$Walt Disney(DIS)$ Surprise gift, the financial report for the third quarter of fiscal year 2021 ending July 3, basically announced its best entertainment company in the US stock market in the coming year.

Overall performance turned losses into profits

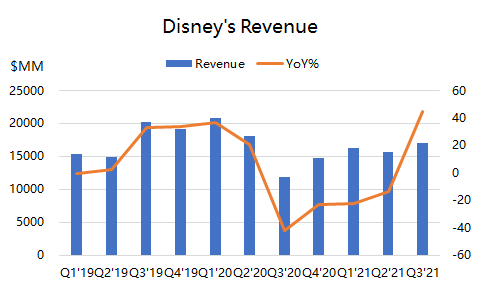

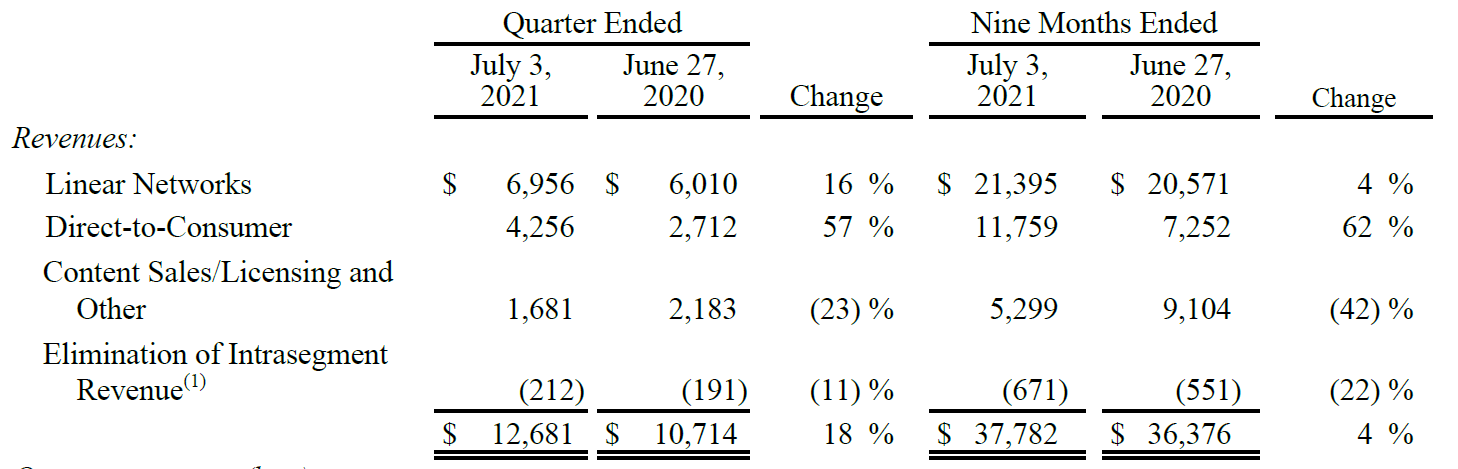

The total revenue was US $17.022 billion, an increase of 44.5% year-on-year. After all, the base was low due to the epidemic in the same period last year, and it did not return to the level of 2019 for the time being. However, this figure exceeded the consensus forecast of $16.76 billion on Wall Street.

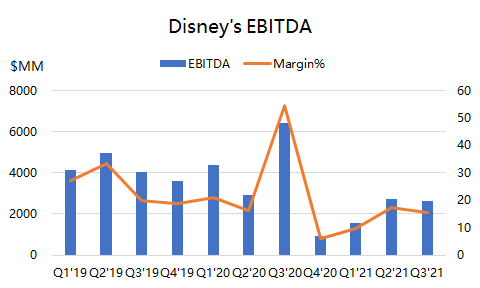

The adjusted EBITDA is 2.62 billion US dollars, with a profit margin of 15.4%;The net profit was US $1.123 billion, compared with the loss of US $4.721 billion in the same period last year.The corresponding EPS is 80 cents, while Wall Street unanimously expects 55 cents.

This shows that the impact of the epidemic on the company has gradually passed, and the company executives also said that most of the business will return to normal by the end of 21.

Streaming media crash?

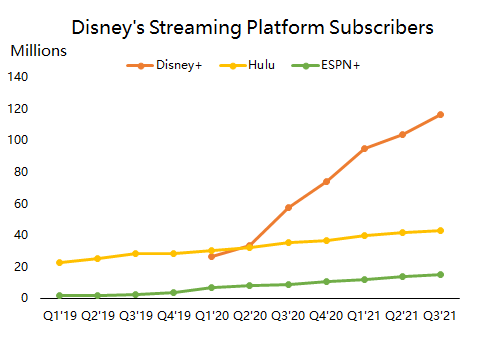

Walt Disney's online business is Disney +, which is the most powerful streaming media to catch up with Netflix.Disney + subscribers reached 116 million this quarter, up 101.7% year-on-year, is still in the outbreak period.

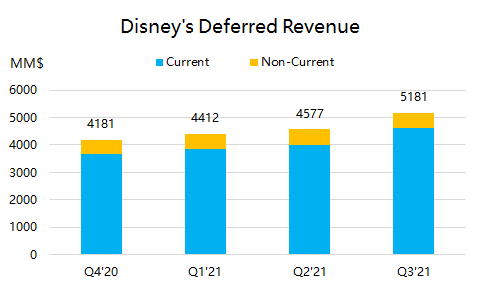

One thing or two can be seen from the deferred income of the company,The current deferred income is 25% more than last year's Q4, up 15% from the previous quarter.

Disney + 's success, on the one hand, is based on Walt DisneyPowerful content systemFor example, Marvel Universe contributed super dramas such as Wanda Vision, Falcon and Winter Soldier and Rocky in Q3. On the other hand, Walt Disney tried Premier Access in an unprecedented way, which willMovies shown in traditional cinemas are also online on streaming mediaFor example, "Black and White Witch Kuira", "Legend of Seeking Dragons" and so on. The Marvel blockbuster "Black Widow" is also launched in Disney +, but it does not belong to this quarter's financial report. It is mainly this way of online and offline simultaneous screening, and also considers the special situation during the epidemic period, and tries the business model of maximizing profits.

Of course, traditional media businesses, such as cable TV programs such as ESPN and ABC, earned 6.9 billion US dollars in revenue this quarter, up 16% year-on-year, which was the fastest growing quarter in recent years, but it was mainly due to the low base during the epidemic last year. If it is extended to 9 months, the year-on-year growth rate will be 4%, which is still the bulk of the company's revenue. Although the advertising unit price of cable programs has increased, the overall cable business is still in a downward trend, which is an industry trend. Therefore, the company does not rely on this business, and actively transforms, such as launching ESPN + streaming media, which has reached 14.9 million subscriptions this quarter. Watching sports programs through streaming media will soon become a trend, and ESPN + is expected to get higher income in Q4 Olympic season.

Hulu, another joint venture streaming media, has 42.8 million users. Although the number of users is also growing steadily, there is no momentum to explode. To a certain extent,Disney + also creates competition for Hulu, and the synergy between the two parties is not large enough.However, Walt Disney's positioning of Hulu may be more to make it develop steadily. After all, there is no need to bet on multiple lines of business.

However, compared with the whole industry, Walt Disney's growth in streaming media has been irresistible, and the content is richIt has already put pressure on peers such as Netflix. The weakness of Netflix's financial report this quarter is not necessarily the fatigue of Netflix's own content, but the relatively fierce competition in the content industry, which shows that Netflix's content is not brilliant enough this season. This kind of competition will be strengthened in the future.

However, we are also full of confidence in the content of Walt Disney in 2022."Doctor Strange 2" with the Scarlet Witch, "Thor 4" with Guardians of the Galaxy, "Panther 2" with the late star and the new film "Eternal Family" by Chinese directors. Among them, "Doctor Strange 2" is the opening content of unlocking the important plot of the multiverse after "Avengers 4".

Offline business recovers faster than expected

Offline parks were considered to be one of the worst-hit businesses last year, but they were easily overcome by Walt Disney.

Walt Disney's six parks are located in Los Angeles, Orlando, Tokyo, Paris, Hong Kong and Shanghai. Among them, Tokyo is a joint venture, which can not only collect stable licensing fees, but also share profits, but also receive less losses under the epidemic situation. This year's Olympic Games was forcibly opened in the epidemic, and there were almost no global tourists, and there was no growth. This park can eat its old money.

Paris Park has always lost money, so although the epidemic has a great impact and the opening days are not many, it will not be any worse than the historical performance.

Hong Kong Park is probably the most influential, because it mainly carries tourists from Southeast Asia and China. However, after some events, Hong Kong Paradise is not very attractive, and it is a park with weak growth.The most important thing is the Shanghai Park. Thanks to the excellent epidemic control in China, the performance of Shanghai Walt Disney Park has explodedSo much so that Walt Disney is ready to raise prices.

In the two parks in the United States, the business is still hot against the epidemic, and the control in California is slightly stricter, but the one in Orlando has almost recovered to the level before the epidemic. Of course, this is also due to the company's Magic Key annual membership plan, which gives tourists more choices to visit many times.

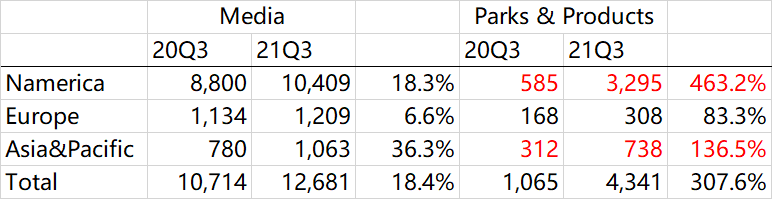

In terms of revenue by geographical location, the revenue of parks and product types in North America increased by 463% year-on-year, and that in Asia-Pacific increased by 136% year-on-year. This also makes the overall revenue of offline theme park business reach 4.34 billion US dollars, and at the same time generates operating profit of 356 million US dollars, turning losses into profits.

In addition, in terms of consumer goods sales, Walt Disney's performance also exceeded expectations. The growth of merchandise and licensing and retail business was mainly due to the strong sales based on related IP. For example, there was news that Dailu doll, a Mid-Autumn Festival star in 300 yuan, Walt Disney Province, was fired for thousands of dollars.

Walt Disney's valuation logic has changed

Most investors pay special attention to the index of "P/E ratio" PE when looking at individual stocks. However, for some comprehensive and complex companies, it is difficult to correctly understand the valuation of this company simply by looking at PE.

In the past, Walt Disney was a company that silently relied on traditional online media and offline parks to eat dividends during economic recovery and prosperity, with considerable profits. Not only was the company's price-earnings ratio easy to observe and explain, but it also paid dividends to shareholders or bought back shares.

However, in the past two years, the streaming media has changed and the epidemic situation has changed on a large scale, which makes Walt Disney's valuation logic no longer so simple. Valuation methods vary widely among different businesses. 【小于】 /P >

DTC business with Disney + is not suitable for valuation with profit multiples, but shouldValued according to the revenue multiple of the corresponding streaming media industryEven if it is only 10 times PS higher than the industry average, it will be much higher than the previous valuation.

For other traditional businesses and offline park businesses, the level after the epidemic recovery should be considered, and the profit multiple should be valued.

If it is 10 times the income multiple of DTC business (PS) and 16 times the profit multiple of other businesses, the value per share in 2022 will reach 220 US dollars.

Of course, if Walt Disney can continue to raise the price of Disney +, park tickets, goods sold and advertisements on the basis of maintaining growth, then this result may still be conservative.

Comments