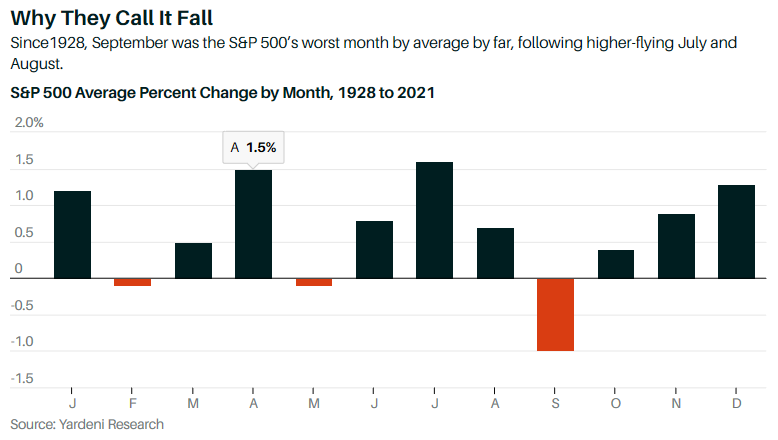

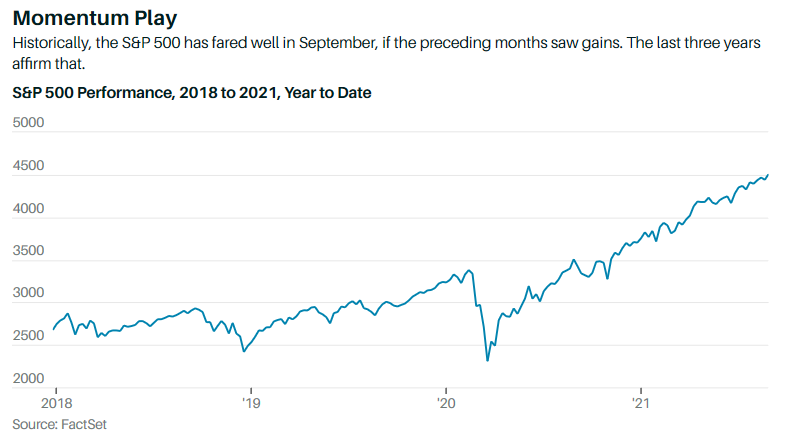

Stocks famously perform poorly in September. But that may not necessarily be the case in a year like 2021.

Since 1928, the average September return for the S&P 500 has been a 0.99% loss. That makes the month far worse than May, which ranks second in investor gloom with an average loss of 0.11%. But there’s a caveat here. History also finds that Septembers that follow strong gains earlier in the year tended to have positive returns. When the S&P 500 rose by more than 13% over the first six months, the median September gain since 1928 rang in at 1.4%, according to Fundstrat.

Over that 93-year span, the S&P fell in 54% of the Septembers. But when markets rose from January through June, 63% of the Septembers saw positive gains. Through June of this year, the S&P 500 rallied 14%.

This Week

Monday 9/6

Stock and fixed-income markets are closed in observance of Labor Day.

Tuesday 9/7

Casey’s General Stores and Coupa Software announce earnings.

Wednesday 9/8

Copart, GameStop, and Lululemon Athletica release quarterly results.

Analog Devices hosts a conference call to discuss its capital-allocation plans and update its outlook for fiscal 2021. The company recently closed its $21 billion acquisition of Maxim Integrated Products.

Global Payments, Johnson Controls International, and ResMed hold virtual investor days.

The Bureau of Labor Statistics releases the Job Openings and Labor Turnover Survey. Consensus estimate is for 10 million job openings on the last business day of July. In June, there were 10.1 million openings, the fourth consecutive monthly record.

The Federal Reserve reports consumer credit data for July. Total outstanding consumer debt increased by $37.7 billion to a record $4.32 trillion in June. For the second quarter, consumer credit rose at a seasonally adjusted annual rate of 8.8%, reflecting pent-up demand.

The Federal Reserve releases the beige book for the sixth of eight times this year. The report summarizes current economic conditions among the 12 Federal Reserve districts.

Thursday 9/9

Home Depot hosts a conference call to discuss its ESG strategy, led by Ron Jarvis, the company’s chief sustainability officer.

Moderna hosts its fifth annual R&D day to discuss vaccines in the company’s pipeline. CEO Stéphane Bancel will be among the presenters.

Danaher holds an investor and analyst meeting, hosted by its CEO Rainer Blair.

International Paper, Synchrony Financial, and Willis Towers Watson hold investor days.

The European Central Bank announces its monetary-policy decision. The ECB is expected to keep its key interest rate unchanged at minus 0.5%.

The Department of Labor reports initial jobless claims for the week ending on Sept. 4. In August, claims averaged 355,000 a week, the lowest since the pandemic’s onset. This will also be the last week that the extra $300 from federal enhanced unemployment benefits is available. They are set to expire by Sept. 6.

Friday 9/10

The BLS reportsthe producer price index for August. Economists forecast a 0.6% monthly rise along with a 0.5% increase for the core PPI, which excludes volatile food and energy prices. Both jumped 1% in July.

Kroger holds a conference calls to discuss earnings. Albemarle and Bio-Techne host their 2021 investor days.