Market has been testing recently, whether a recession is coming?

Last week, Jan US CPI and PPI both exceeded eastimates, which also made the US treasury and Dollar Index significantly higher. We had discussed last week, What A Boost in January CPI Could Mean To Market?

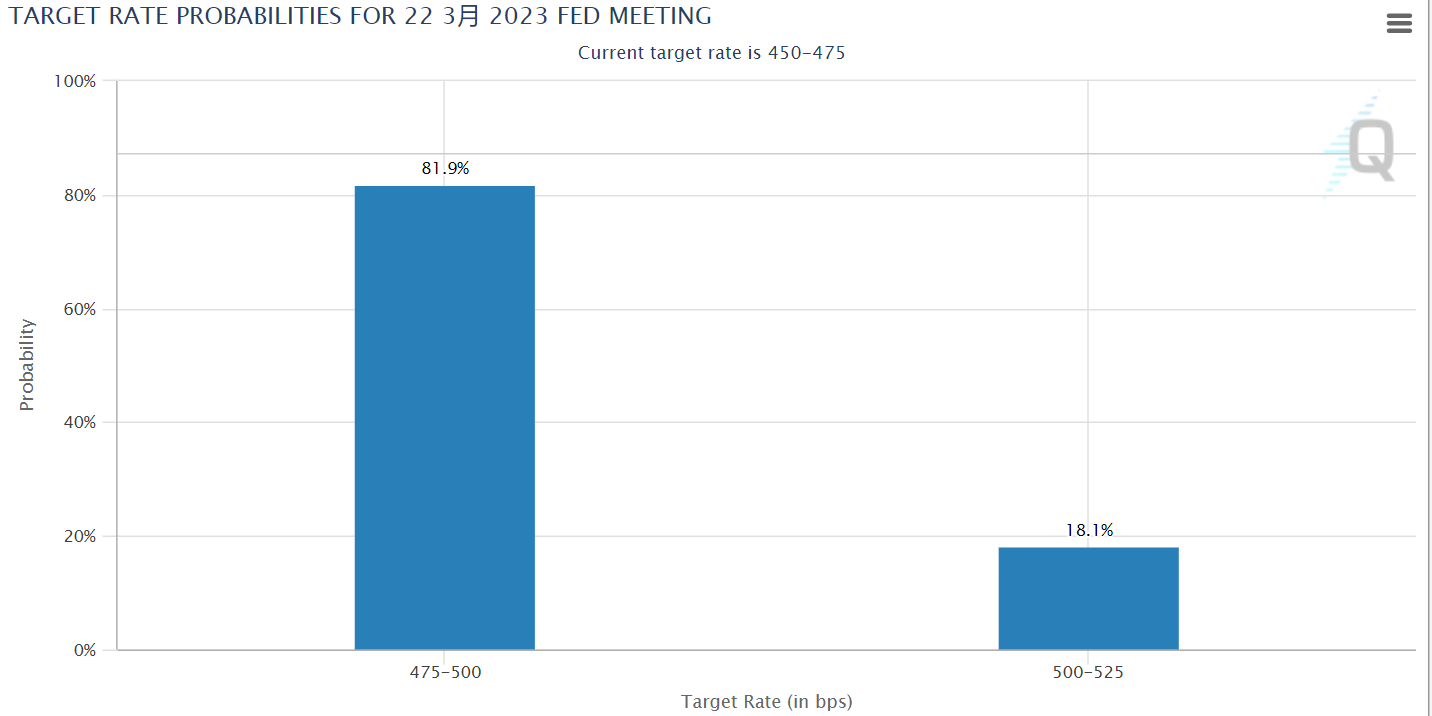

At the same time, other economic data (such as non-agricultural) continued to remain strong, and the market's expectation of the Fed's pivot began to reverse. At present, market has been implying that Fed will raise interest rates by 75 basis points more in the next few months, and the possibility of 50 bps interest rate hike in March FOMC meeting is reaching 81.9%.

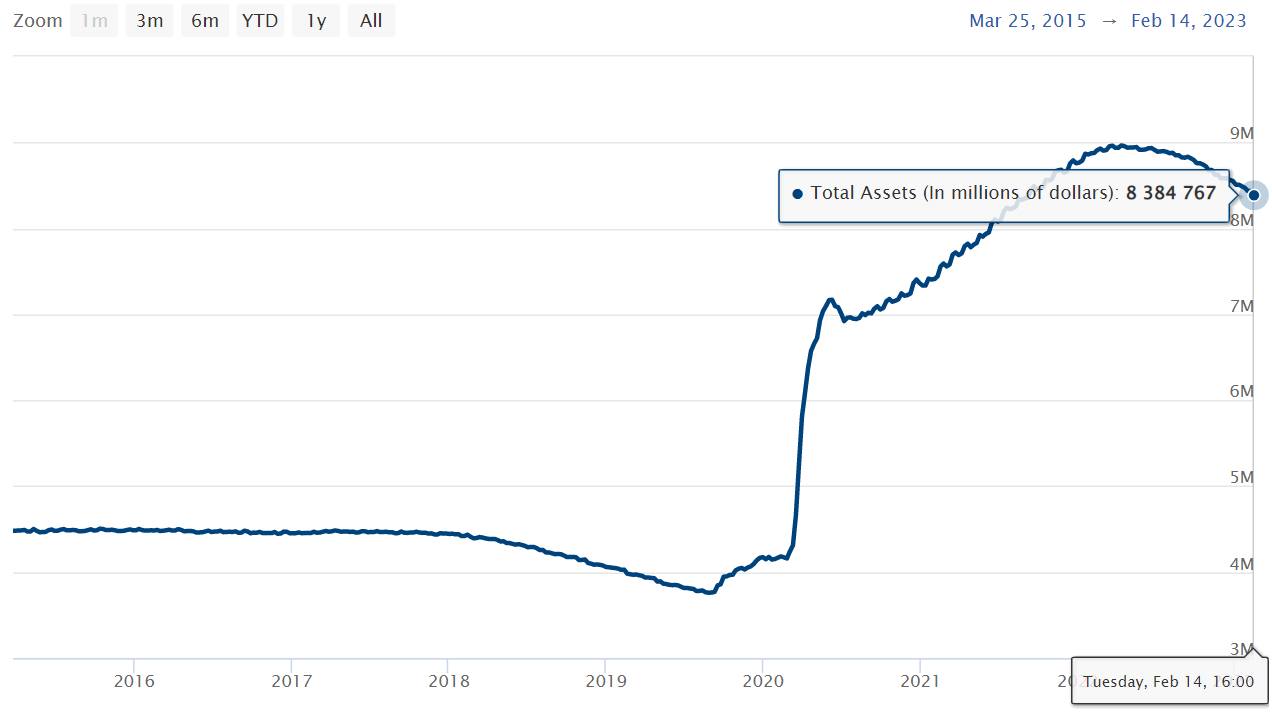

The current tightening of monetary policy by the Federal Reserve relies more on raising interest rates, and the speed of scale reduction is slower than that when QE was started before, resulting in insufficient liquidity tightening. However, the fiscal expenditure has not decreased much.

Although the liquidity in the United States has been tightened, it is still looser than before the epidemic. Although this does make the policy tightening restrain the economy mildly, which is in line with the Fed's expectation of suppressing inflation and enabling the economy to make a soft landing, it in turn slows down the rate of inflation decline.

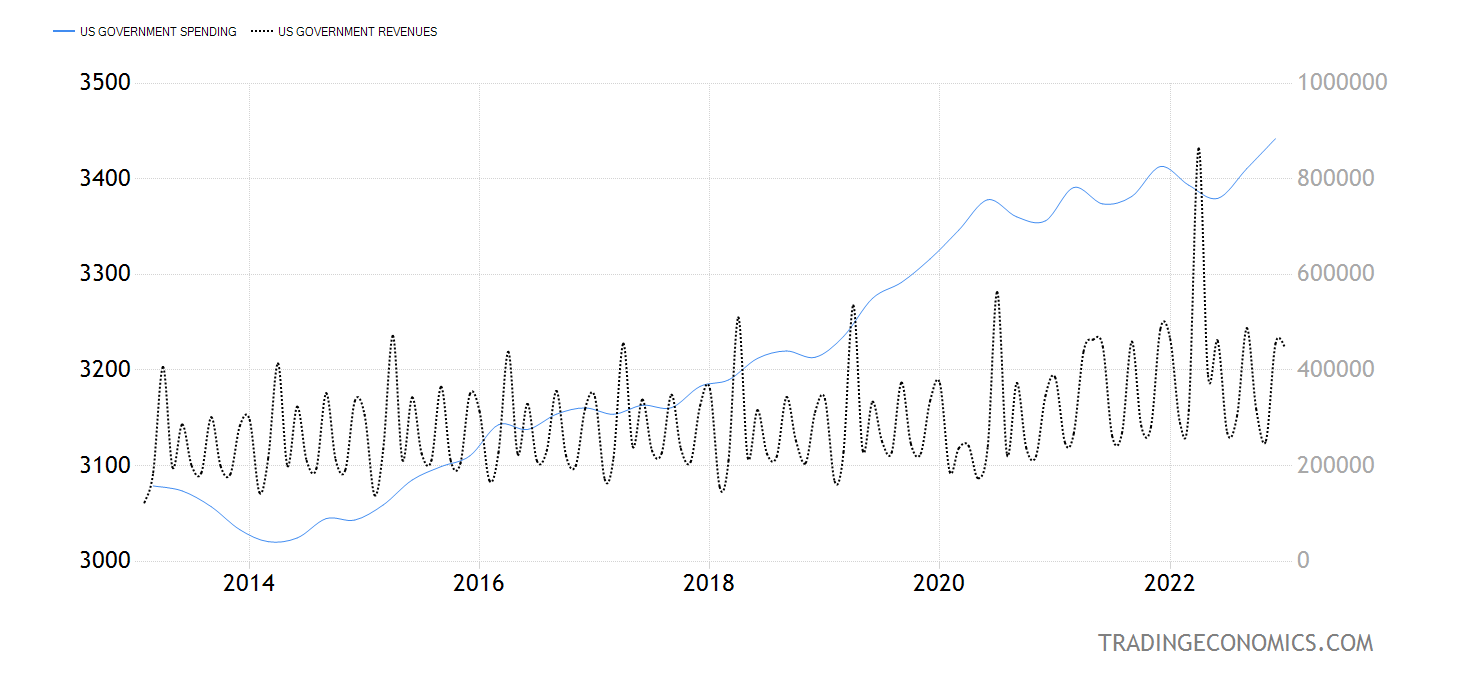

In the first four months of fiscal year 2023, the US fiscal expenditure was 1.93 trillion US dollars (a record high). If the average annual growth rate of each month from January 2020 is calculated based on the same period in 2019, we can see that the current fiscal expenditure growth rate has dropped from the previous high point, but it is still higher than the average level before the epidemic.

- In January, ISM service PMI rose above threshold (55.2 vs. December 49.2), and new orders and business activities were obviously repaired.

- In February, Michigan's consumer confidence index rose higher than expected to 66.4 (vs. 64.9 in January), and consumer confidence of all income groups has improved since November.

- Fannie Mae's homebuyer confidence index has rebounded sharply from its low since November last year, and the survey data of builders has shown signs of recovery since December.

- In January, 517,000 new non-agricultural jobs far exceeded expectations, the largest increase since July 2022. Low-end service industries such as leisure hotels, commercial services and retail rebounded significantly

- In January, the unemployment rate fell to 3.4%, the lowest since 1969;

- In January, the CPI fell less than expected, with an overall year-on-year rate of 6.4% and a quarter-on-quarter rate of 0.5%;

- Retail consumption in January exceeded expectations by 3% (vs.0.1% in December)

- Although the industrial output was flat in January, the manufacturing industry increased by 1% month-on-month, the largest increase in the past year.

- NAR (National Association of Realtors) consumers' affordability to buy houses rebounded from the low point since November last year, which contributed to the increase of new home sales for three consecutive months.

In the short term, the market's expectation of policy tightening may be difficult to weaken for the time being.

Before there are more signs that inflation will fall rapidly or the economy weakens, or the geopolitical uncertainty heats up, the yield of US and US bonds may remain fluctuating in high range.

Comments