If $TENCENT(00700)$'s retracement was impacted by major shareholder selling, liquidity problems in Hong Kong market, then US social stocks $Meta Platforms, Inc.(META)$,$Snap Inc(SNAP)$$Pinterest, Inc.(PINS)$ should prove the extermination of the value.

Different with Tencent's monetization, META and SNAP's revenue are almost only advertising, so under the background of recession, they are much easier to fall into Davis double kill of both stock price and performance.

In this way, SNAP's third-quarter financial report miss the consensus and plunged sharply again, is not an accident. SNAP has already lowered its Q3 guidance before.

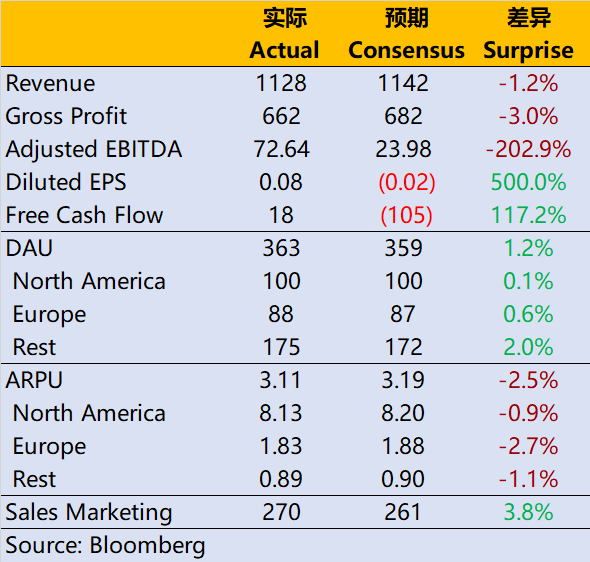

- Q3 revenue was 1.13 billion US dollars, a year-on-year increase of 6%, which was the lowest since listing and fell to single digits for the first time, and it was less than the market expectation of 1.14 billion US dollars;

- The adjusted earnings per share was 0.08 US dollars, which was better than the market expected loss per share of 0.02 US dollars. The net loss increased by 400% year-on-year, and the loss per share was 0.22 US dollars. In the same period last year, it was a loss of 0.05 US dollars, of which 155 million US dollars were restructuring expenses;

- DAU, a daily active user, increased by 19% year-on-year to 363 million, and the market expected consensus was 358.2 million;

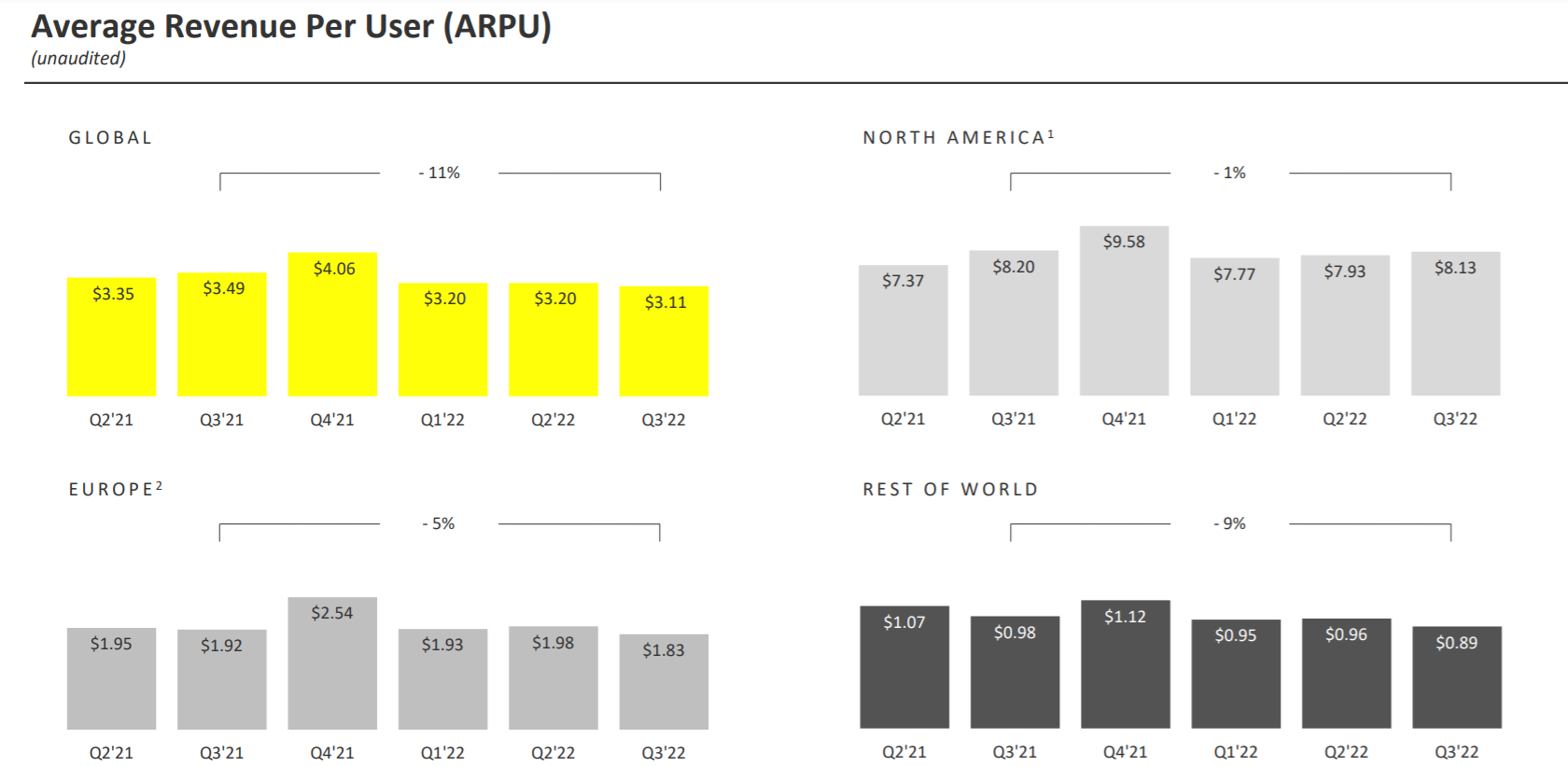

- As a result, the revenue ARPU generated by individual users dropped to 3.11 US dollars, and the market expected to be 3.19 US dollars; Among them, ARPU in Europe was US $1.83, down 5% year-on-year, while that in other regions outside North America decreased by 9%. As you can imagine, the influence of exchange rate is also very important.

At the same time, the company refused to give Q4 performance guidance, the market believe it "has no confidence in even the lower limit of performance", it is no wonder that it plunged 27% after hours.

Different from subscription companies, SNAP, a company that focuses on advertising revenue, cannot directly determine the quality of revenue by the number of users, and companies need to have more strategies in realizing cash. At present, the depression of the advertising industry also makes social enterprises worried but no solution. It is not the sole situation of SNAP.

The competition trend is even more fierce. In addition to the competition with its peers like META (FB, INS, Reels), TWTR and PINS, it also faces such a powerful opponent as Tik Tok, even$Amazon.com(AMZN)$,$eBay(EBAY)$,$Etsy(ETSY)$, E-commerce platforms such as this have also taken away advertisers with higher efficiency needs. There are also those who have just entered the advertising market$Netflix(NFLX)$.

The stronger the expectation of recession, the higher the requirement of advertisers for realization efficiency. And if social companies can't prove their ability to advertisers, then some dispensable advertising expenses can be lost.

Therefore, the next financial reports such as META and PINS will not be much better. META has at least more than a decade of accumulated cash to buy back and help prop up the company's share price. But without a new direction, what should investors think of social companies?

Winter has just begun, don't expect spring is near.

Comments

With slowing global economy, high inflation and rising interest rates, Snap's revenue and earnings are severely impacted as companies cut their advertising budget.

On top of that Snap also faced competition especially from Tik Tok. It is no wonder Snap's latest earnings report 3Q 2022 is dismal and its share price plunged almost 30% that day.

This negative news will certainly impact Meta Platforms and Pinterest too and their share prices have also fallen in tandem.

Thanks @MaverickTiger for your excellent analysis on Snap and the snowball effect on other social media stocks.

[真香]