Weak Advertising means nearer recession?

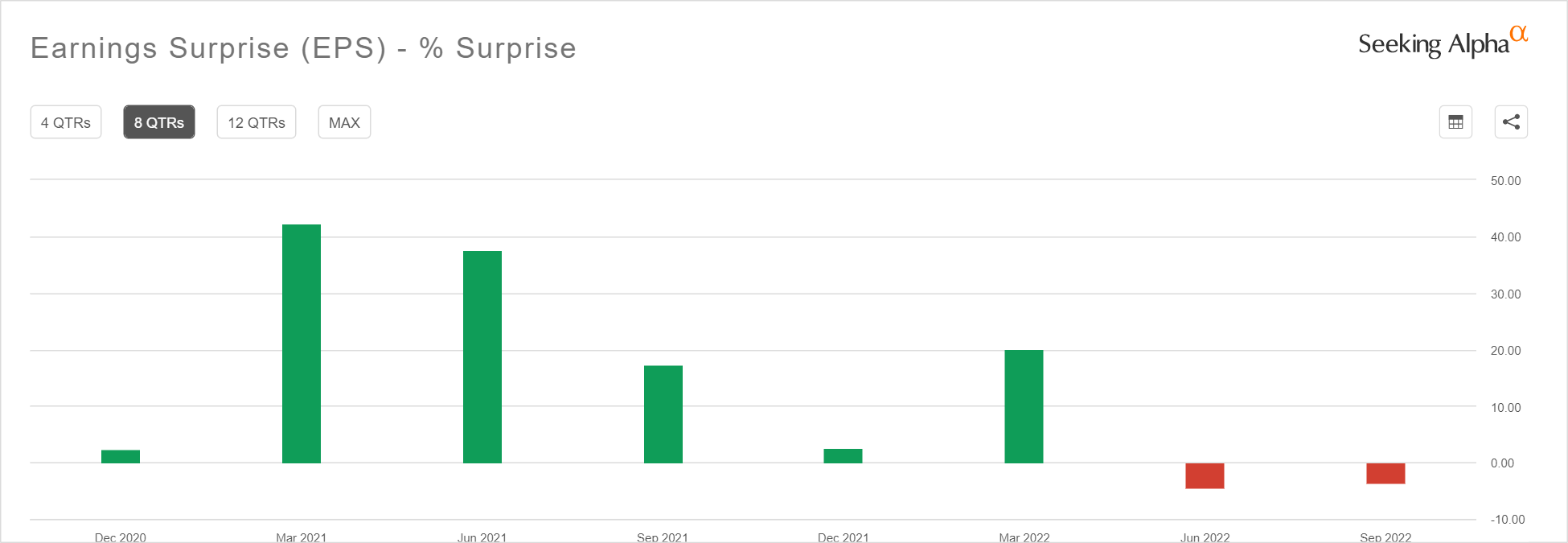

$Alphabet(GOOG)$ released Q3 earning after October 25th's trading hours, it plunged of 6.6% due to both revenue and profit miss the expectations. Last time it plunged that much occurred in 2019, but in the past two years, only one EPS fell short of expectations (last quarter).$Alphabet(GOOGL)$

How bad Google's performance could be?

Double miss is rare in Google's earnings history.

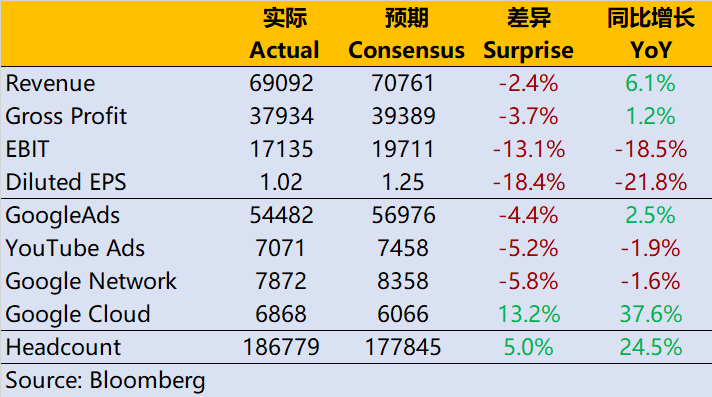

- Revenue was US $69.09 billion, up only 6.1% year-on-year, which was about 2.4% lower than the expected consensus of US $70.76 billion, and it was also the lowest growth rate in history except the epidemic-affected quarter.

- The comparable EBIT is US $17.14 billion,It is about 13% worse than the expected consensus of $19.7 billionThe profit gap is even greater.

- All the unexpected differences come from the advertising business.Actual revenue from the advertising business was $54.5 billion, which was less than the expected $57 billion, with a surprise of -$2.5 billion,

- Among them, the revenue of Google Engine was US $39.5 billion, with a year-on-year growth rate falling to 4.3%, while YouTube advertising decreased by 1.9% year-on-year to US $7.07 billion.

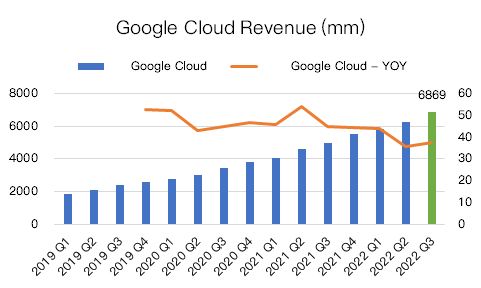

- In terms of cloud business, the overall revenue was US $6.9 billion, with a year-on-year growth rate of 38%, which was better than the expected US $6.6 billion and better than peers. But the loss before interest and tax was $700 million, which was better than expected.

- Other businesses (including hardware, games, streaming media, etc.) had revenue of $200 million and a loss before interest and tax of $1.6 billion.

Advertising business declined, while Google Cloud increased, which means profit margin lower, from 32% in the same period last year to 24.8%, even far below market consensus of 27%.

Why is the market so sensitive to Google's performance this time?

Considering that Google Q3 acquired and consolidated $Mandiant(MNDT)$, whose Q3 is expected revenue is $144 million. Which means the real surprise of Google Cloud busniss is only 3.6%.

In fact, Google Cloud's expectation is relatively high, and the market consensus is 32% year-on-year growthe, which is the only major cloud service company with an expected growth rate of over 30%.

What surprised the market was the weak of advertising business.

From last week's $Snap Inc(SNAP)$ financial report, the market also smells danger.

We noticed that the big banks frequently revised Google's performance expectations in early October.In the past three months, no big bank has raised Google's revenue forecast, and all of them have been loweredIt's over, The main reason is the advertising business.

While the market continues to reduce expectations, Google's advertising business is still less than expected, and the real number is unexpected, so the natural market will not give any good feedback.

Of course, there is also the influence of foreign exchange, but this piece is also expected by the market.The expected foreign exchange impact was $3.83 billion, while the actual impact was $3.92 billion, it's close. The impact of the exchange rate is huge, but priced-in.

What Google Q3 Earnings Tell Investors?

1. The greater the contraction of advertising, the stronger the expectation of recession.

Google executives generously acknowledged the decline in major advertising businesses, and also made it clear that YouTube included Advertisers' willingness to put in decreases. This is an industrial issue.

This quarter, the advertising business is mainly supported by travel and retail industries. But after these two quarters, are there more advertisers in the industry willing to spend?

Here's what Pichai said: Advertisers are carefully reevaluating the effectiveness of their budgets.

The implication is that the higher the requirements of advertisers for delivery conversion, the more cautious their delivery will be.

2. Online video advertising in highly competitive

YouTube's advertising business has fallen short of expectations, and there are some competitive factors. In addition to Tik Tok, the strongest competitor of short videos, there are also those who are about to enter the advertising industry$Netflix(NFLX)$.

YouTube also continued to strengthen its YouTube Short short video service in Q3, and announced that it would start sharing revenue with creators. To some extent, this will increase Google's own expenses and reduce its profit margin.

But there is no way. The competition is getting fiercer and fiercer.

3. Google also needs to reduce cost

There are many factors that affect Google's profit, such as marketing expenses, research and development expenses, broadband costs and foreign exchange headwinds. Every item is not so easy to solve. However, as the profit margin keeps falling, shareholders will put forward higher requirements for the company.

Among them, labor cost is also an important direction for Google to control next. The number of employees in this quarter increased by 12,700 compared with the previous quarter and 36,700 compared with the same period last year. The total number of employees reached 187,000. Besides 2600 from Mandiant, a newly merged company, it has a lot of hiring of its own.

The scale of hiring is certainly too much, so executives say the number of new employees in the fourth quarter will be much lower than in the third quarter. At the same time "

Plan 2023 makes important trade-offs when needed, focusing on slowing down the growth of operating expenses.

The implication is that layoffs may be made.

Advertising contraction hints the recession, Executive hints the redanduncy, where will the US economy go in 2023?

Comments

Last week was a week that Big Tech would like to forget. Google presented a dismal 3Q22 earnings report that caused its share price to plummet further.

The main culprit was decrease in advertising revenue. This is not surprising considering that Google's main source of revenue is advertising.

However the market sell offs present a exciting opportunity to buy more Google's shares. Google is still a fundamentally profitable company with lots of growth ahead.

Thanks @MaverickTiger for your excellent insights on Google's 3Q22 performance.

Really worth to spend time and read this...