead. 💊

The new reality:

1.Compounding Killer: At $149, NVO undercuts the grey market. Safety + Price = No brainer.

2. Volume Play: They are trading high margins for massive volume (100M+ TAM). Available NOW at 70k+ pharmacies.

Risk shifts from lost share to margin dilution, but the "Avoid" rating is rescinded. If volume explodes in Q1, the bottom is in. Scorecard attached 👇