Last week's macroeconomic events were intensive and significant.

March 7th, Federal Reserve Chairman Jerome Powell expressed a hawkish speech during his congressional testimony, stating that "future rate hikes may exceed previous expectations and may last longer." It immediately caused the market's expectations for the March interest rate hike to move from 25 basis points to 50 basis points (with a probability of nearly 70%).

However, the liquidity crisis at Silicon Valley Bank on Friday quickly dispelled these expectations. Currently, the Fed's policy observation tool shows that the probability of a 50 basis point rate hike in March is 0, the probability of a 25 basis point rate hike is 96%, and the probability of no rate hike is 4%.

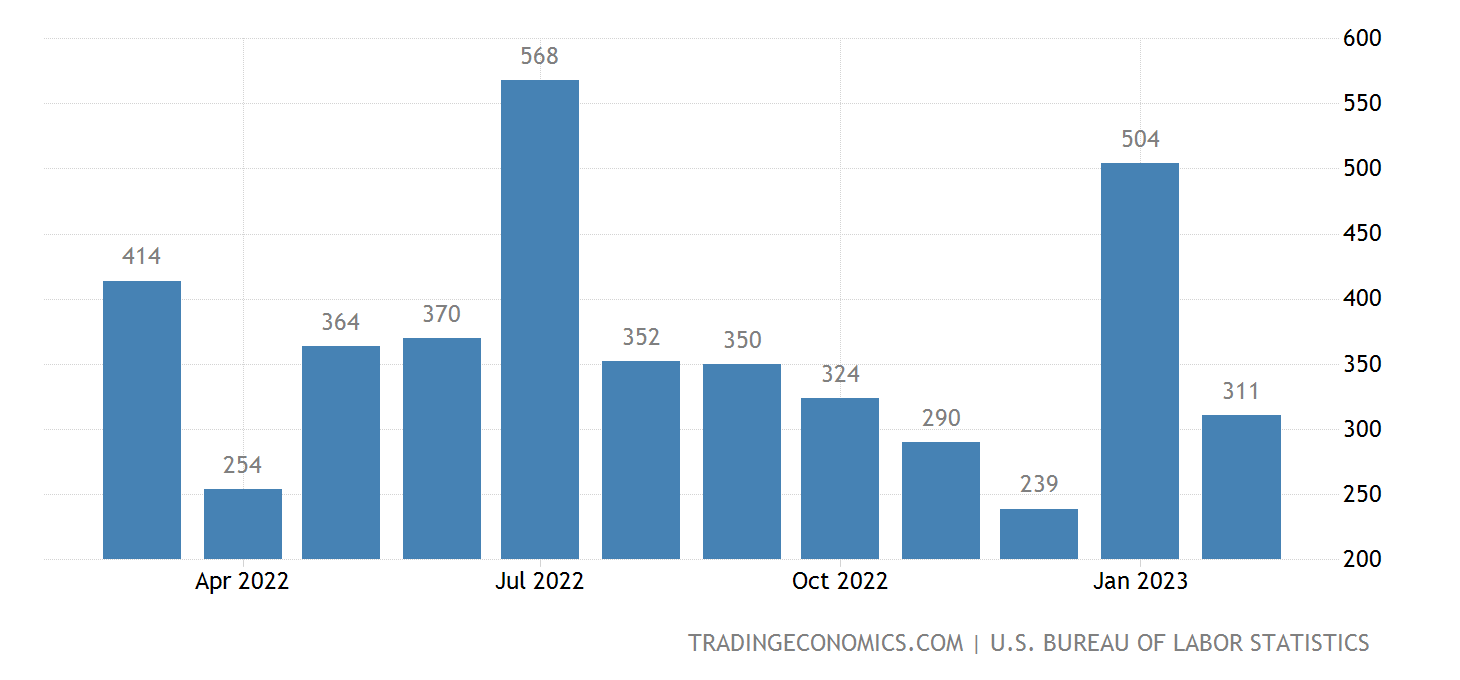

Meanwhile, the nonfarm payroll report released by the United States on March 10th also indicated some macro market sentiment. The number of nonfarm payroll jobs exceeded market expectations, reaching 311,000, with leisure and hospitality, retail, government, and healthcare leading job growth.

This was also to some extent a misaligned recovery (with warm weather in February, leisure and hospitality employment increased by over 100,000), but the labor market remains robust, with hiring demand continuing to exceed available workers.

Interestingly, the unemployment rate also rose from 3.4% to 3.6%, higher than expected (not on the same scale as the nonfarm payroll), and the month-over-month wage growth slowed down, with average hourly earnings increasing by 4.6% year-on-year, lower than the expected 4.8%. This also eased the market's concerns about escalating interest rate hikes and lowered the basis for sustained high inflation.

Average Hourly Earnings% MoM

Employment data are lagging indicators, providing a basis for the Fed's next monetary policy meeting while also constantly confirming the market's previous expectation of "slowing inflation." As we have entered the "quiet period" before the Fed's March FOMC meeting, there will be no statements from Fed officials this week. However, Tuesday's February CPI data will be a very critical piece of data.

The biggest focus this week is still on the liquidity risk issues of Silicon Valley Bank. Essentially, this is a bank liquidity crisis caused by the Fed's tightening policies (raising rates and reducing balance sheets).

Silicon Valley Bank (SIVB) is facing a liquidity crisis triggered by the aggressive tightening of major central banks worldwide, represented by the Federal Reserve. As financing costs continue to rise, "cheap money" is disappearing, and market interest rates are expected to remain high for longer. To counter this, SIVB has resorted to shortening the duration of its assets to increase short-term net interest income. However, this move has created a liquidity gap, which has raised doubts about the bank's solvency in the market.

SIVB's decision to sell assets at a discount, almost all AFS assets, has further exacerbated the run, triggering market volatility. The good news is that it is only a liquidity problem at present, and there is no debt leverage, thanks to stricter supervision after the subprime mortgage crisis. The liquidity problem can be handled by the central bank as the lender of last resort, but debt leverage requires large-scale debt restructuring.

U.S. Treasury Secretary Yellen has stated that the SIVB crisis is not a technical problem of enterprises but is caused by raising interest rates. However, the government will not implement a rescue. To provide some relief, the Federal Reserve has announced the $25 billion Bank Term Financing Program (BTFP) on March 12, providing loans for up to one year to all U.S. federally insured depository institutions. The program allows banks to mortgage U.S. Treasury bonds and mortgage-backed bonds and other debt, borrowing at one-year overnight index swap rate plus 10 basis points to meet client withdrawal requests without having to sell the bonds at a loss. The Treasury will allocate $25 billion from the Exchange Stabilization Fund as a backstop for BTFP, but the Fed does not expect to need to use these support funds.

Financial risks are highly homogeneous and contagious, so panic has quickly spread to other similar small and medium-sized banks. However, big banks (too-big-to-fail) are not seeing similar characteristics at the moment because they are well capitalized. Liquidity problems have always come on suddenly and don't last long. In recent years, with the tightening of central banks in various countries, similar events have emerged one after another, such as the British pension crisis, the FTX bankruptcy crisis, the BlackRock Nordic REITs redemption crisis, and the Credit Suisse liquidity crisis.

The current inflation is the biggest constraint on the global economy. Central banks worldwide are actively or passively following interest rate hikes to curb inflation, even if the domestic economy has not fully recovered from the epidemic. In 2022, the proportion of central banks that have entered the cycle of interest rate hikes in the world has reached the highest level since the 1980s' highest level ever (~80%). According to Bloomberg, in the next 6 months, two-thirds of central banks worldwide are still in the process of raising interest rates.

The Fed may also re-examine its monetary policy path as a result. Goldman Sachs has changed its view, believing that the Fed is unlikely to raise interest rates at the March interest rate meeting. The bankruptcy of SIVB has hit the sentiment of the technology industry and related investors, triggering investors to think about the overall systemic risk, and could potentially lead to further adjustments in US stocks.

Comments

買爆空投手不抖