Summary

- Shares of Palantir have dropped 30% since the start of November, despite a fundamental business that continues to thrive.

- In particular, Palantir has been successful at diversifying away from government contracts, with overall commercial revenue growth accelerating in Q3 and more than doubling in the U.S.

- Still, the government business is not slacking, with the company winning recent contracts with the Air Force, Department of Health and Human Services, and National Institutes of Health.

- Cash flow is also trending ahead of plan, driving the company to boost its full-year cash flow guidance by $100 million.

The mantra of "thinking and investing for the long term" is a well-touted investment principle, yet rarely ever put into practice. It's also a rule that is most commonly broken in the tech sector, where investors choose their stocks primarily based on momentum and rarely based on fundamentals and value.

So when the great growth correction of 2021 happened in the fourth quarter this year, while many stocks certainly deserved a small correction and a breather in valuations, many high-quality names got knocked down multiple pegs far more than their fundamentals justify. In this bucket is Palantir (PLTR), the big data analytics powerhouse which has seen a tremendous correction in its share price despite a business that has never looked healthier.

Perhaps alone among high-profile software IPOs, Palantir has had a very rocky trading journey since going public last October. Palantir took a while to get off the ground, as investors worried early on that the lack of an insider lockup period would pressure Palantir's ability to rally. The stock did end up rallying and peaked near $40 in mid-February, before proceeding to trade in a very jagged and choppy fashion throughout the rest of the year, including a ~30% decline since November alongside other tech growth stocks.

Throughout this tumultuous time period, I've happily held onto my Palantir stock, and this company is one of the rare exceptions where I'm very bullish on a stock that is technically trading at quite expensive valuation multiples (though, with the sharp correction from February peaks, Palantir isn't trading at the egregiously expensive multiples it was trading at earlier). I continue to view Palantir as a tech mega-cap in the making, one with a powerhouse software platform that is broadly applicable across industries, and across both the public and private sectors. Currently dominant primarily in the United States, Palantir also has broadly untested expansion opportunities abroad, where innovation in big data and machine learning technologies has not quite yet matured.

Stay long here, and add to your positions in Palantir at its new lower price before year-end: in my view, Palantir is well-equipped to outperform the market indices for years to come.

Recent wins showcase how prominent Palantir is

Before we get into more granular details and fundamentals, it's worthwhile to illustrate that Palantir has been busy from a go-to-market perspective. The company is always on the heels of some large, transformational deal, and the current situation is no different. In particular, the company has just recently signed a multi-year $60 million deal with the National Institutes of Health:

Figure 1. Palantir NIH win

And, building off the strength that Palantir has historically enjoyed with the U.S. armed forces, the company also signed a four-year $87 million deal with the Department of Veterans Affairs:

Figure 2. Palantir VA win

And though the large deals that Palantir showcase are typically public-sector deals, the company's commercial/enterprise sales have recently picked up steam as well, which we'll discuss in further detail in this article.

The bullish thesis for Palantir, revisited

With the recent pessimism in Palantir stock over the past two months, it can be easy for investors to forget the longer-term bullish thesis and fundamental merits that this company possesses in abundance.

Here's a refresher of all the key reasons why this company is a superstar:

- Big data is a massive discipline that can be applied in nearly limitless ways.Palantir isn't a software company that serves only one or a limited set of use cases. Data and inferences that can be made from data are prevalent in just about everything: which explains why Palantir is such a powerful tool for both public and private sector clients.

- Growth at scale.Despite being at a ~$2 billion annual revenue scale, Palantir continues to deliver 30-40% y/y revenue growth, and its long-term outlook calls for the company to be able to sustain growth rates in excess of 30% y/y through at least 2025. Few companies are able to achieve this kind of growth at scale, and it's a testament to the wide applicability of Palantir's products and the humongous clientele it has drawn (in particular, the U.S. Army).

- Stepping up go-to-market momentum.Palantir is chasing growth across a wide variety of channels. The company has stepped up its sales hiring this year, a nod at the broad market opportunity it has and the need for more territory coverage. Palantir also has deepened relationships with ISVs (integrated service vendors) that can resell Palantir's products without its involvement and offer additional coverage that Palantir's direct sales force can't handle.

- One foot in the public sector, one foot in private. Palantir made its name on being a large federal government contractor, but its products are just as compelling to an enterprise segment that is growing ever more obsessed with the value of big data. Most software companies start off as primarily dealing with enterprise buyers, and then hopefully getting FedRAMP certification to sell into public sector clients later. Palantir did the reverse: but now, its momentum with Fortune 100 companies is continuing to grow, and customer adds are continuing to trend at an impressive pace.

- Free cash flow.Though not yet profitable from a GAAP standpoint, Palantir continues to exceed internal expectations for free cash flow, which means the business is self-financing (a departure from. many other rapid-growth software companies that continue to need to raise capital to finance their losses).

Valuation isn't cheap, but more reasonable than in the past

I wouldn't go so far as to say that Palantir's recent correction has left the stock at cheap levels - but for the caliber of this company's brand, plus its consistent combination of hyper-growth at scale while building up profitability and margins, I view its current valuation as quite reasonable.

At current share prices near $18, Palantir trades at a market cap of $35.99 billion. After netting off the $2.48 billion cash pile on its books (another reason to be bullish on Palantir: it has a load of cash and is unencumbered by debt), its resulting enterprise value is $33.51 billion.

For next fiscal year FY22, meanwhile, Wall Street analysts are expecting Palantir to deliver $1.98 billion in revenue, representing 30% y/y revenue growth (data from Yahoo Finance). Considering the company has committed to 30%+ annual revenue growth throughout 2022 (and this is a company that has routinely delivered well ahead of its promises), I'd say this outlook is a little dim. Yet regardless of that, at this revenue estimate Palantir trades at 16.9x EV/FY22 revenue.

Again, we can hardly call this cheap, and in the face of rising interest rates, certainly Palantir's prior valuation multiples in the high-20s were unsustainable. But given this company's rapid growth trajectory, I'd say the ~$18 price level still represents a great entry point for the longer-term investor.

Q3 results showcase tremendous fundamental traction, especially in the commercial segment

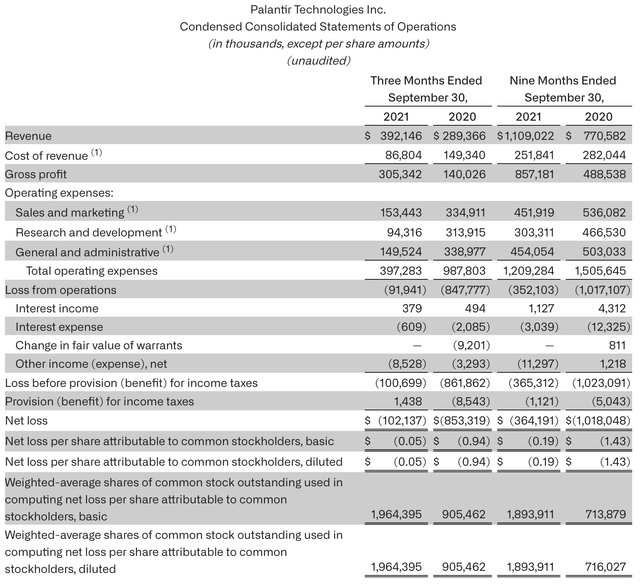

We additionally note that Palantir's end-of-year correction has been accompanied by a continuation of its strong fundamentals. Take a look at the Q3 earnings results below:

Figure 3. Palantir Q3 results

Palantir's revenue grew at a robust 35% y/y pace to $392.1 million in the quarter, beating Wall Street's expectations of $386.6 million (+33% y/y) by a two-point margin. We note that revenue growth did decelerate versus 49% y/y growth in Q2, but that's largely due to an easier comp versus the pandemic period in Q2 of last year.

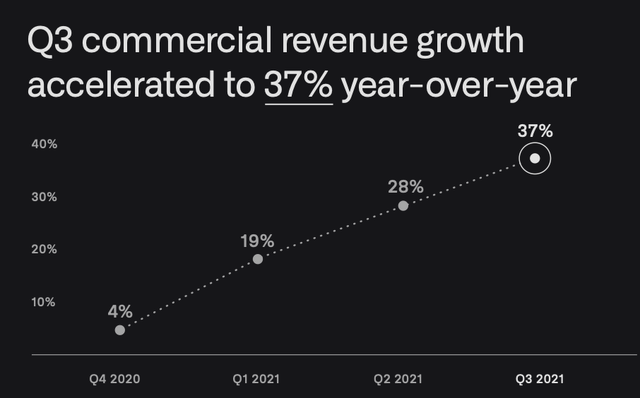

The major highlight in Q3 was Palantir's success in driving enterprise go-to-market. The company reported commercial revenue growth of 37% y/y in Q3 - which, despite tougher comps, represented substantial acceleration over the prior few quarters:

Figure 4. Palantir commercial revenue trends

We note as well that when counting U.S. commercial revenue only, Palantir grew domestic enterprise revenue at a blazing 103% y/y pace.

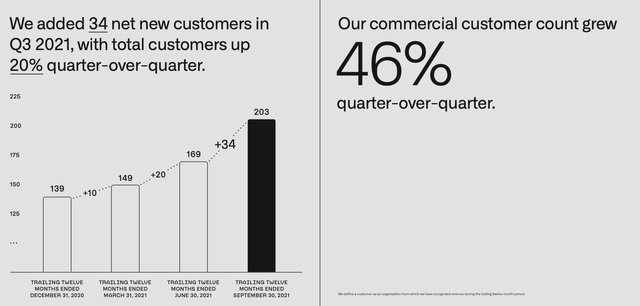

Note as well that as of the moment, Palantir remains a relatively early-stage enterprise software vendor with relatively few, but large customers. Q3 saw the biggest customer expansion in Palantir's history. The company added 34 net-new customers in Q3 to end the quarter at 203 total customers, which is a significant 20% expansion in the company's customer base in the space of a single quarter. Year over year, the company also boosted its commercial customer counts by 46%.

Figure 5. Palantir customer adds

Recall as well that for its enterprise customers, Palantir adopts a "land and expand" playbook that many SaaS companies adhere to. These customers may start off as smaller deployments that grow substantially over time.

Equally worth noting is that Palantir's billings expanded 56% y/y to $347 million. The surplus of Palantir's billings growth rates over its revenue growth, plus the sharp buildup in its remaining performance obligations, give us confidence that the company will be able to make good on its promise of sustaining 30%+ revenue growth for years to come.

Lastly, a word on profitability. Palantir's customer growth, and at a positive contribution margin as well, has driven the company to dramatically boost its adjusted free cash flow. In Q3, adjusted FCF hit $119 million, or a ~30% adjusted FCF margin - versus cash burn of -$53 million in the prior-year period.

Figure 6. Palantir FCF trends

Building on the strength in cash flow that the company has seen all year, Palantir management also increased its annual FCF guidance for FY21 to $400+ million, versus a prior outlook of just $300+ million. These moves, in my view, solidify to investors in a very risk-off market mindset that Palantir isn't just growing robustly, but also keeping profitability balance in mind.

Key takeaways

In my view, Palantir retains a very long runway for success. The company's undisputed category leadership in big data and analytics continues to prove out new use cases for both public and private-sector teams, and the fact that Palantir can continue to grow at >30% y/y despite hitting an expected ~$2 billion annual revenue run rate next year further solidifies that Palantir is a unique and rare story in the software sector. Take advantage of the ~30% correction since November to build up a well-timed position in this stock.