Big banks performed well in 2021, and the US banking index$KBW Regional Banking Index(KRX)$ rose 33% for a whole year, outperforming S&P (27%).

All five major banks have announced their fourth-quarter financial reports. In view of the general decline in trading income and the market concerns that large banks may weaken their profits next year due to cost problems, banks all fell sharply in recent days.

Q4 Earnings season started under the background of high inflation and interest rate hikes, and the market focus more on earnings instead of valuation.Banks wil go upward differentially due to business structure and cost control.

Under the environment of raising interest rates, the current market is facing a situation of "double killing" of valuation and earnings. Investors can't ignore the matching degree between eanings and growth rate, whether it is value stocks or technology stocks.

So, what are the noteworthy in Q4 financial report?

1.The trading income of the five major banks all missed market expectation

The fluctuation of the market reflected by the trading business of the bank. In the first half of the year 2021,trading banks outperformed consumer banks as a whole, since the second half of the year, the trading enthusiasm has dropped from a high level, and both fixed-income business and stock trading business have declined to varying degrees, but the stock trading business is still stronger than FICC, which is consistent with previous judgments.

From the perspective of this quarter, bank trading income was more dragged down by FICC business. that is, debt, foreign exchange and commodity trading declined significantly, and banks such as $JPMorgan Chase(JPM)$And$Citigroup(C)$,whose FICC accounting for a relatively high proportion is affected seriously.$Goldman Sachs(GS)$FICC's business performance is the best among its peers.$Bank of America(BAC)$And Goldman Sachs' FICC revenue fell less than JPMorgan Chase,$Morgan Stanley(MS)$And Citigroup's 10-20% decline.

On the contrary, the income from stock trading is relatively resistant to decline, but only Morgan Stanley has a positive year-on-year growth.On the whole, the scale of stock trading remained at a relatively high level.

The prosperity of trading comes from the high volatility throughout the year, which has certain periodicity. Looking ahead to 2022, although this fluctuation will not plummet, the overall amplitude will converge.

2. The investment banking business maintained a high prosperity throughout the year

In 2021, IPO activities boosted investment banking revenue among big banks. According to the statistics of Refinitiv, after deducting the Special Purpose Acquisition Company (SPAC), there were 2,097 IPOs in 2021, raising a total of 402 billion US dollars. Compared with 2020, the amount of fund-raising increased by 81% and the amount increased by 51%.

In the fourth quarter, the income of investment banks of Goldman Sachs, JP Morgan Chase, Citigroup and Bank of America all exceeded expectations, while Goldman Sachs, JP Morgan Chase and Citigroup led in absolute income, with a year-on-year increase of 30-40%. Morgan Stanley is the only company whose investment banking revenue growth rate is lower than that of the same period of last year. If we look at it from a longer perspective, the investment banking revenue of Morgan Stanley also achieved a high growth rate of 43% last year, setting a record.

Similar to trading business, there are hidden worries behind the high enthusiasm. The risk points of investment banking business mainly come from cross-border regulatory risks and liquidity tightening expectations. The cooling of IPO market in 2022 is also a high probability event, and M&A financing activities will be significantly reduced.

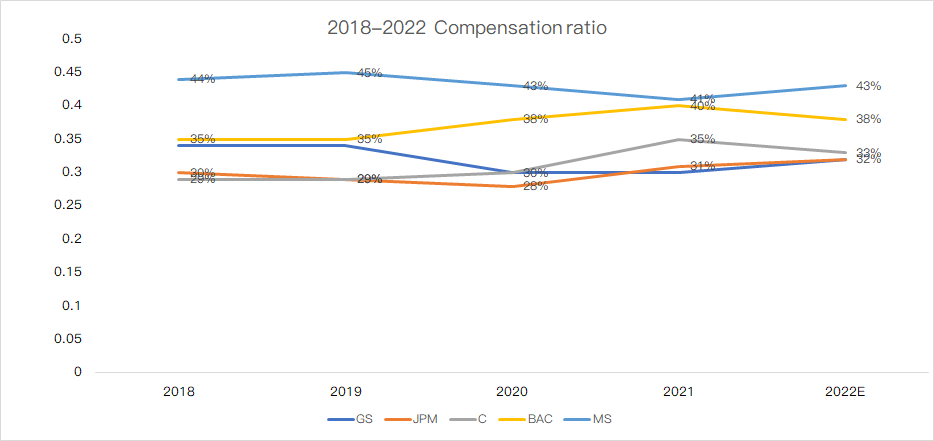

3. Profits are restricted by multiple factors, and the battle for talents is on the verge

This quarter, the common problem among banks is the erosion of profits due to high operating expenses. In the past year, the five major investment banks competed to raise salaries, paying employees a total of about 142 billion US dollars, an increase of 18 billion US dollars over 2020,nearly 15% increase year-on-year.

At present, the rising labor cost exposed by JP Morgan Chase and Goldman Sachs is not an industry-wide trend.The salary impact on each enterprise is different, which is related to the salary policy and salary structure of each enterprise.

Salary levels of Goldman Sachs, Morgan Stanley, including Credit Suisse and Deutsche Bank are still lower than 2020. Compared with their peers, trading banks are more focused on capital market, wealth and asset management, and have a solid talent reserve. Even if the pressure of labor cost exists, it will not excessively weaken profits.

For example, although Morgan Stanley has the highest compensation ratio among five major banks, and the salary expenditure of Q4 reaches 5.487 billion US dollars, it is still basically the same as that of the same period of last year, significantly lower than the consensus expectation of analysts of 5.98 billion US dollars. In the fourth quarter, Morgan Stanley's cost control was also the best among the five major banks.

However, it must be admitted that the salary ratio of global investment banks may rise further in 2022. This year, major American banks will increase their expenditure on salary and benefits,because inflationary pressure, epidemic risk and tight labor market force them to raise their salaries in order to recruit and retain employees. The competition for talents among investment banks will not stop, especially in the face of the competitive pressure of new financial technology companies, and the labor cost is becoming a factor that can not be ignored.

The profitability of banks ultimately depends on many forces: 1) the economic recovery. From the economic data in recent months, the economic recovery is not smooth sailing, and the economic growth forecast of the United States in 2022 has also been lowered. At least,in the first quarter of this year, there will be no obvious recovery trend. High inflation will also make the recovery process tortuous, which will directly affect credit demand and bank profitability; 2) At the beginning of the epidemic, banks made provision for doubtful debts in 2020 and 2021 in order to increase the potential bad debt level. The reduction of bad debt provision this year will also directly affect profits; 2) Repurchase and dividend distribution. In 2021, bank repurchase tends to be normalized and dividends are increased, and profit indicators such as ROE and EPS are thickened, which will amplify the leverage effect during the economic recovery period, which supports the bank's share price to a certain extent.

4. Integrated banks outperform trading banks

As mentioned above, as the US market returns to normal from overheating, the trading income has started to fall from the peak. This trend is stronger with the process of raising interest rates, and the related trading business and investment banking business of major investment banks will face greater challenges.

On the other hand, economic recovery and credit demand, the rise of long-term interest rate widens the net interest margin, thus pushing up interest income, so comprehensive banks will gradually narrow the gap with trading banks.

Once FOMC raises intetest rate, the eranings flexibility of traditional comprehensive banks (JP Morgan Chase and Bank of America) begins to appear, and will outperform peers and markets.

Comments