Under the news of raising the forecast of fiscal year 2021, CVS share price reached a 52-week high yesterday, only one step away from the all-time high. As the largest pharmaceutical retailer brand in the United States, CVS's performance benefited from the epidemic. Improving performance guidance is the current booster, and it can also resist inflation from a longer perspective.$CVS Health(CVS)$

Introduction

CVS Health Corporation (NYSE:CVS) has quickly evolved into more than just a convenient place to fill your prescriptions and pick up some toilet paper while you're there. Since 2017, when they announced what would become known as thelargest healthcare merger in U.S. historywith Aetna, CVS Health has transformed itself into a true giant in the healthcare industry. They now find themselves in the rather unique position of capturing profits through an interconnected array of services. The addition of "health hubs" in many of their stores is the final piece which will allow them to unlock their true earning power. I find the future being laid out for CVS to be quite attractive and believe now represents a great time to buy shares for the long term.

Company Overview

CVS derives revenue from three main segments. These include the company's newest addition Aetna, which provides health benefits and managed care to over 23 million members, making them the third-largest health insurer in the United States. Having such a large market share affords CVS the ability to offer lower cost, as well as a wider array of benefits, to current and would-be members. Their size also attracts more service providers, such as physicians and hospitals, willing to offer CVS lower prices in order to have access to their large customer base.

Then there isCVS' Caremark division, a pharmacy benefit manager (PBM) working behind the scenes for health insurers, Medicare, and large employers to negotiate with manufacturers and pharmacies for the best pricing on prescription drugs. Caremark essentially determines how much they are going to pay the pharmacies to fill prescriptions.

Which leads me to CVS' final segment, retail pharmacy. CVS currently owns and operates just shy of 10,000 stores. Building on what is referred to as "Minute Clinics", 1500 stores now have what is known as "Health Hubs". Health Hubs aim to be more staff intensive and focus on treating chronic diseases such as diabetes and sleep apnea, as well as behavioral and mental health conditions. These health hubs tend tolead to more foot traffic, front-of-store sales, and prescriptions dispensed.

I would also mention that Covid-19 has been somewhat of a tailwind for CVS Health through Covid-19 testing, of which CVS isAmerica's largest private provider, as well as through the administration of over 43 million vaccines to date. This has led CVS to capture and retain many new customers, as12.5% of new customers testedfor Covid-19 have chosen to fill a prescription or receive vaccinations through CVS Health. Originally it was thought that the widespread use of vaccines would put a swift end to Covid-19, but new strains continue to evolve, such as that of Delta and Omicron. While I'm sure we would all like to see an end to this deadly disease as soon as possible, it appears that CVS will be administering testing and vaccinations longer than anticipated.

By the Numbers

Q3 2021 sawCVS Health beat top-line resultsby a healthy $3.27B, with total revenue of $73.8B, representing 10% YOY growth. While Non-GAAP EPS of $1.97, which equates to 18.6% YOY growth, beat analyst expectations by $0.18. Management is aiming for sustainable,low double-digit, bottom-line growth, starting in 2024.

Free cash flow (FCF) came in at $4.9B for the quarter. This compares quite favorably to FCF of $1.3B in Q3 2020. Over the trailing twelve-month period, CVS has had a massive free cash flow of $15.2B. CVS Health expects revenues of $286.5B to $290.3B for FY2021, representing growth of 6.2% to 7.5%. FY2021 adjusted earnings per share of $7.90B to $8.0B, if met, would equate to growth of 5.3% to 6.67%.

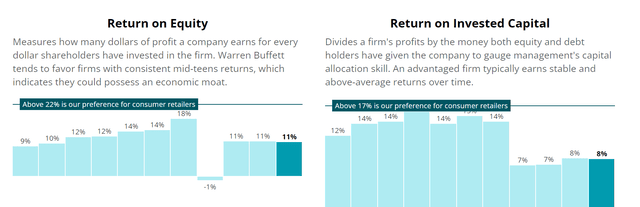

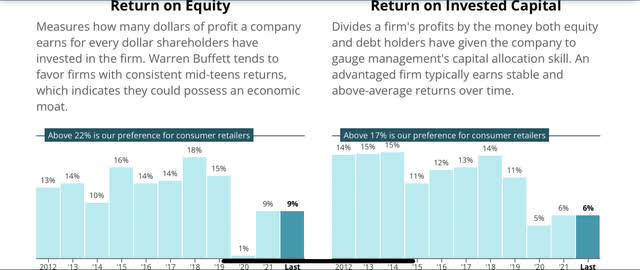

Since closing the Aetna merger in 2018, CVS took a major hit to their return on equity and return on invested capital, as their debt load skyrocketed. Yet both metrics have been trending up as they have consistently paid down debt.

Valuation

CVS closed yesterday at $98.86 on a mixed price-earnings ratio of 13.29 times. On the basis of valuation, this is better than their average P/E ratio of 13.77 times in 10 years and 15.66 times in 20 years. Analysts expect earnings per share to rise by 3pc in 2022 and 8pc in 2023. This will all become supporting stocksArguments for upward price.

Competitive Advantage

CVS Health has taken their business to another level with their blockbuster acquisitions of Caremark and Aetna. No longer are they dependent strictly on the retail side of things, as their revenues are split almost evenly between their retail business, Caremark's PBM division, and Aetna's health insurance. Each segment is surrounded by their own moats, giving them a durable, competitive advantage over their competition. These moats mainly take the form of cost advantages and network effects which essentially go hand in hand. The larger their network becomes, the more negotiating power they have, which in turn allows them to offer lower prices and better benefits. This creates a virtuous cycle that sees CVS continue to expand and grow their business.

While the Amazon effect has many companies backfilling their moats, CVS may prove immune. While CVS offersfree prescription delivery, the majority of customers still prefer to pick up prescriptions in-store. Also, the implementation of health hubs will keep customers more reliant on in-store visits to receive care in the form of check-ups, vaccinations, and maintenance of chronic diseases. Most of these services would be very difficult to replicate any way other than in-person visits.

Peer Comparison

Walgreens Boots Alliance (NASDAQ:WBA) is CVS Health's largest competitor in their retail and pharmacy divisions. CVS and Walgreens both operate over 9,000 stores in the U.S. and arenumbers 1 and 2 respectivelyas far as market share goes, based on prescription drug revenue. Both businesses will look to combat e-commerce with the implementation of care clinics in their store which should keep more customers reliant on in-store visits. Where CVS holds the advantage is that each of their three segments only accounts forroughly one-third of revenue, while Walgreens relies heavily on their retail stores, with around three-fourths of their revenue coming from their pharmacy segment. While CVS has seen their earnings per share and free cash flow per share consistently rise higher over the years, Walgreens has found itself on a downward trend in these categories, which has resulted in lower ROE and ROIC than CVS at 9% and 6% respectively.$Walgreens Boots Alliance(WBA)$

This may have played a part in their most recentdividend raise in July of only 2.1%as compared to CVS' 10% raise this month. Overall, the future just looks much brighter for CVS, which is backed up by their outperformance over Walgreens over the past year.

Key Decisions

After the merger with Aetna, CVS' management made the decision to freeze their dividend and buybacks, and instead focus on paying down the large debt taken on in this merger. Not only did this show that management wasn't focusing on short-term share movements, or the typical pay bonus that comes with this, but instead they were determined to act in a manner that was best for the long-term viability of CVS Health by making smart, responsible decisions.

It was also announced recently thatCVS has plans to close 900 stores, at a rate of 300 a year for the next 3 years. This works out to right around 9% of their total store count and is aimed at reducing store density. Many of the remaining stores will be updated to reflect their new strategy, which includes offering more health services through the addition of "health hubs". If these hubs are as effective as management seems to believe, and as many stores are beginning to show, then that could be a major boon for the company as a whole. The benefits to these health hubs are glaringly obvious, as they could effectively benefit each segment of CVS Health. Not only will they drive more foot traffic to their stores for doctor visits, which in turn will lead to more prescriptions being filled as well as more front-of-store purchases, but they can also use these formats to offer more benefits aimed at attracting a higher number of Aetna members to frequent CVS stores, while incentivizing non-members to sign up for their health insurance.

Another change you may have noticed in stores is the addition of self-checkout machines. SinceCVS recently raised their minimum wage to $15, this would seem to be an obvious next step to keeping only their best workers and using technology to replace the rest. This is just one of the ways recently that CVS has shown their willingness to use technology in order to advance their business. Last year CVS announced they wereteaming up with UPSin using drones to deliver prescriptions directly to homes, and more recently they have announced intentions tobegin working with Microsoft, using their cloud service Azure in order to enhance capabilities of machine learning and customized health. Over time this should lead to higher margins, and in turn greater profits.

Comments