Wall Street concluded on the minutes that there is a lack of Hawkish hawkish surprises and little new information that the market does not know.

-We were cheated by the Federal Reserve again. When we issued a hawkish statement in January, it seemed that we knew everything and everything was certain. Now I find out that they don't know anything.

At 3:00 a.m. Beijing time, the minutes of the Fed meeting were released. This 20-page minute is a transcript of the meeting on January 27th. That is, at this meeting, the Fed completely changed into a super hawk image-announcing that QE will end in early March and raise interest rates "soon and appropriately" (the currency carnival era is over, and the Fed is starting the most historic tightening cycle).

The Fed usually releases minutes three weeks after the meeting, and a statement immediately after the meeting ends, which will be very concise (with or without raising interest rates, what is the rate increase?) . For example, the full statement of the meeting in January was less than 700 words, and these officials actually met for two days. Therefore, this detailed meeting minutes is very important for studying Fed policy (there will be some details). What many officials say, what a few officials say, and the minutes of the meeting almost express the anonymous views of all people. After they finish talking about several issues, they will talk about the results of their votes.

Given the length, just focus (all eyes will be on any sign of a 50 basis point rate hike, the timing of the balance sheet downsizing, and comments on when the rate hike cycle will end).

1. Policies

(Most officials) tend to continue to reduce QE according to the timetable announced in December and end it in early March (QE ends in early March, which means there will be no interest rate increase before March).

(Most officials) believe that if inflation does not go down as expected, it would be appropriate to cancel the easing policy faster than expected.

(Most officials) believe that the rate hike will be faster than the rate hike cycle in 2015.

The meeting discussed the timing and pace of lifting easing policy and its impact on economic prospects (when it will trigger economic recession and when to cut interest rates).

The policy path will depend on the economic development prospects, and the assessment of the policy stance will be updated at each meeting (indicating that the Fed does not know what to do next, and studies it step by step).

In the current highly uncertain environment, maintain policy flexibility to implement appropriate policy adjustments according to risk management (strengthening the Fed's data dependence model, especially around inflation. Anything is possible, and the ultimate interpretation power belongs to the Fed).

Here are the controversial parts:

(A few officials) believe that QE should be ended as soon as possible to send a stronger signal that the Fed is committed to reducing inflation (a few officials support raising interest rates before March).

(A small number of officials) worry about the risk that financial conditions could be overly tightened by the swift lifting of policy easing (a small number of officials do not support too fast interest rate hikes).

2. Inflation

Participants pointed out that inflation continues to be well above 2%, and the inflation outlook faces upward risks (it is a consensus within the Fed that inflation has not yet peaked).

If inflation does not fall as expected, easing will be lifted more quickly than currently expected.

3. Employment

(Most officials) commented that labor market conditions are very close to full employment (the job market has met the conditions for raising interest rates).

(A few officials) commented that in their view, the maximum employment has not yet been reached (the job market has not yet reached the adjustment of raising interest rates).

4. Balance sheet

(Most officials) commented that at some point in the future, it may be appropriate to sell part of the principal of the securities held and reinvest them in government bonds (unlike the way of reducing the balance sheet in 2017, when a certain number of securities were allowed to mature and the returned funds were not used to buy securities instead). And reduce the Fed's securities holdings over time in a predictable way.

[A few officials] commented that the situation may support the start of balance sheet reduction later this year (possibly around December).

Participants agreed that details of the timing and pace of the balance sheet reduction would be worked out at the forthcoming meeting (details of the reduction will be revealed at the March meeting).

5. US stock market

Asset valuation pressure is still great, especially the forward P/E ratio of the S&P 500 index is in its historyThe highest level in history (when the Fed governs, it still worries about the overvaluation of the stock market)

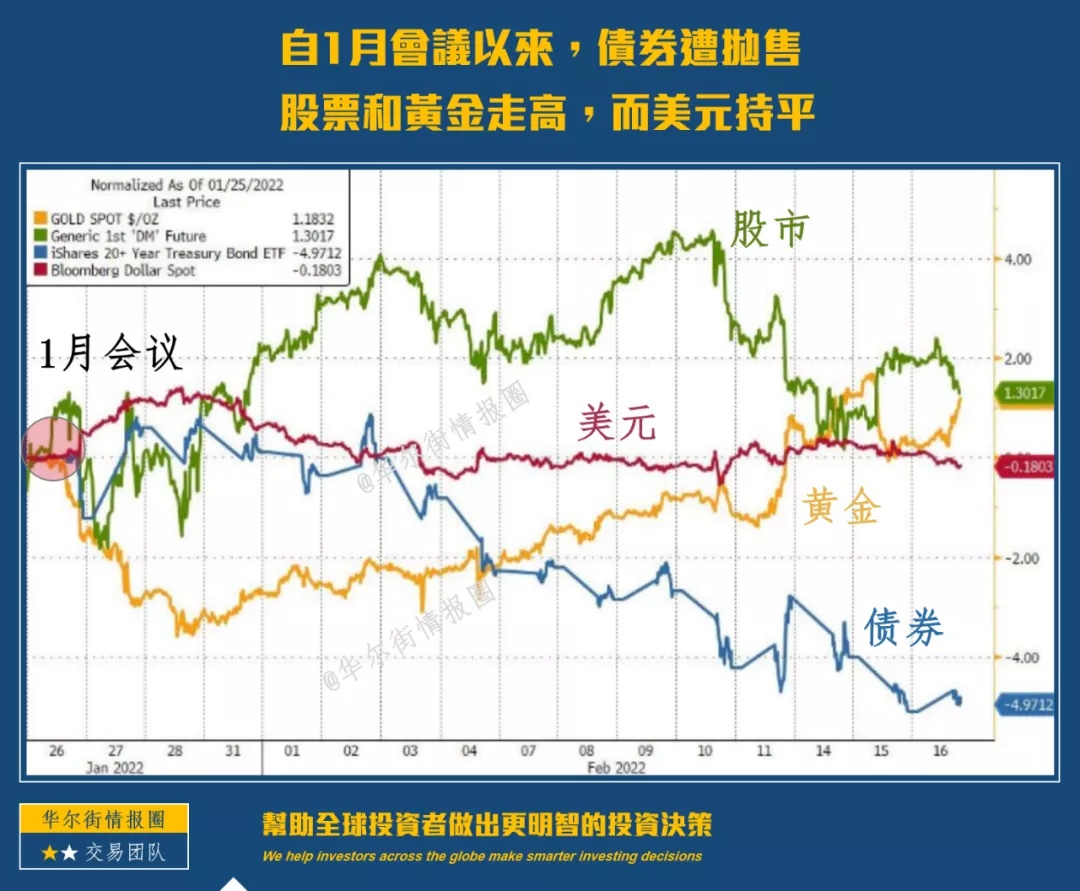

Wall Street concluded on the minutes that there was a lack of Hawkish hawkish surprises and little new information that markets did not know. Therefore, at the moment when the minutes of the meeting were released, the US stock market rose, gold rose, the US dollar fell, and the US bond yield retreated its increase.

However, I think this summary provides us with a lot of things worth studying.

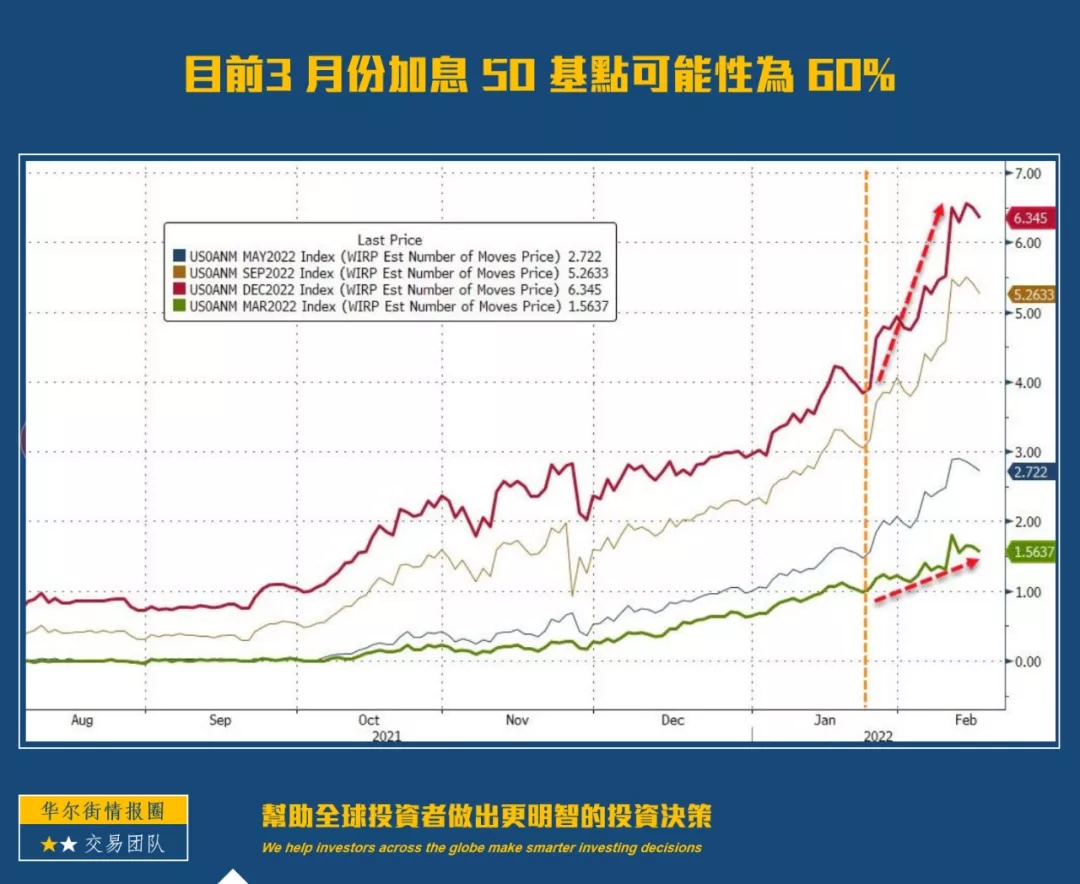

First, from the content point of view, there is almost no definite conclusion, which shows the Fed's high degree of self-distrust. With such lack of confidence, do you think it is possible for the Federal Reserve to raise interest rates by 50 basis points in March?

The minutes of the Fed meeting reduce the probability of raising interest rates

Second, "finalize the details of the time and speed of balance sheet reduction at the upcoming meeting." This is very useful information. I also judged that the Fed would not mention the details of balance sheet reduction in the first half of the year. The more the Fed talks, the more chaotic the market may be. It seems that a turmoil on March 17th is inevitable.

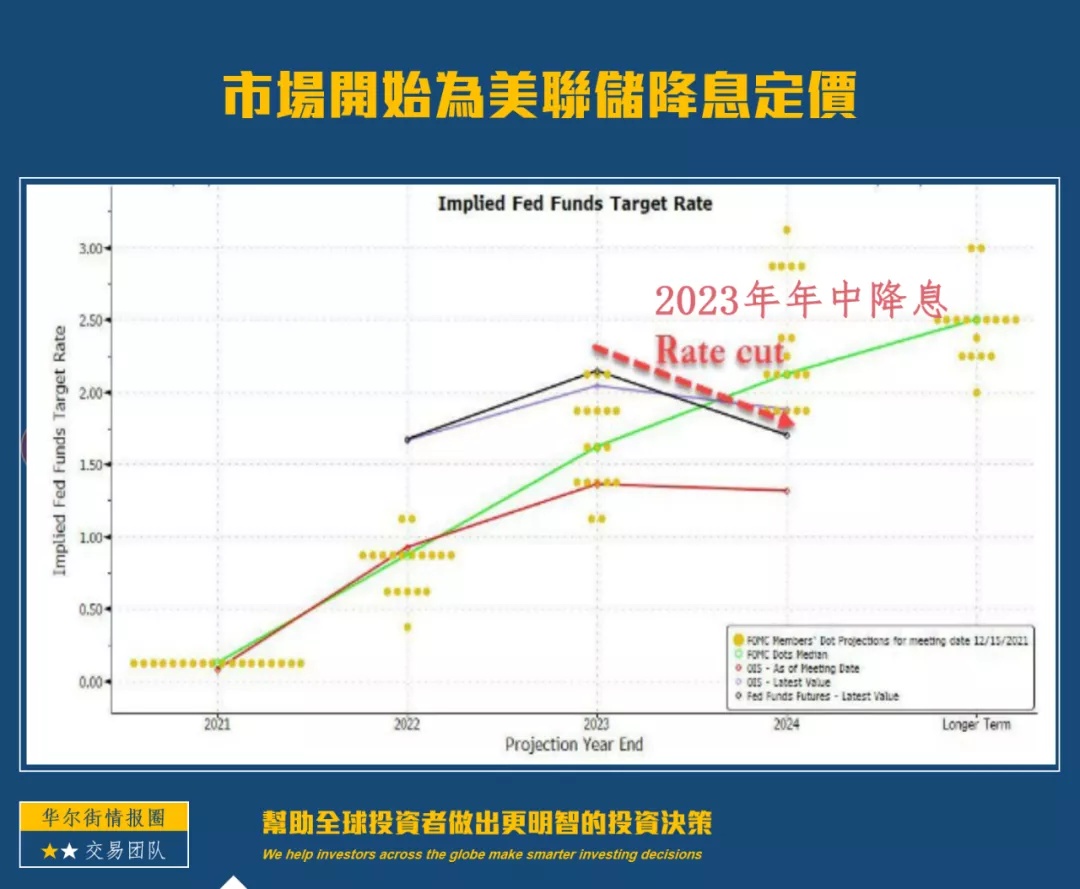

Third, it is now clear that the Fed will become more hawkish in the short term (most support faster rate hikes) and then a dovish shift (for fear of recession). In other words, interest rate hikes will be very frequent at first, but then they will end quickly. This is a sprint, not a long run.

Fourth, before the Fed raises or cuts interest rates, it will assume a complete path: when to raise interest rates-when to end interest rates-when to cut interest rates. It is thought out at the beginning, and this time they cannot provide the same predictability. This may be a bumpy time for the market. The Fed's strategy is to look at the economic data first, then take it step by step, and it is expected that it will not be understood until the second half of the year.

Fifth, the minutes are not as hawkish as expected (as reflected by the dollar sell-off), and the Fed cannot be so aggressive. I have long said that from the Fed's point of view, they should act responsibly when communicating with politicians and the public, so they will look like hawks. But you know, they can't do that. In the end, the Fed may give politicians different answers than it gives traders. Don't be too innocent.

In general, we were fooled by the Federal Reserve again. When we issued the hawkish statement in January, it seemed that we knew everything and everything was certain. Now I find out that they don't know anything.

$E-mini Nasdaq 100 - main 2203(NQmain)$ $YMmain(YMmain)$ $Gold - main 2204(GCmain)$ $Light Crude Oil - main 2203(CLmain)$

Comments

(Most officials) commented that at some point in the future, it may be appropriate to sell part of the principal of the securities held and reinvest them in government bonds