Previously, the Q4 delivery data of $理想汽车(LI)$ was good, but under the multiple pressures,such as lack of chips, rising raw material prices and tight supply chain, the Q4 result is still valuable.

Throughout 2021, the delivery volume of Li has increased month by month, and the revenue scale has expanded rapidly. With the advantage of cost structure, the Li has achieved a profit level superior to its peers.

At the same time, we also see that after 1-2 years of capacity climbing, sales channel expansion and consumer choice, the Li One, which was criticized at the beginning and is most likely to fall behind, is becoming the mainstream of the market.

Quarterly ASP, delivery volume rose, and revenue accelerated

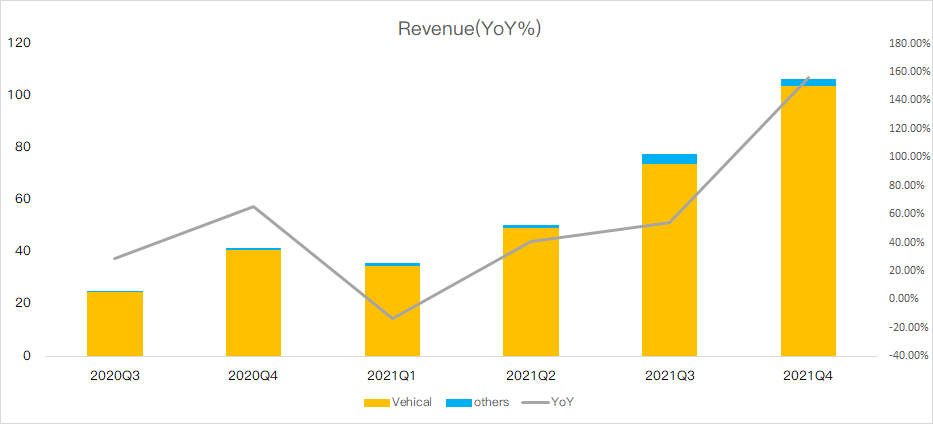

In the fourth quarter, the LI revenue was 10.62 billion yuan, a year-on-year increase of 156.1%; Among them, automobile sales revenue was 10.38 billion yuan, up 155.7% year-on-year. In 2021, the annual revenue reached 27 billion yuan, a year-on-year increase of 185.6%.

With the accelerated growth of revenue scale, the core driving force is naturally that automobile delivery has reached a new level.

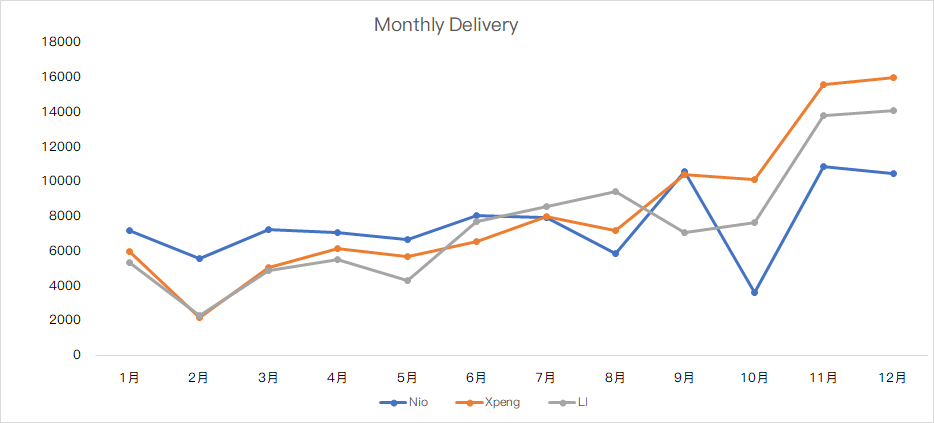

Looking back at 2021Q4, the Li delivery volume was 35,221 vehicles, up 143.5% year-on-year. The delivery volume in the first three quarters was 12,579, 17,575 and 25,116 respectively, which made a huge leap both month-on-month and year-on-year.

If compared with the three head new energy vehicle manufacturers in China, the performance of LI is better than $NIO Inc.(NIO)$and second to $XPeng Inc.(XPEV)$. If we take January into account, the LI has delivered over 10,000 yuan for three consecutive months.

In addition to the steady increase in delivery volume, the average selling price (ASP) of automobiles is also increasing. Since the release of the new LI One in the middle of last year, the average selling price in the third quarter reached 294,000 yuan, and ASP continued to maintain a high level of 294,700 yuan in the fourth quarter.

The market segment of over 300,000 medium and high-end SUVs has always been fiercely competitive. LI has to face the competition from pure trams such as Model Y and NIO Es6, as well as fuel vehicles such as Highlander and Touang. After nearly two years of competition, Ideal One has obviously established a leading position in this market segment.

In addition to the recognition of products by the market, another major driving factor for the rapid growth of revenue is the expansion of sales channels and sinking into the market.

In the second half of 2021, the expansion of offline stores and experience stores accelerated obviously. As of January 31, 2022, the LI had 220 retail stores, and achieved the goal of 200 offline stores in the whole year in the fourth quarter, sinking from first-and second-tier cities to third-and fourth-tier cities.

R&D and sales expenses are restrained, and profitability is better than peers

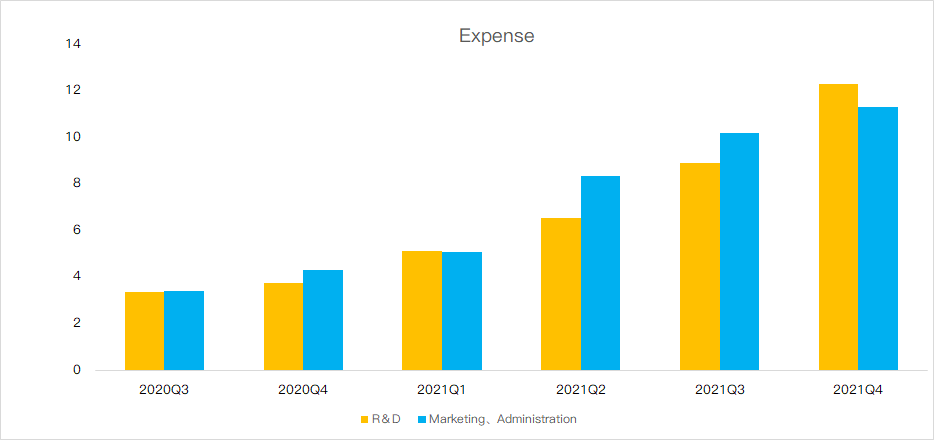

Since last year, under the high inflation environment, the automobile industry has generally faced the pressure of cost surge. Typically, the price of upstream raw materials, especially lithium, has risen several times, which has greatly raised the battery cost. Because batteries account for 30-40% of the vehicle cost, the increase in battery cost has put pressure on gross profit margin.

Q4, gross profit margin of LI is 22.4%, which decreased by one percentage point month-on-month, but increased by five percentage points year-on-year, and remained stable at about 21% throughout the year, much higher than that of XPeng and Nio.

Moreover, because LI takes a unique extended-range route, its own vehicle manufacturing cost is lower than that of pure electricity, and we observe that Ideal's investment in R&D and marketing is not so radical compared with NIO and Xpeng (R&D expenditure surged year-on-year in this quarter, but R&D expenditure/income remained stable). Therefore, the high gross profit margin and cost control once again made LI profitable in the quarter, with an operating profit of 415 million yuan and a net profit of 686.4 million yuan under Non-GAAP, up nearly five times year-on-year.

It is true that the trouble of tight supply chain may not be solved in the short term, but the ideal control of financial structure is more conducive to its survival in the bad secondary capital market.

favored by large institution

With the clarification of regulatory policies and the return of valuation to a reasonable range, the adjustment of China Stocks is gradually coming to an end, and the new energy industry has once again become the target of large investment banks and hedge funds to increase their positions. Among the three new forces of building cars, LI is obviously the most favored by institutions.

According to the latest disclosure of the fourth quarter position report (13F), it is LI to obtain positions or increase holdings from many well-known institutions. Among them, UBS Global Asset Management (America) added 7.59 million shares, and Tiger Global increased its holdings by 7 million shares, the number of shares increased by 20 times from the previous month; Morgan Stanley and Goldman Sachs bought 2.5 million shares and 6.7 million shares respectively.

In addition, HHLR Advisors, an overseas investment institution, also increased its holdings of LI and Xpeng in the fourth quarter.At the same time, LI was increased by Jinglin Assets, and its shareholding increased from 284,000 shares to 985,000 shares.

In contrast, HHLR sold nearly 60% of Wei Lai's positions in the fourth quarter.

Capital prefers certainty and profitability. After climbing the production capacity and re-selecting the market in the past two years, LI model has been proved to be feasible, and the sales growth rate, stability and profitability even rank among the forefront of new energy vehicle enterprises, which is also the main reason why the ideal has been favored by institutions.

The guidelines for the first quarter are in line with expectations, and new models can be expected

For the delivery situation in the first quarter of next year, which investors pay more attention to, the guidance given by the management is also in line with expectations.

Q1 is usually the off-season of automobile sales. The management expects the delivery volume of Q1 to be between 30,000 and 32,000 vehicles, an increase of 138.5% to 154.4% compared with the first quarter of 2021, and the performance is still strong; Total revenue ranged from 8.84 billion yuan to 9.43 billion yuan, an increase of 147.2% to 163.7% compared with the first quarter of 2021.

In addition, new model X01 is expected to be released in the second quarter and delivered in the third quarter. X01 equipped with lidar will support high-level automatic driving assistance system, and X01 with more intelligence and higher price is expected to boost total sales and revenue.

Comments