Bank Of America: A Value Trap

Summary $Bank of America(BAC)$

- Bank of America has pro-cyclical investment characteristics.

- Bank of America will likely see a spike in net charge-offs in a recession.

- The bank’s stock is unlike to trade at a premium to book value during if economic prospects falter.

Evidence of a recession is mounting, implying that pro-cyclical investments such as Bank of America will generate negative returns in the future.

Since March, the central bank has also become much more aggressive inraising interest rates, which is expected to harm the financial industry's profitability.

With recession risks increasing, Bank of America's stock faces a potentially toxic cocktail of higher interest costs, higher net charge-offs, and declining consumer business strength.

Prepare For A Downturn In Consumer Banking

Consumer Banking trends (mortgages, credit cards, payment volumes) were assisting the company's recovery following the Covid-19 pandemic.

These trends included sharp increases in total loans and leases, with Bank of America's total loans and leases having recovered to pre-Covid levels by the end of the first quarter.

Total Loans And Leases(Bank of America)

Bank of America's Consumer Banking division profited significantly from pent-up demand following the pandemic, and the business reported strong first-quarter financial results.

Bank of America's first-quarter profits were fueled by a strong performance, primarily in Consumer Banking: this unit earned$3.0 billion in profitsin 1Q-22, up $294 million from the previous year. Consumer Banking is Bank of America's most profitable business unit, and its success is based primarily on consumers' willingness to spend money.

Consumer Banking Income(Bank of America)

Asset Quality Trends

Bank of America's asset quality on the balance sheet has not yet deteriorated, but if the U.S. economy were to enter a recession, it would only be a matter of time before investors saw a significant increase in the bank's net charge-off ratio, as it has in previous recessions.

The net charge-off ratio distinguishes between gross charge-offs and recovered debt. As a result, the net charge-off ratio quantifies the amount of debt that delinquent borrowers are unlikely to recover. Bank of America's net charge-off ratio was 0.16% in the first quarter, indicating that the balance sheet's financial assets are of good quality so far.

Having said that, Bank of America's net charge-off ratio is expected to rise if the economy enters a slump and borrowers struggle to pay their bills on time.

Net Charge-Offs(Bank of America)

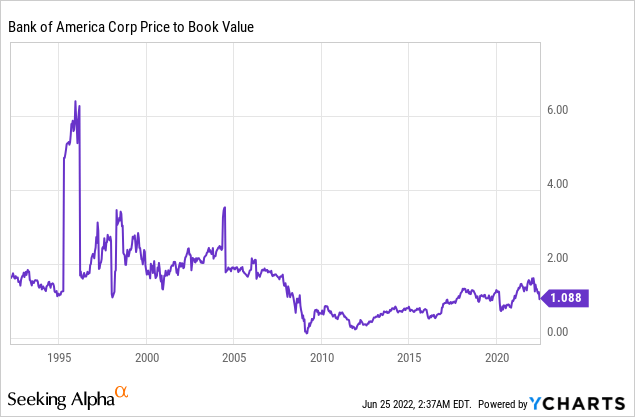

Bank of America Is Not Going To Trade At A Premium To Book Value In A Recession

The United States' gross domestic productfell 1.5%in the first quarter. A second consecutive decline in GDP in the second quarter would officially place the U.S. economy in recession. The first-quarter GDP decline was the first since the 2Q-20, when the economy contracted sharply due to the emergence of the Coronavirus.

Percent Change In GDP(Bank of America)

Most Wall Street analysts now predict a recession in 2023, but I believe we are already in one. If the reading of 2Q GDP data indicates that the U.S. economy is already in a recession, bank stocks in particular may be in for a lot more pain as investors exit cyclical investments.

The issue with Bank of America is that its stock has not traded at a premium to book value during previous recessions, implying that the bank could be in for a major earnings slump, particularly in the economy-dependent Consumer Banking unit. Bank of America currently trades at a 13% premium to book value. During previous contractions, the stock traded at steep discounts to book value.

Why Bank of America Could See A Higher Stock Price

Why Bank of America Could See A Higher Stock Price

Of course, the market's expectations of a recession could be completely wrong. If a recession is avoided, Bank of America's Consumer Bank will likely perform well, asset quality will remain high, and the stock price may rise. An unexpected drop in interest rates, which helps the debt-dependent financial sector, would almost certainly be beneficial to Bank of America.

My Conclusion

I believe Bank of America is a value trap here, and I don't see it producing positive stock returns for investors as the economy appears to be heading for a recession.

Simultaneously, higher interest rates risk pushing the economy into a recession, which will have an impact on Bank of America's profit growth, asset quality, and book value multiple.

Bank of America's risks have increased significantly since the central bank raised interest rates in 2022, and investing in pro-cyclical financial investments at the start of a recession may not be a wise move.

source: seekingAlpha

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- KwLau·2022-06-27Buy and keep for long term.LikeReport

- Sporeshare·2022-06-27waiting for fund to come in and push it higherLikeReport

- GOH87·2022-06-27Goo d2Report

- LI_CHUN·2022-06-27

![[呆住]](https://c1.itigergrowtha.com/community/assets/media/emoji_004_daizhu.a66c6320.png) LikeReport

LikeReport