$Pinterest, Inc.(PINS)$ released Q2 financial report after close of August 1. Although double miss, it did not plunge as last week's Facebook$Meta Platforms, Inc.(META)$And$Snap Inc(SNAP)$, An important reason is the support of Elliott, a new major shareholder.

For Q2 performance

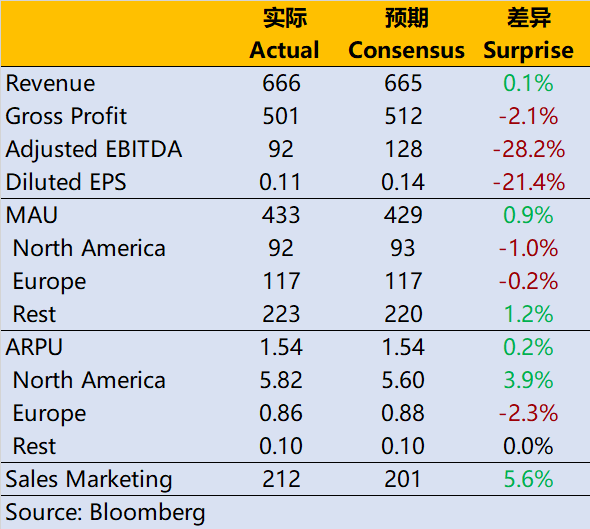

- Revenue was US $666 million, up 8.6% year-on-year, almost the same as expected;

- The adjusted EBITDA was US $92 million, down 48% year-on-year, which was worse than the expected US $128 million;

- The diluted EPS was US $0.11, which was worse than the expected US $0.14.

- MAU 433 million, down 4.6% year-on-year, but better than the expected 429 million;

With the lessons by Facebook and Snapchat last week, market has priced- in, so PINS's price is not sensitive to the poor performance.

Some believe the decline of MAU is slightly better than expected, regarded as "good news". However, the monthly active users of PINS in North America have not caught up with the daily active users of SNAP, and ARPU is only 74% of SNAP, so it is not particularly good news.

On the other hand, because of the intervention of activist investor Elliott Management and the belief in the long-term value of Pinterest, it boosted investor confidence and rose 21% in after-hours.

Let's compare the performance of SNAP and PINS

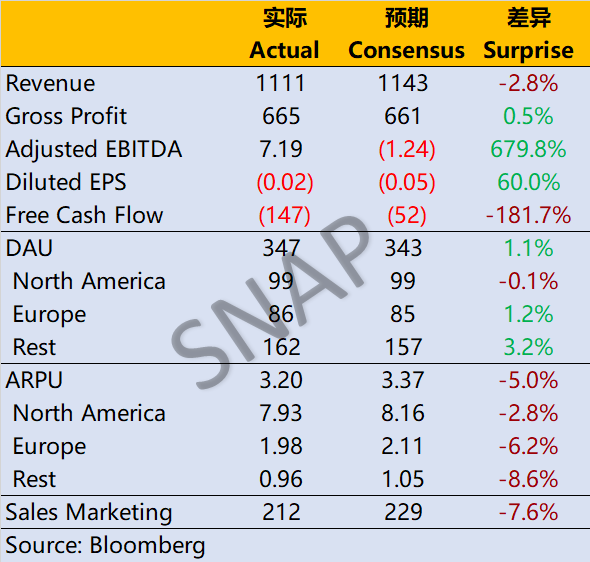

- PINS has meeet the estimate of revenue, while SNAP's revenue is a miss.

- SNAP is still losing money, but it has made a breakthrough in reducing losses this quarter, and the marketing expenses are similar to PINS; And PINS still continues to maintain profitability;

- SNAP's free cash flow Q2 continued to flow out 150 million, while PINS's free cash flow has been positive after 21 years, with a single quarter of 200 million US dollars.

- It is also interesting that,The Q3 revenue growth of both companies is expected to fall into the "middle single digit"Is much lower than predicted by previous analyst models.

Facebook, on the other hand, hit the ceiling, and revenue declined. Although it did not give guidance, the market expected Q3 revenue to decline in the middle single digits. In comparison, Facebook's social App matrix is more powerful, justThe whole advertising industry is facing strong macro headwind and competition from video industry.

From the valuation point of view, the income multiples of PINS, SNAP and META for 12 consecutive months are 5.18, 4.61 and 3.44 respectively. In terms of profit multiples, the EV/EBITDA of PINS in the past 12 months is 34 times, while META is 8.3 times. PINS has a relatively higher valuation because it is also smaller in size.

But in the final analysis, the favor of investors is the most important. PINS is obviously more stable than the other two.

How important a major shareholders could be? $TENCENT(00700)$'s shareholders could tell...

Comments