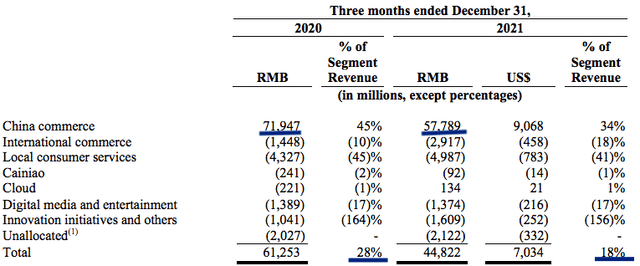

Alibaba (NYSE:BABA) had reported a big decline in its EBITA within core commerce business in the last quarter. Core commerce in China is the biggest contributor to its profit and hence we saw a massive dip in Alibaba’s income and margin in the last quarter. This margin decline could continue in the near term as the restrictions due to the pandemic are still being imposed on major cities. Alibaba’s EBITA in core commerce came at RMB 57.8 billion, down from RMB 71.9 billion in the year-ago quarter. Most of this decline was due to higher investment in Taobao Deals, Community Marketplaces, Local Consumer Service and Lazada.

We should see better margins in the medium term as the competitive pressure declines due to lower investment by Tencent (OTCPK:TCEHY) in Alibaba’s rivals like JD.com (JD), Pinduoduo (PDD), Meituan, and others. Alibaba’s cloud platform will also be the main driver for margin expansion over the next few quarters. Even with a lower margin in this earnings call, Alibaba could see better bullish sentiment if it continues to show strong progress in cloud, international regions, subscriptions, delivery, and other key business segments.

Decline In Margins

The decline in margins within core commerce business is due to ramping up of investments in several strategic initiatives. The growing competition from Pinduoduo forced Alibaba to launch Taobao Deals where the margins are low. This service already has over 240 million annual active customers. Alibaba also invested in Ele.me to improve its delivery network. Another big investment activity was in Lazada in Southeast Asia. Lazada is competing against Sea Limited and Alibaba has set a target to hit $100 billion gross merchandise value within this business.

Alibaba Filings

Figure 1: Decline in core commerce EBITA is driving the overall margins lower.

The margin decline in commerce segment was quite high. The overall EBITA margin in the year-ago quarter was 28% which declined to 18% in the last quarter.

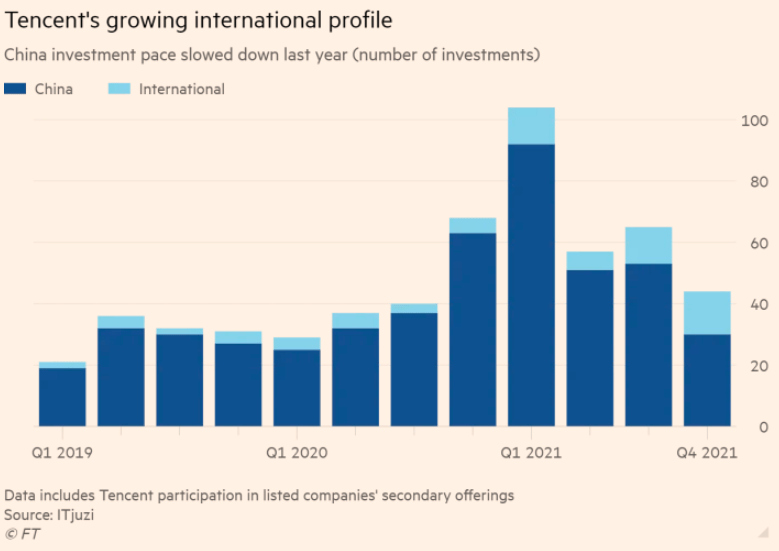

Tencent's Withdrawal

Tencent has seen significant regulatory headwinds in recent quarters. It is Alibaba’s main rival which has invested in a number of companies that directly compete with Alibaba. Tencent is now trying to divest its stake in these companies to prevent antitrust action by regulators.

It has already announced a reduction in stake in JD from 17% to 2.3%. There could also be a reduction in strategic partnership where JD uses Tencent’s platform to improve its service. Tencent might also divest from PDD, Meituan and other startups. At the same time, Tencent is increasing investment outside China. This will reduce the competitive pressure on Alibaba in several business segments.

Financial Times

Figure 2: Lower investment by Tencent in China.

Importance Of Cloud Business

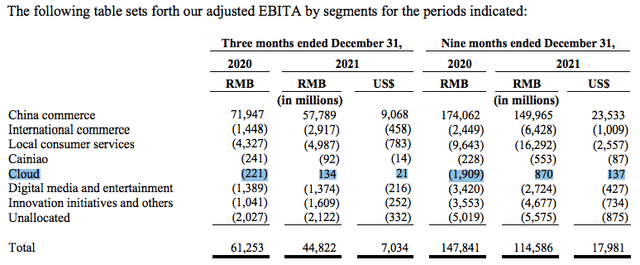

Alibaba Cloud is already showing annualized revenue rate of $12 billion.

Company Filings

Figure 3: Improvement in cloud business compared to year ago quarter.

In the nine months ending December 31, 2020 Alibaba reported EBITA of negative RMB 1.9 billion. In the latest nine-month period this has changed to positive RMB 0.87 billion. The margin swing in this period was from negative 4% to positive 2 %. Many cloud providers have struggled with lower margins in the initial stages. After reaching a higher revenue base, they are able to leverage the economies of scale to deliver better margins.

We have already seen this in Google's ((GOOG)(GOOGL)) cloud business. Google was able to deliver a 16 percentage point improvement in margin on a YoY basis in the previous quarter. Alibaba should also be able to show improvement in cloud margins as the revenue base increases and we see better economies of scale.

Another factor working in favor of Alibaba Cloud is the rapid international growth shown by the company. Recently, Alibaba opened its third data center in Germany and it now directly competes with Amazon (AMZN), Microsoft (MSFT), Google, and other cloud providers in the lucrative European region. It should be noted that Alibaba Cloud has many features which are similar to Amazon's AWS because both of these cloud operations started with their e-commerce business. This makes it easier for clients to use Alibaba Cloud instead of AWS in case they get better discounts.

Many clients are focusing on using the services of multiple cloud providers instead of a single cloud company. This should help Alibaba Cloud gain market share as clients try to diversify their cloud providers.

Amazon Filing

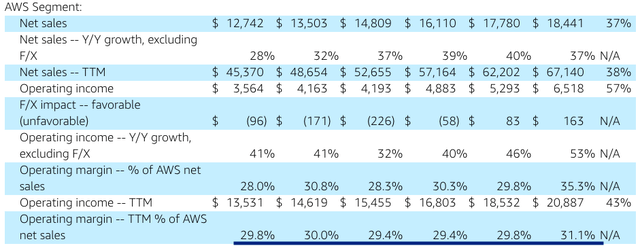

Figure 4: Amazon's AWS has shown operating margin of close to 30% in the last few quarters.

Amazon’s AWS regularly shows operating margin of 30%. There is a massive margin gap between Alibaba Cloud and AWS. Alibaba Cloud has already shown an improvement of six percentage points in margins in the first three-quarters of this fiscal. Further improvement is likely as Alibaba ramps up its international investment in cloud business.

Hence, we should see a lot of margin improvement in Alibaba Cloud due to better economies of scale, international expansion, and usage of multiple cloud providers by clients, and thereby see a reduction in margin gap with AWS.

Are Margins Important?

If Alibaba can show rapid growth in international regions, the margins might take a back seat for Wall Street in evaluating the stock. The company is trying to replicate the business model it has created within China in other locations. It tries to gain a good share of the ecommerce market in a new region and then launches other services like payment, cloud, delivery, subscriptions, etc. within these locations. Alibaba has already proven itself in Southeast Asia. It owns Lazada which is a major player in the ecommerce market of Southeast Asia.

Lazada had $21 billion gross merchandise value according to recent estimates compared with Sea Limited which had $35 billion GMV. Sea Limited is trading at close to $50 billion market cap. Hence, Lazada could also have a massive standalone valuation. Alibaba also owns a big stake in Trendyol which is the leading e-commerce company in Turkey with a valuation of over $16 billion.

By end of this decade, Alibaba’s international business could be worth more than its Chinese business. During the expansion phase in international regions, the margins will suffer as the company tries to invest in warehousing, logistics and attracts new customers through discounts. Wall Street might overlook margins in this period if Alibaba’s management can deliver high enough growth in international markets. The recent YoY growth in Lazada was 82% which shows that heavy investment can bring a strong growth from a high revenue base.

Impact On Stock

Alibaba is trading at a modest valuation multiple even if we price in the regulatory challenges faced by the company. The company has a number of growth drivers that it can use to deliver better numbers in the future. The core business is still very strong and it has been able to retain its market share despite the growth of innovative disruptors like PDD.

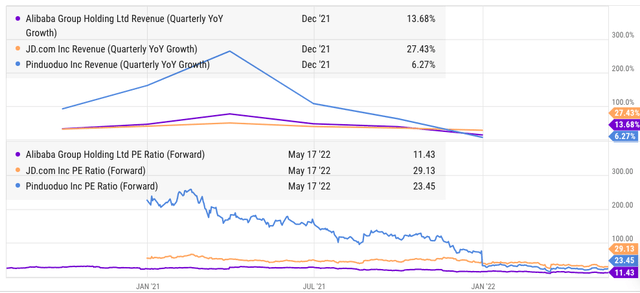

Ycharts

Figure 5: Alibaba's forward PE ratio is considerably lower than that of JD and PDD.

The revenue growth is still strong in a number of important businesses like cloud, international commerce, Ele.me and others. The forward P/E ratio of Alibaba is close to single digit which does not reflect the core strengths. We could still see some margin headwinds due to pandemic restrictions in the near term. However, in the medium to long term, the revenue growth and margin potential of the company are promising.

Investors should look past the short-term margin fluctuation and gauge the long-term growth of important segments like cloud, international commerce, subscriptions, and competition with Tencent.

Investor Takeaway

Alibaba has seen a dip in margins as the company invests in its strategic initiatives. We should see lower competitive pressure on Alibaba in the medium term as Tencent reduces its stake and partnership in JD, PDD, Meituan and others. Tencent is also directing more investment in international regions which should be favorable for Alibaba in China. Alibaba’s cloud business will be the main margin driver in the next few quarters.

Alibaba’s international growth will also put less attention on the margins. If Alibaba can rapidly expand in Southeast Asia and Europe across services like ecommerce, cloud, payments, delivery, and others, then it can improve the long-term growth runway for the company.