Microsoft issued a disappointing revenue forecast for the current quarter in its earnings call on Tuesday, causing a reverse in the stock price after the shares initially rallied on better-than-expected earnings for the December quarter.

What are your thoughts on this earnings report? Would it be worthwhile to invest in Microsoft?

How is Microsoft's financial report?

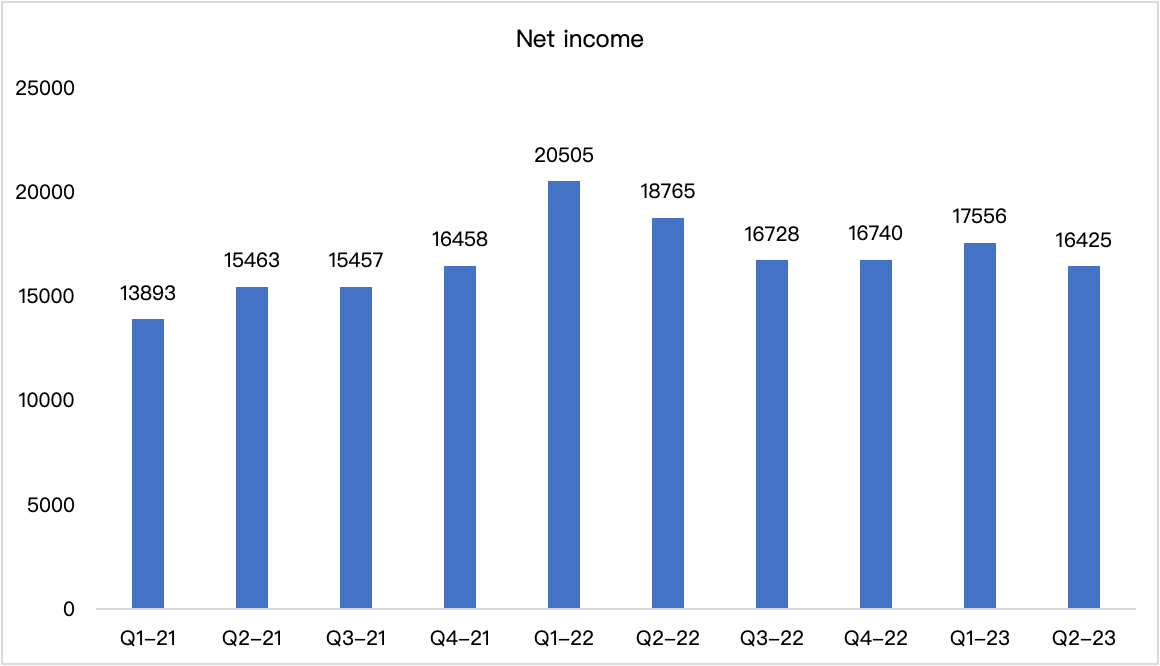

According to key data, Microsoft's revenue in the second quarter of fiscal year 2023 was US $52.75 billion, slightly lower than the market expectation of 52.94 billion,Year-on-year increase of 2% .It is the lowest level since 2016.Operating income was $20.4 billion GAAP and $21.6 billion non-GAAP, and decreased 8% and 3%, respectively. Net income was $16.4 billion GAAP and $17.4 billion non-GAAP, and decreased 12% and 7%, respectively. Diluted earnings per share was $2.20 GAAP and $2.32 non-GAAP, and decreased 11% and 6%, respectively.

Net income was $16.4 billion GAAP and $17.4 billion non-GAAP, and decreased 12% and 7%, respectively.

- ·Office Commercial products and cloud services revenue increased 7% (up 14%in constant currency) driven by Office 365 Commercial revenue growth of 11% (up 18% in constant currency)

- ·Office Consumer products and cloud services revenue decreased 2% (up 3% in constant currency) and Microsoft 365 Consumer subscribers grew to 63.2 million

- ·LinkedIn revenue increased 10% (up 14% in constant currency)

- ·Dynamics products and cloud services revenue increased 13% (up 20% in constant currency) driven by Dynamics 365 revenue growth of 21% (up 29% in constant currency)

Revenue in Intelligent Cloud was $21.5 billion and increased 18% (up 24% in constant currency), with the following business highlights:

- ·Server products and cloud services revenue increased 20% (up 26% in constant currency) driven by Azure and other cloud services revenue growth of 31% (up 38% in constant currency)

Revenue in More Personal Computing was $14.2 billion and decreased 19% (down 16% in constant currency), with the following business highlights:

- ·Windows OEM revenue decreased 39%

- ·Windows Commercial products and cloud services revenue decreased 3% (up 3% in constant currency)

- ·Xbox content and services revenue decreased 12% (down 8% in constant currency)

- ·Search and news advertising revenue excluding traffic acquisition costs increased 10% (up 15% in constant currency)

- ·Devices revenue decreased 39% (down 34% in constant currency)

Microsoft's Earnings Confirm Fears of Economic Slowing

Market participants celebrated Microsoft's (MSFT) headline numbers on Tuesday night which showed a slight earnings beat but comments by management about the challenges that lie ahead trapped the early buyers. Microsoft was up as much as 5% last night but is now indicated to be 1.5% lower early on Wednesday morning. There is at least one downgrade so far this morning by BMO Capital to "underweight".

The primary thesis of market bears has been that the market has yet to discount slowing economic growth. The thinking is that forward earnings estimates are still too high, and valuations will come down as multiples erode.

In addition to lowering expectations, Microsoft also announced last week that it would lay off 10,000 jobs in the third quarter of fiscal year 2023.

The technology industry has always been seen as one of the"carriages"that drives the U.S. economy, and the emergence of a "wave of layoffs" has raised public concern regarding the macroeconomic crisis. Technology companies may find that they are unable to grow as fast or spend as freely as they did in the past few years, as a result of the new economic environment.

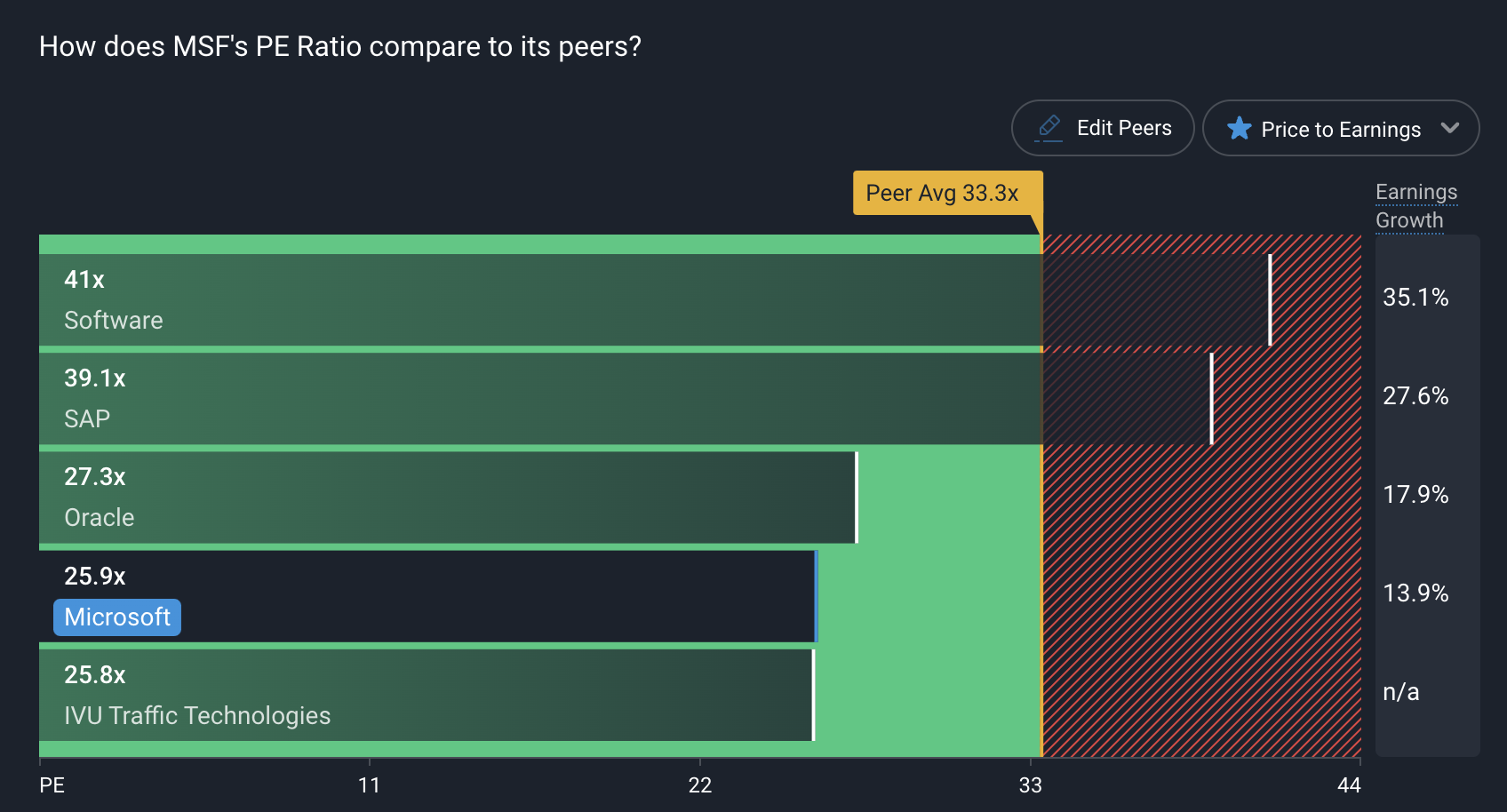

Is Microsoft expensive?

Is Microsoft expensive or not? Microsoft's current valuation is 23-25 times earnings, which is below the 10-year average. The forward P/E ratio in 2023 is 24.5 times, which means that the profit forecast in 2032 has not changed much.

In the long run, there is nothing wrong with Microsoft's fundamentals. If we consider the empowerment in AI field, Microsoft is still worth looking forward to. But now this market is not easy to say, after all, the impact of economic recession enterprises can not be estimated, want to invest in Microsoft friends suggest to wait, such as the economic situation is clearer, perhaps a better investment opportunity.$Microsoft(MSFT)$

Comments