After the market on March 28, yoga sportswear brands$lululemon athletica (LULU) $The Q4 performance of fiscal year 22 ended January 29, 2023 was announced. Because Q3 Financial Reporting Company actively lowered Q4 performance, the stock price in the secondary market dropped by more than 12%. However, Q4 performance once again exceeded market expectations, which also showed that the company's previous lowering expectations were somewhat conservative. Therefore, the company also took the initiative to raise the guidelines for the next quarter, which also made the market re-enhance its performance expectations, and the stock price returned to the Q3 decline.

Overview

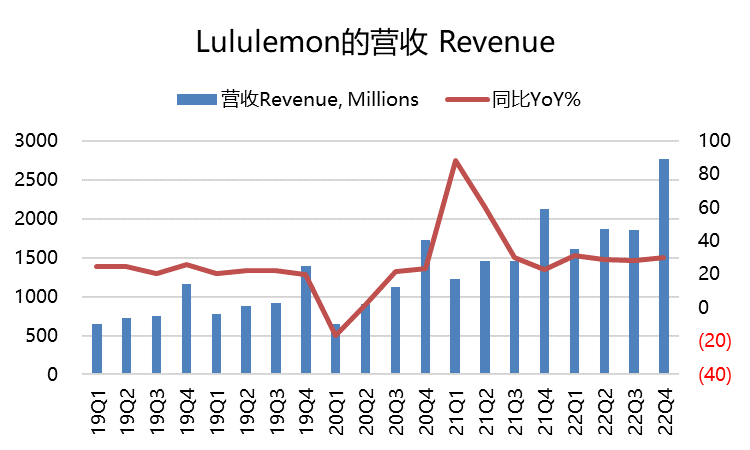

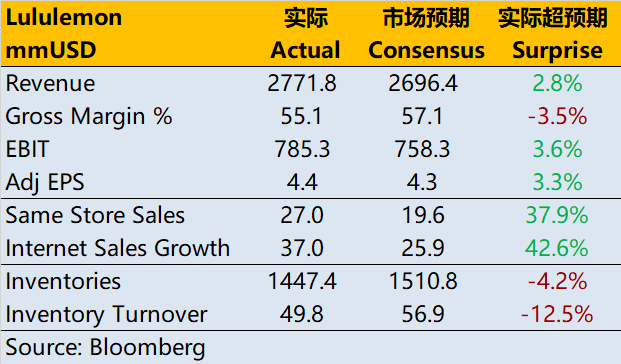

Overall revenue was US $2.77 billion, up 30% year-on-year, exceeding the consensus of US $2.70 billion expected by the market. At a fixed exchange rate, it increased by 33% year-on-year.

Comparable sales in the same store increased by 27% year-on-year and 30% at a fixed exchange rate, which was higher than the 22.7% generally expected by the market. Among them, the same-store sales of stores increased by 15% year-on-year, and the net income of DTC business increased by 37%.

Gross profit margin decreased by 300 basis points to 55.1%, which was worse than the expected 57.1%. After adjustment, gross profit margin decreased by 70 basis points year-on-year to 57.4%.

In terms of profit, earnings before interest and tax was US $785 million, up year-on-year, higher than the market expectation of US $758 million.

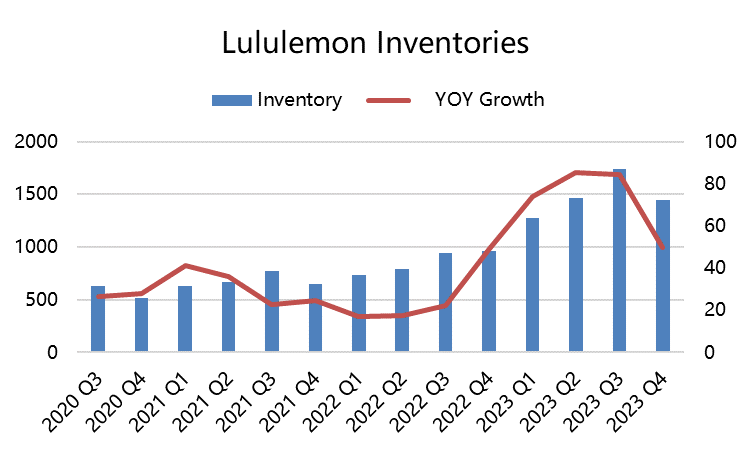

At the same time, inventories reached US $967 million, a surge of 50% year-on-year, but less than the market expectation of US $1.51 billion.

Investment Highlights

In the dynamic operating environment of 2022 (most), lululemon, as a middle and high-end sportswear brand, can still exceed the annual revenue target, which also proves the lasting influence of lululemon brand.

The overall same-store sales growth is higher than the market expectation, but it is more from the online (DTC) business, which has increased by 30% year-on-year (fixed exchange rate), and the proportion of DTC has reached 52%, more than half.

On the one hand, it shows that consumers' recognition and loyalty to brands have increased; On the other hand, it also shows that users' consumption habits may change permanently since the pandemic.

It must be mentioned that the business in China increased by 30% this quarter, which is lower than the CAGR of 50% in the past three years, but it is indeed higher than expected to achieve such results under the influence of COVID-19 in November-December. After all, Nike, which previously announced its financial report, saw its sales in Greater China decline again as of February 28th.

This quarter's inventory growth reached nearly 50% year-on-year, reaching 967 million yuan, which also increased slightly compared with the previous quarter, but the growth rate also declined year-on-year. Although Europe and America suffer from inflation, the inflation level of clothing is low. Due to the decline of residents' savings, purchasing power may not be as strong as before. However, China has experienced the end of the epidemic and the Spring Festival holiday, and its sales recovery is still in progress, but the recovery prospects are good.

If inventory continues to rise, it seems possible to see this "never discount" company discount.

Estimate and Valuation

The company's revenue for Q1 in fiscal year 2023 will be between 1.89 billion and 1.93 billion US dollars, which is higher than the current market consensus of 1.85 billion US dollars. Diluted earnings per share are expected to be between $1.93 and $2.00, which is also much higher than the consensus of $1.64.

For the whole fiscal year 2023, the company expects revenue to be between 9.3 billion and 9.41 billion US dollars, which is higher than the consensus of 9.41 billion US dollars. At the same time, the diluted earnings per share guidance is between $11.50 and $11.72, which is higher than the consensus of $11.30.

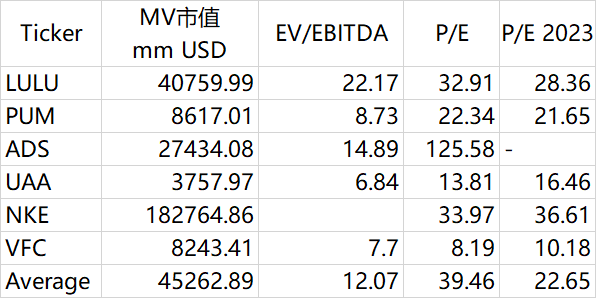

At present, the company's P/E level is medium and high in the industry, but it is higher than the head of the industry$Nike (NKE) $It's also much lower.

In terms of growth, Lululemon is still higher than these traditional sportswear brands, and it is expected to perform better in the recovery of Greater China this year. At the same time, Lululemon is increasingly showing its advantages in the recognition of users' brands.

Comments

👍🏻👍🏻