Summary

- Expansion in emerging markets and iPhone upgrades by current customers should drive continued growth for Apple.

- Microsoft has a long, robust growth runway in Azure, and its investments in gaming will likely bear fruit.

- While Microsoft is leading in the metaverse, there is talk that Apple is developing competing products.

- Looking for a helping hand in the market? Members of High Dividend Opportunities get exclusive ideas and guidance to navigate any climate.

Now consider this: Apple's P/E multiple reached the mid-30s last year, and Microsoft's P/E was in the mid-50s in 2017. This stands as a rebuttal to those who claim there is never a bad time to invest in the best companies.

Investors must determine whether one or both of these firms have the growth potential to warrant current valuations.

Apple has an ecosystem that creates a virtuous circle, while MSFT can count on the cloud for a growth runway that stretches for the foreseeable future. Additional developments could also bolster growth for both companies.

Comparing Quarterly Results

It is hard to find fault in the latest quarterly results for Apple. When perusing the earnings call transcript, one finds the term "all-time record" mentioned 31 times.

Apple set records for revenue ($123.9 billion, up 11%), operating cash flow ($47 billion) net income ($34.6 billion), and EPS ($2.10) in Q1 2022. The last two metrics were both up year-over-year by more than 20%.

Other records set last quarter:

iPhone revenue of $71.6 billion increased 9% year-over-year. Not only was revenue at an all-time high, but the active installed base of iPhone users set a new record.

Mac revenue of $10.9 billion. The 25% revenue growth rate for Mac was spurred by the redesigned MacBook Pro.

Wearables, Home and Accessories up 13% year-over-year to $14.7 billion.

The current installed base of active devices recorded a new all-time record of 1.8 billion devices.

Services revenue of $19.5 billion increased 24% from a year ago. That division set records for cloud services, for music, video, advertising and payment services, as well as a December quarter record for the App Store.

Records were also set in the Americas, Europe, Greater China and the rest of Asia Pacific.

Furthermore, as of the end of 2021, Apple counted over 785 million paid subscriptions across the company's platforms, an increase of 165 million over 2020.

The lone outlier was the iPad. iPad generated $7.2 billion in revenue, down 14% year-over-year due to supply constraints. Even so, new customers pushed the installed base of iPads to a new all-time high during the quarter. Management estimates that roughly half of the customers purchasing an iPad during the quarter were new to the product.

This robust growth occurred despite supplychainissues that likely cost the company over $6 billion in revenue.

I should add that Apple's gross margin of 43.8% nearly surpassed the highest gross margin the company has reported in a decade: back in 2012, that metric hit 43.9%.

Microsoft provided quarterly results a day before Apple. While the company did not break as many records, it still has some bragging rights.

MSFT set a record for revenue generated by Microsoft Cloud in the quarter, at over $22.1 billion, revenue was up 32% year-over-year,. With close to $51.7 billion in total revenue, an increase of 20% year-over-year, the company notched EPS of $2.48.

Azure revenue surged 46%, and revenue from Intelligent Cloud was up 26% year-over-year. Productivity and Business Processes increased 19% year-over-year, while More Personal Computing, which includes Windows, rose 15% in the same time period.

Management guides for a revenue range of $48.5 billion to $49.3 billion, along with a modest increase in operating margins in Q3.

Where We Might Find Future Growth

Apple announced it will hold a "Peek Performance" event on March 8th. There isspeculationthe company will unveil a new low-cost iPhone with 5G support and a fingerprint reader,as well asan updated version of the iPad Air and perhaps a new Mac.

There is also talk that iOS 15.4, the latest version of iPhone software, will debut.

Aside from those seeking to upgrade to the latest device, if a lower-priced entry-level iPhone becomes reality, that could act to spur significant growth.

J.P. MorgananalystSamik Chatterjee opines that a lower-priced phone could prompt 300 million current iPhone users to upgrade older iPhones and sway some of the 1.4 billion Android users with low to mid-end smartphones to migrate to an iPhone.

This topic serves as a segue into Apple'sgrowthin India. In Q421, iPhone sales in India surged by 150% year-over-year, while sales of the iPad in that country increased 109%.

The company hauled in $4 billion in revenue from India last fiscal year and captured 44% of the market for smartphones selling for over $400.

With only 17% of smartphones being 5G, there is potential for robust sales from those seeking upgrades. Of course, India is also an enormous market.

A growing installed base of iPhones also brings more customers into Apple's ecosystem, and in turn that drives revenue for the services business.

In FY21, services generated over $68 billion, or roughly 19% of the company's total revenue. Furthermore, last quarter services tallied $19.5 billion in revenue, a 24% increase year-over-year. Services also delivered a gross margin of 72.4% last quarter, versus an overall gross margin of 43.8%.

There is another trend that could provide an avenue of growth for Apple. There is a growing movement to allow employees to choose the computer and/or the mobile device they use at work. A recentstudyreports roughly half of all businesses now embrace that work model. This is driven by a belief that providing a choice results in greater employee retention and productivity.

When provided an option, 72% of employees chose a Mac over other PCs. This dovetails with afindingthat 70% of college students prefer to work on Mac devices.

Microsoft has a differing path to growth.

One very strong positive for Microsoft is the company's position as a cloud service provider. Azure's market share hasincreasedby roughly 50% since FY17, and ResearchAndMarketsforecaststhe global cloud market will increase at a CAGR of over 19% thrrough 2028.

Gartnerprojectsthe cloud market will grow 21.7% in 2022.

Microsoft's acquisition ofNuanceshould also serve to strengthen the company's cloud offerings.

I find few areas in which robust, long-term growth is as assured as Microsoft's position in the cloud. Microsoft's cloud computing revenue was up 28% in the final six months of 2021 to $35.3 billion.

Furthermore, Microsoft's Intelligent Cloud EBIT margin is 36% compared to 25% for the personal computing segment, including devices and gaming. Consequently, cloud growth is providing a high margin revenue source that offsets the low margin but near bulletproof sales generated by the company's Office products.

Another area that could generate outsized growth is Microsoft's push into gaming. I'll make a relatively short shrift of this topic, as I covered the Activision Blizzard (ATVI) acquisition in arecent article. I also provided insights into the company's push into gaming in my Octoberpiececomparing Microsoft to Amazon (AMZN).

Assuming the acquisition of ATVI is approved, that would mean Microsoft will control 14% of the gaming industry.

Although Microsoft is growing at a rapid pace, the share of revenue derived from gaming is increasing. Just over two years ago, gaming was growing at a low double-digit pace and provided 9% of the company's revenue. The last three months of 2019, gaming brought in around $3.3 billion in revenue. In the three months that ended in December of 2021, gaming revenue had increased to $5.4 billion.

Furthermore, the acquisition of Activision should increase gaming revenues by around 60%. However, I would argue that Microsoft's shift to the cloud with its xCloud gaming subscription service provides the company with an enormous advantage over rivals.

Through the cloud, we're extending the Xbox ecosystem and community to millions of new people, including in global markets where traditional PC and console gaming has long been a challenge. And when we look ahead and consider new possibilities, like offering Overwatch or Diablo, via streaming to anyone with a phone as part of Game Pass, you start to understand how exciting this acquisition will be.

Satya Nadella,CEO

Mordor Intelligenceprojectsa CAGR of 9.4% from 2022 through 2027 for the gaming market.

Gaming should also serve to buttress Microsoft's AR/VR offerings.

I would like to provide an addendum of sorts.

Since 2016, Apple's stock buyback program resulted in the company retiring nearly a quarter of the shares. In contrast, MSFT bought back roughly 5% of its stock in the same time frame.

While I understand the criticism regarding buying stock when it is selling for a relatively high P/E, I must state that Apple's progress in this respect is a strong incentive for investing in the company.

Is Apple Or Microsoft Better Positioned For The Metaverse?

Since Mark Zuckerberg changed the name of Facebook to Meta Platforms (FB), there has been a great deal of talk in the investment community regarding the metaverse.

Azure, Microsoft's gaming infrastructure, Microsoft Mesh, HoloLens, and mixed reality devices, provide a nearly comprehensive ecosystem for the development and monetization of the metaverse.

Areportby Grayscale Investments claims video gaming in the metaverse will provide $400 billion in revenue by 2025.

On the other hand, Apple has a much smaller footprint in the metaverse.

According toAppleInsider, Apple will debut augmented reality hardware in mid-2022. Here is an excerpt from the AppleInsider article discussing Apple's efforts in AR/VR:

Apple is thought to deploy products in AR and MR in three phases, with the first being a "helmet type" in 2022. It will be followed by a "glasses type" product in 2025, then contact lens-based hardware between 2030 and 2040.

When questioned by ananalystregarding Apple's metaverse initiatives during the latest earnings call, Tim Cook provided the following response:

…we're a company in the business of innovation. So we're always exploring new and emerging technologies. And I -- you've spoken at length about how this area is very interesting to us. Right now, we have over 14,000 AR kit apps in the App Store, which provide incredible AR experiences for millions of people today. And so we see a lot of potential in this space and are investing accordingly.

My takeaway is that the response was rather tepid. While I am not dismissing the potential for Apple's prospective products, after all, the company has an extensive ecosystem that elicits a strong degree of loyalty, I will note that it is a latecomer to the metaverse.

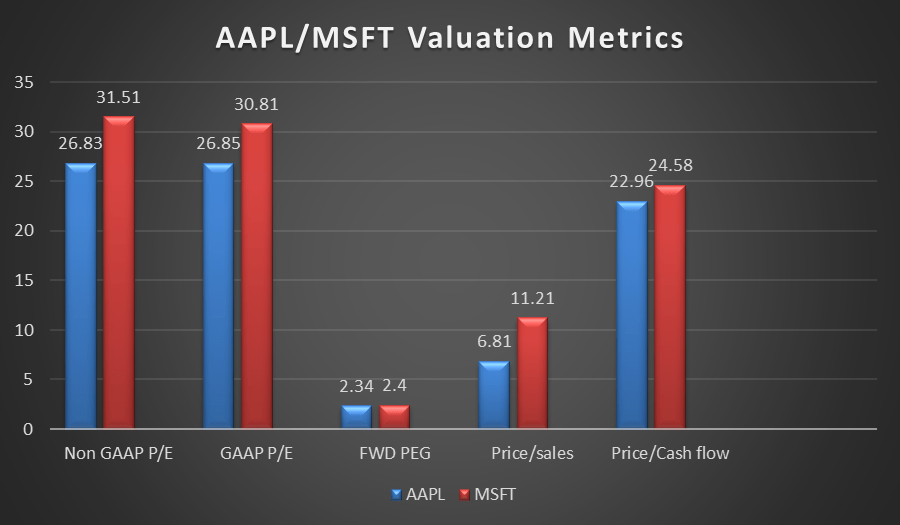

Head To Head Comparisons

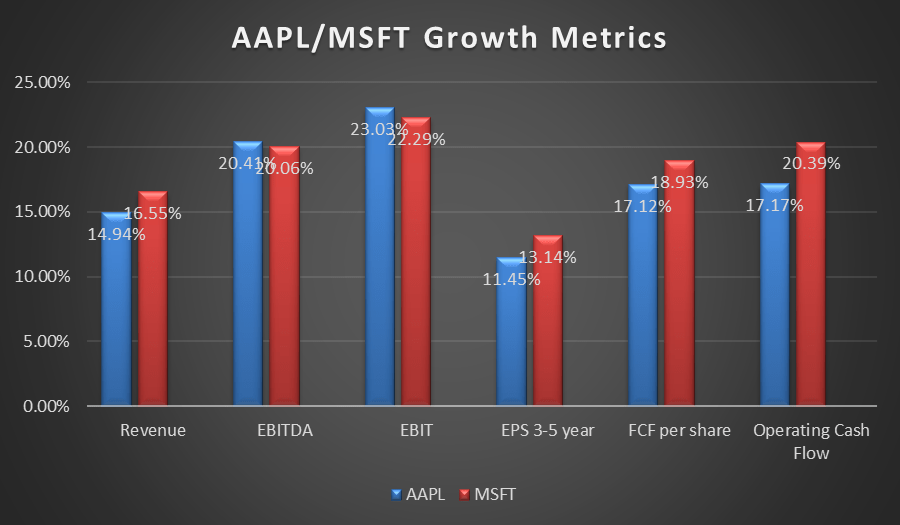

The following chart provides an array of growth metrics for the two companies. Note that with the exception of EPS, the figures represent analysts' consensus revenue estimates for two fiscal years forward.

Apple currently trades for $163.17 per share. The average 12-month price target of the 31 analysts that rate the stock is $190.24. The price target of the 17 analysts that rated the stock following the most recent quarterly report is $189.49, a 16% upside.

Microsoft currently trades for $289.86 per share. The average 12-month price target of the 33 analysts that rate the stock is $358.52. The price target of the 11 analysts that rated the stock following the most recent quarterly report is $363.03, a 25% upside.

Is AAPL Or MSFT Stock A Better Buy?

To describe Apple and Microsoft as dynamic companies is almost an understatement. Both firms have been at the cutting edge of technology, and each company has shown an enviable ability to adapt to the modern marketplace.

Arecentsurvey by 451 Research of U.S. consumers indicates an iPhone customer satisfaction rate of 98%. My review of Apple's most recent results indicates the company is setting new all-time records across nearly every product category. I also detailed how the overwhelming majority of those in the younger generation prefer Apple devices.

In contrast, Microsoft has as wide a moat as one can imagine in its Office products. However, that segment provides low margins and cannot be counted on to support a P/E that hovers around 30x. High growth is required to keep Microsoft's valuation at that level.

This is where Azure fits in. There are few areas that offer the near-guaranteed growth provided by the cloud, and MSFT appears destined to add to its market share going forward.

Additionally, I contend that the company's gaming business will likely provide a lengthy growth runway, and the metaverse as a whole could also bolster revenues.

I hold but one concern. The strengths of both companies are well known to the investing community, and one can argue that the positives surrounding the stocks are baked into the current share prices.

Apple's 5 year PEG ratio of 2.29x is well above the firm's average PEG over the last five years of 1.90x.

Microsoft's 5 year PEG of 2.34x is a bit above its average 5-year PEG of 2.23x.

I'll add that I seldom invest in companies with PEGs below 2x.

Consequently, I rate both AAPL and MSFT as HOLDS.

I'll add, however, that Apple presents a more favorable current valuation, as recorded in the chart above.$Microsoft(MSFT)$

source:seekingalpha

Comments