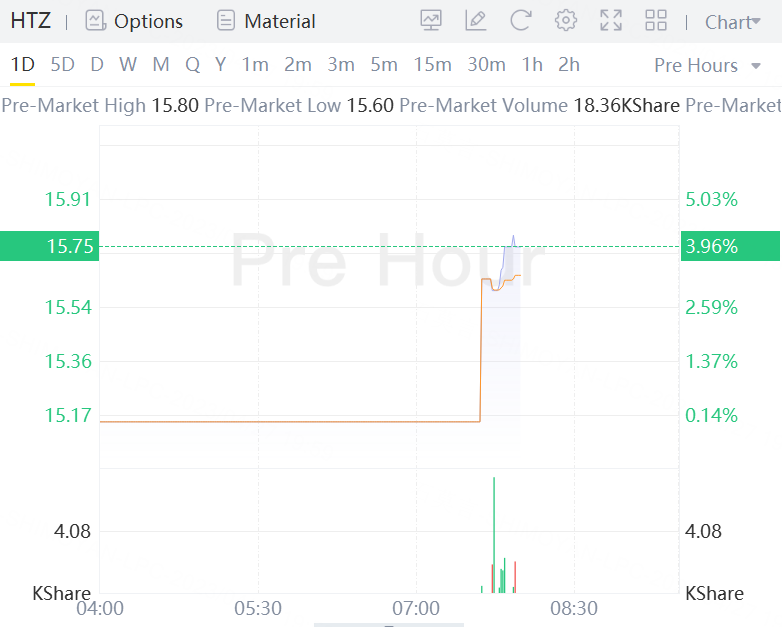

Hertz Global Holdings Inc.'s stock $(HTZ)$ rose nearly 4% premarket Thursday, after the car-rental company posted better-than-expected first-quarter earnings, even as net income fell from a year ago. Estero, Fla.-based Hertz had net income of $196 million, or 61 cents a share, for the quarter, down from $426 million, or 82 cents a share, in the year-earlier period.

Adjusted per-share earnings came to 39 cents, ahead of the 19 cent FactSet consensus. Revenue rose to $2.047 billion from $1.810 billion a year ago, ahead of the $2.013 billion FactSet consensus.

The company's costs rose to $1.985 billion from $1.254 billion a year ago, as it continued to invest in technology including electrification, The company, which went bankrupt during the pandemic when shutdowns crushed demand for its cars, said it ended the quarter with $2.2 billion of liquidity, including $728 million in unrestricted cash.

The stock has fallen 1.6% in the year to date, while the S&P 500 has gained 5.6%.