VTEB: Simple Muni Bond Index ETF, But Better Choices Out There

The $Vanguard Tax-Exempt Bond ETF(VTEB)$ is a simple muni bond index ETF. VTEB's holdings have extremely low credit risk, moderate interest rate risk, and its dividends are tax-exempt. On the other hand, dividends are quite low, with the fund sporting a TTM dividend yield of only 2.1%, and an SEC yield / forward yield of 3.0%.

In my opinion, although VTEB seems like a reasonable investment for more conservative investors wishing to minimize their tax burdens, the fund's overall value proposition is not very compelling. Several investments offer broadly superior, although not identical, value propositions to VTEB. As such, I would not be investing in the fund at the present time.

VTEB - Overview

VTEB is a muni bond index ETF, tracking the Standard & Poor’s National AMT-Free Municipal Bond Index. It is a relatively simple index, including all relevant investment-grade, tax-exempt muni bonds in the market. As with most indexes, applicable securities must also meet a basic set of inclusion criteria to be included in the index. Due to the large size of the muni bond market, VTEB invests in a representative sample of its underlying index, meant to match key benchmark characteristics. VTEB invests in 6930 bonds, more than enough to ensure a representative sample and adequate diversification, in my opinion at least. It is a market-value weighted index, equivalent to a market-cap weighting scheme but for bonds.

VTEB provides diversified exposure to tax-exempt muni bonds, with investments in 6930 of these, from dozens of states. VTEB is more than sufficiently diversified for a muni bond fund, but it does not provide the diversification broader bond funds do, those with exposure to other bond sub-asset classes.

VTEB invests in bonds of all relevant maturities, with an average maturity of 13.5 years, and average duration of 5.9 years.

VTEB's duration and interest rate risk are slightly below-average, so expect moderate, slightly below-average, losses during periods of rising interest rates. VTEB itself saw moderate losses during 2022, a period of rapidly rising interest rates, as expected. On the other hand, the fund fared quite a bit better than average, somewhat exceeding expectations. It is my understanding that muni bond durations exaggerate their interest rate risk, due to their structures/convexity, although I don't have sufficient data to be 100% certain of this. Still, it seems that VTEB's interest rate risk is somewhat below-average.

VTEB almost exclusively invests in investment-grade muni bonds, with an average / median credit rating of AA.

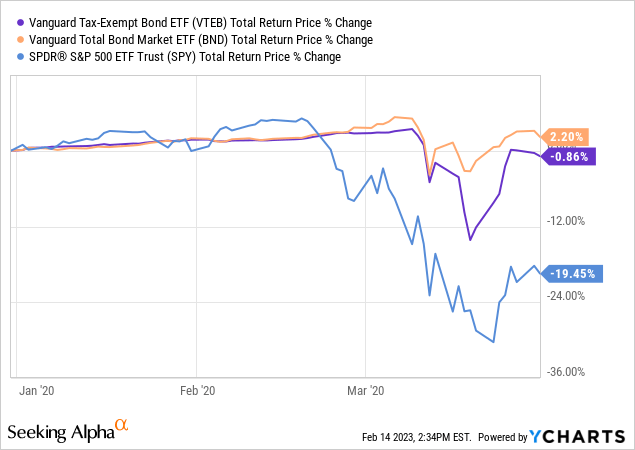

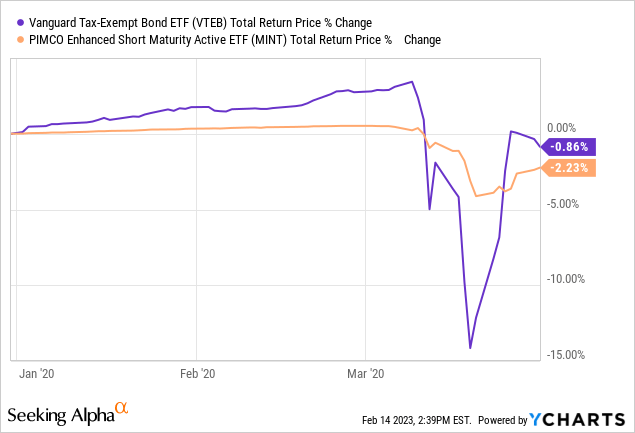

VTEB's underlying holdings have strong credit ratings, indicative of resilient issuers with ample, proven capacity to pay. Default rates are incredibly low, and repayment is to be expected, even during downturns and recessions. As per Moody's, investment-grade bonds cumulative default rates over ten-year periods average 0.09%, or less than 0.01% per year. These are incredibly safe securities, so expect extremely low losses during downturns and recessions, as was the case in 1Q2020, the onset of the coronavirus pandemic.

Data by YCharts

VTEB's safe, low-risk holdings are an important positive for the fund and its shareholders.

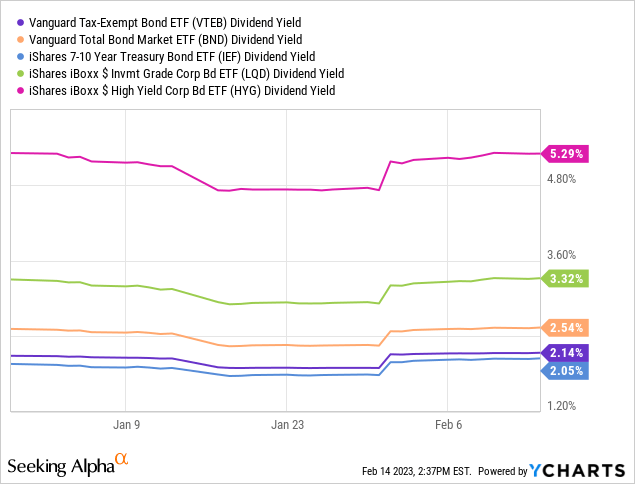

On a more negative note, safe investments tend to be low-yielding investments, and VTEB is no exception. The fund sports a TTM dividend yield of only 2.1%, incredibly low on an absolute basis, and lower than that of most bonds and bond sub-asset classes. Only treasury ETFs yield less, and barely so.

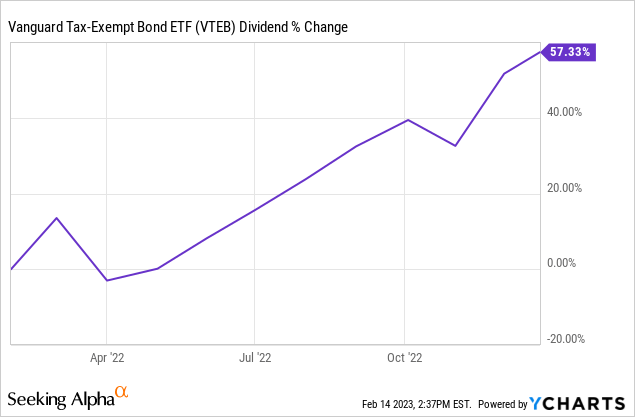

On a more positive note, VTEB's dividends and dividend yield will both likely see some growth in the coming months, courtesy of Federal Reserve rate hikes. Higher Fed rates mean higher muni bond interest rates, which means higher income for the fund, which ultimately results in higher dividends for the fund's shareholders. The process is slow and gradual, but has already started, with fund dividends growing over 57% in 2022.

VTEB's dividends should grow until the fund is yielding around 3.0%, equivalent to its SEC yield, a standardized measure of a fund's underlying generation of income. Although this is quite a bit higher than the fund's current dividend yield, it is still a relatively low figure on an absolute and relative basis.

VTEB focuses on tax-exempt muni bonds, which are exempt from federal income taxes. This is a significant, straightforward benefit for investors, and particularly impactful for investors in higher tax brackets, who could significantly reduce their tax bill by investing in VTEB over other funds.

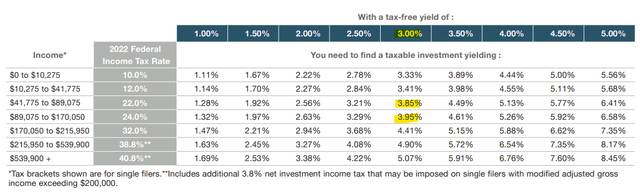

The specific magnitude or impact of these savings is dependent on dividends received, federal income tax rates, and the specific circumstances of each individual investor. These specific issues are outside the scope of this article, but I'll provide a quick table of tax-equivalent yields that might be of use. In simple terms, the table lets you compare tax-free yields with equivalent taxable yields depending on your tax rate. VTEB's 3.1% SEC yield is equivalent to a 4.0% taxable yield for most investors, although figures do vary depending on an investor's tax bracket.

Although a taxable equivalent yield of 4.0% is a bit more respectable than a 3.1% yield, it is still quite low, and compares unfavorably to several other investments and asset classes. Let's have a quick look at some of these.

Quick Asset Class Comparison

T-Bills

T-bills have effectively nil credit risk, barring an unprecedented U.S. government default. VTEB's muni bonds have slightly more credit risk, but still quite low on an absolute basis.

T-bills have maturities of up to three months, so interest rate risk is incredibly low. VTEB's muni bonds have longer maturities, and so interest rate risk is appreciably higher, although still below-average.

T-bill asset values are incredibly stable, if bought individually or through ETFs. VTEB's share price does fluctuate a bit, much more than a T-bill.

T-bills currently yield +4.5%, quite a bit more than VTEB's 2.0% TTM dividend yield, and 3.0% SEC yield. Tax benefits might make VTEB a more compelling choice for investors in the higher tax brackets.

T-bills yield more than VTEB, and are safer, more stable assets to boot. Under these conditions, I see no reason to invest in VTEB over a T-bill.

MINT

There are several short-term bond fund ETFs with stronger value propositions than VTEB out there, including the PIMCO Enhanced Short Maturity Active Exchange-$PIMCO Enhanced Short Maturity Exchange-Traded Fund(MINT)$ .

MINT focuses on investment-grade bonds, so credit risk is low. VTEB's credit risk is somewhat lower, as muni bonds themselves have lower default rates than average. Both funds should perform reasonably well during downturns and recessions, but MINT's losses should be a little bit higher, as was the case in 1Q2020.

MINT focuses on short-term bonds, so interest rate risk is quite a bit lower relative to VTEB. Expect significant outperformance from MINT during periods of rising interest rates, as was the case in 2022.

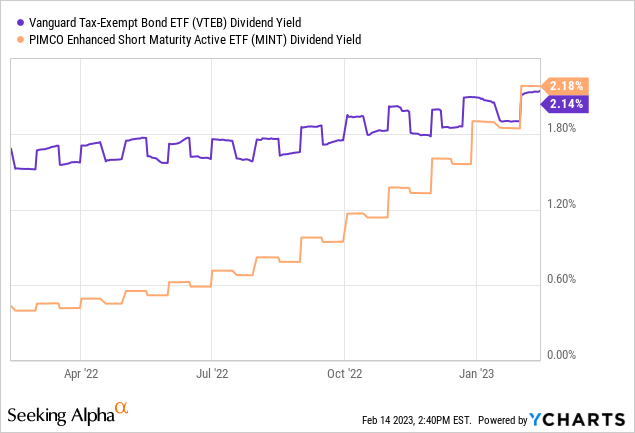

Both funds have very similar dividend yields, with MINT yielding 2.2%, and VTEB yielding 2.1%. On the other hand, as MINT focuses on short-term bonds, the fund can quickly replace its portfolio when interest rates rise, leading to very fast dividend growth during periods of rising interest rates. MINT's dividends grew much faster than VTEB's during 2022, for instance.

Due to the above, MINT will almost certainly yield more than VTEB moving forward. MINT currently sports an SEC yield of 4.6%, quite a bit higher than VTEB's 3.1% SEC yield, or its 4.0% taxable equivalent. MINT will likely yield more than VTEB moving forward even after accounting for VTEB's tax benefits.

In my opinion, MINT's overall value proposition is much more compelling than VTEB's. As such, I see no reason to invest in VTEB over MINT.

As a final point, VTEB would compare unfavorably to several other asset classes and funds, including CDs, I-bonds, and the$JPMorgan Ultra-Short Income ETF(JPST)$ . T-bills and MINT are representative examples of this. VTEB ETF simply yields too little to be a worthwhile investment opportunity, in my opinion at least.

Conclusion

VTEB is a simple muni bond index ETF. Although VTEB has its benefits, the fund's overall value proposition is not very compelling. As such, I would not be investing in the fund at the present time.

Source : VTEB: Simple Muni Bond Index ETF, But Better Choices Out There (NYSEARCA:VTEB) | Seeking Alpha

Comments