2023 Outlook: The big adjustment is underway!

TL;DR: Capital prevention required, diversification needed, monetary tightening and deleveraging continue, markets need time to adjust, and the world needs economic freedom

2022 was terrible for most investors. So naturally, everybody hopes that things will change for the better in 2023. However, there is no place for hope in the markets. If you want to succeed as an investor, you have to learn from what the market provides us with and continue to evolve. So yes, crystal ball projections are fun; we surely have ours. But learning and adjusting are what makes the difference for us investors.

Last year, we wrote our 2022 Outlook. We developed 9 theses for the markets. Surprisingly, most of them are still true today:

#1 Monetary Cycle ending? -> Yes, tightening continues in 2023

#2 Inflation is here to stay -> Yes, and it’s not transitory, we are in the middle of it

#3 High Valuations -> Yes, remaining high even after 2022’s correction

#4 COVID forever -> Yes, we learned to adjust and live with

#5 Geopolitical autumn -> Yes, turning into a winter

#6 Technology as growth drivers -> Yes but no straight line up

#7 Crypto, Gold, and the inflation hedge puzzle -> Crypto is no hedge

#8 In a bull market, everybody is a genius -> Yes, see performance of previous high-flyer funds (=disaster)

#9 Diversification is more important than ever -> Yes, the broader, the better

Here are our 6 theses for 2023:

#1 Capital prevention first!

It is not the time to be a hero. 2022 should have reminded investors about the most basic principle of investing: Capital preservation first, capital growth second. If you don’t have any money, how do you want to grow it? Successful investors control their portfolio drawdowns and retain a high equity base level; then, they can compound returns. You can control your drawdowns by applying disciplined money management and position sizing, using stop losses, or hedging your portfolio with options and other leveraged products.

If you don’t have any money, how do you want to grow it?

#2 Diversification: Stocks and bonds are not enough

Following the “everything bubble” of the early 2020s, 2022 surely qualifies as the “everything sucked” year in the market. Besides commodities, the US Dollar, and cash, there were no major asset classes with positive returns (which does not happen very often!).

2022 has shown us that successful investing is more than holding some kind of a traditional stocks/bonds portfolio. And no, holding various tech stocks and cryptocurrencies also don’t count as diversification. The key to diversification is to be invested in asset classes with uncorrelated (or low-correlated) returns. There are two advantages to this approach:

- It lowers your portfolio risk by spreading money across and within different asset classes; if one doesn’t perform well, the other might.

- The more asset classes monitored, the higher the chances of capturing a strong trend with outsized returns.

In addition to stocks, bonds, commodities, and real estate, FX (foreign exchange), Bitcoin, Carbon, Tail Hedge, and CTAs (e.g., via DBMF) are good examples. Farmland or collectibles are also interesting, despite being less liquid.

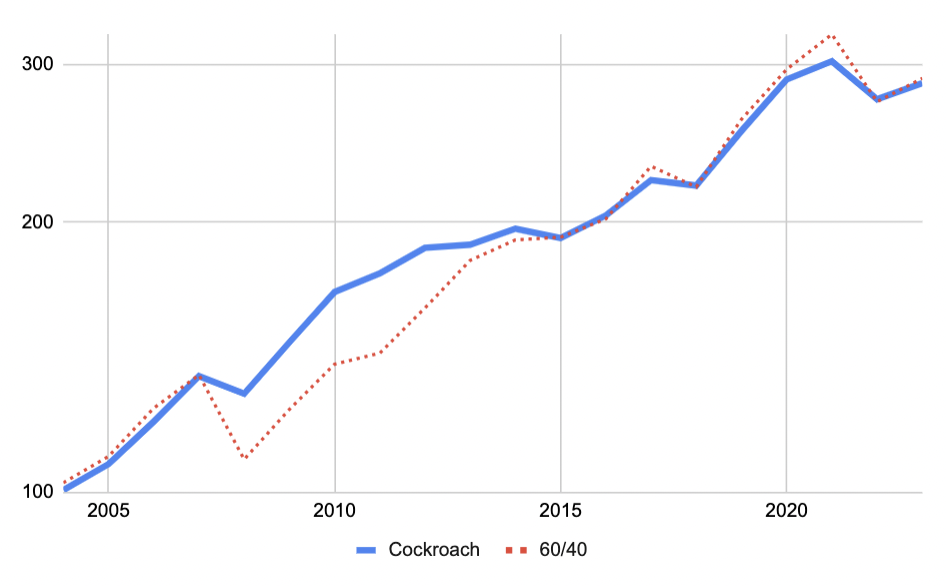

Here is one simple example: The Cockroach Portfolio.

The Cockroach Portfolio is the simplest, most inexpensive, and lowest effort way to diversify a portfolio. The Cockroach Portfolio holds 25% stocks, 25% bonds, 25% cash, and 25% Gold. In 2022, it only lost -9%, while a 60/40 stocks/bonds portfolio was down -16%. It achieved this relative outperformance with a max. drawdown of only -16% (vs. -35% 60/40). This is a great example of how to profit effortlessly from the benefits of very basic diversification. The chart below shows the long-term performance of the Cockroach Portfolio vs. a Global 60/40.

#3 Liquidity is driving the market (down)

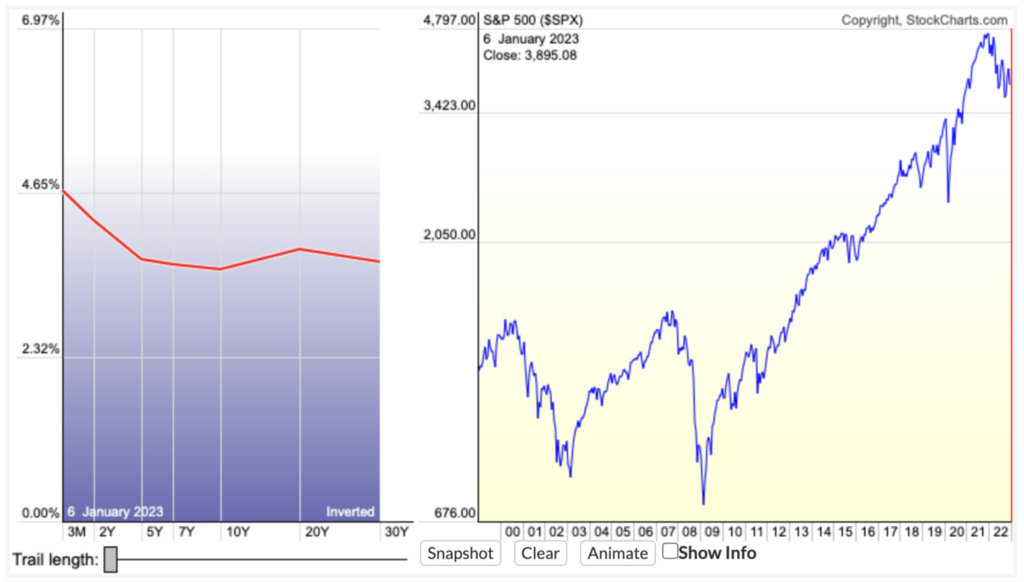

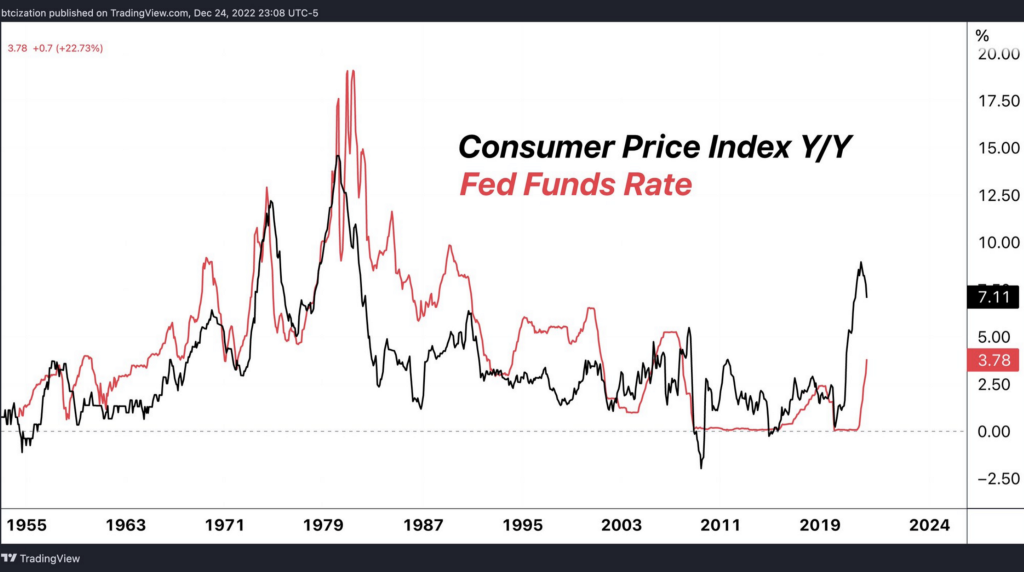

Ever since reading The Theory of Money and Credit by Ludwig von Mises, I have believed interest rates are the main driver of the economy and the markets. Big cycles, and hence regime changes, result from monetary policy. At the beginning of 2023, the U.S. yield curve is inverted. In all cases, an inverse yield curve is followed by a recession.

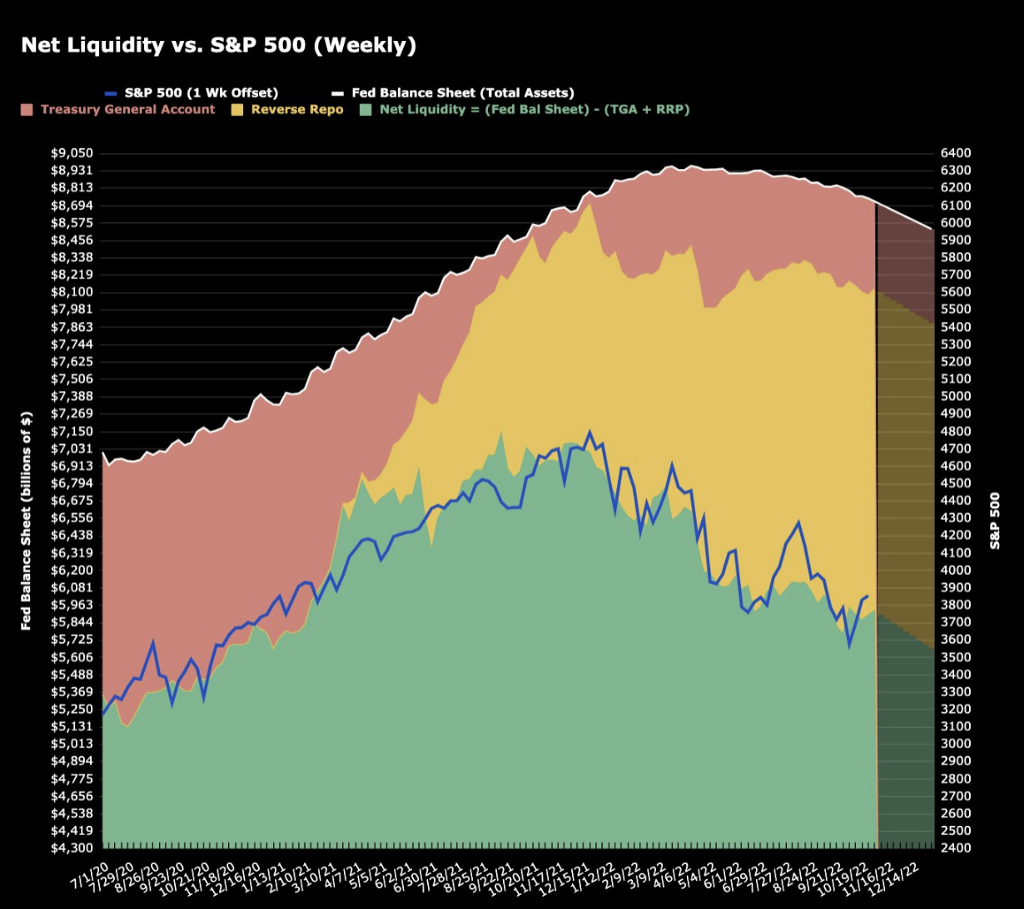

Ok, I get it; the yield curve is a pretty abstract concept. So let's make it more tangible. The media is full of narratives about why the market is up or down (mostly in 2022). Geopolitical risks, the war in Ukraine, Inflation, the energy crisis, etc. However, the market has always been driven by liquidity. When liquidity gets injected into the system, markets go up. When liquidity gets removed, the market goes down. The chart of Net Liquidity vs. S&P 500 chart shows exactly that. We are in times when liquidity gets reduced.

We are currently in a rising rate cycle (falling liquidity). This is true for the U.S. and almost all countries worldwide. Massive money printing since the great financial crisis in 2008 and great fiscal spending during the COVID crisis has led to the “everything bubble” and — eventually — rising inflation worldwide. Now, central banks are working hard to remove the excess liquidity they have created.

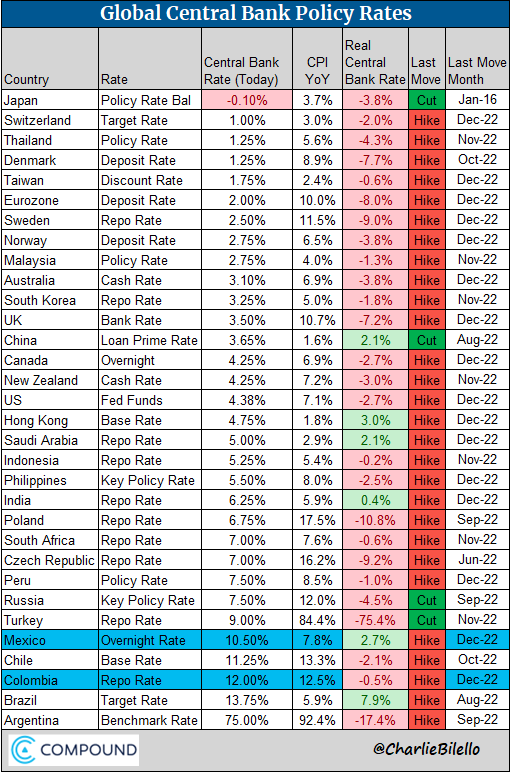

How long will the cycle of rising rates continue? In the U.S., once inflation gets above 5%, it never comes down unless the Fed Fund rate is higher than the CPI (i.e., interest rates > inflation). There is still a gap of more than 3%. We cannot predict the future, but based on these observations, we should expect 2023 to be rocky and challenging.

China’s reopening, breaking supply chains, environmental laws and regulations (they cost money), and protectionism put upward pressure on prices; some analysts believe that this could lead to 4–5% inflation rather than the 2% targeted by Western central banks.

#4 Deleveraging continues

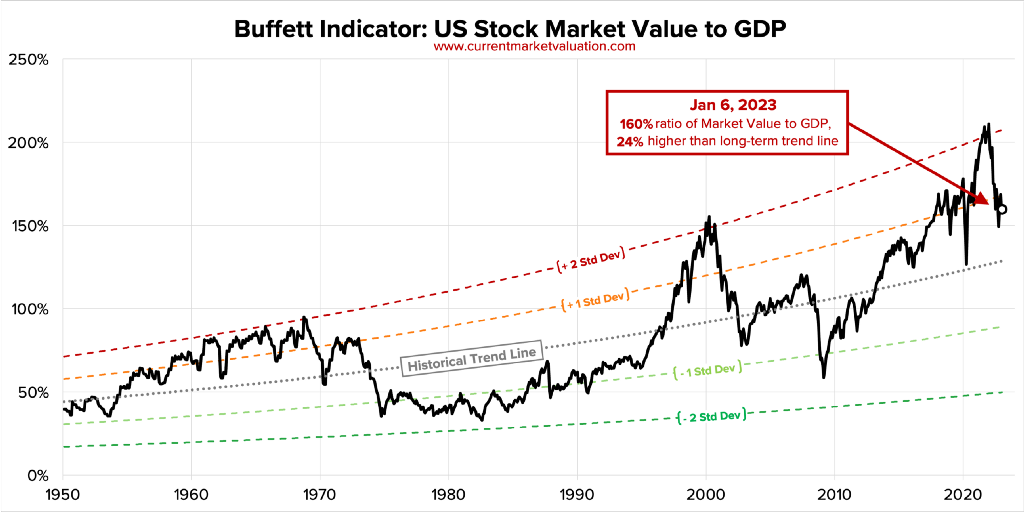

By many measures, global valuations are still above their long-term trends. For example, Shiller’s PE Ratio is at 28, way above the average range of 15–20.

Another popular indicator is the popular Buffett Indicator. It measures the value of U.S. stocks in relation to the economy. In 2022, it came back from its stretched levels but is still about 1 Standard Deviation above its historical average.

How will this deleveraging happen? Nobody knows for sure. There can be a relatively short crash or a longer downtrend. For me, it’s clear that companies all over the world are right-sizing to match the new regime we are in. The faster this adjustment process takes place, the better. To return to growth, we need to see a change in global monetary policy in combination with more attractive valuations. For now, we agree with AQR’s Cliff Asness, who concludes that the bubble has not popped.

# 5 Things take longer than you think/wish

Markets are the result of human action. Patterns we experience in our daily lives, we also see in the markets. A general observation is that things usually take longer than we think. There is a lot of hope that the downturn ends and things will return to “normal”. Didn’t stocks and bonds already fall enough? Didn’t valuations come down enough that VCs are interested in investing again? Aren’t the company’s cost-saving initiatives, especially in the tech sector, enough? In the summer of 2022, we asked: Where is the bear? If this is a true regime shift, we have not seen a true bear market. It takes time for rising interest rates to work their way through the economy. Here is why:

- Fundamentally, the value of a company or an investment is the present value of future cash flows (i.e., money earned in the future worth today). Future cash flows are discounted at the discount rate, and the higher the discount rate, the lower the present value of the future cash flows. The basis for all discount rate calculations is the interest rate set by the central bank. So everything else equal, if interest rates rise, the present value of the future cash flows decreases (= worth less!).

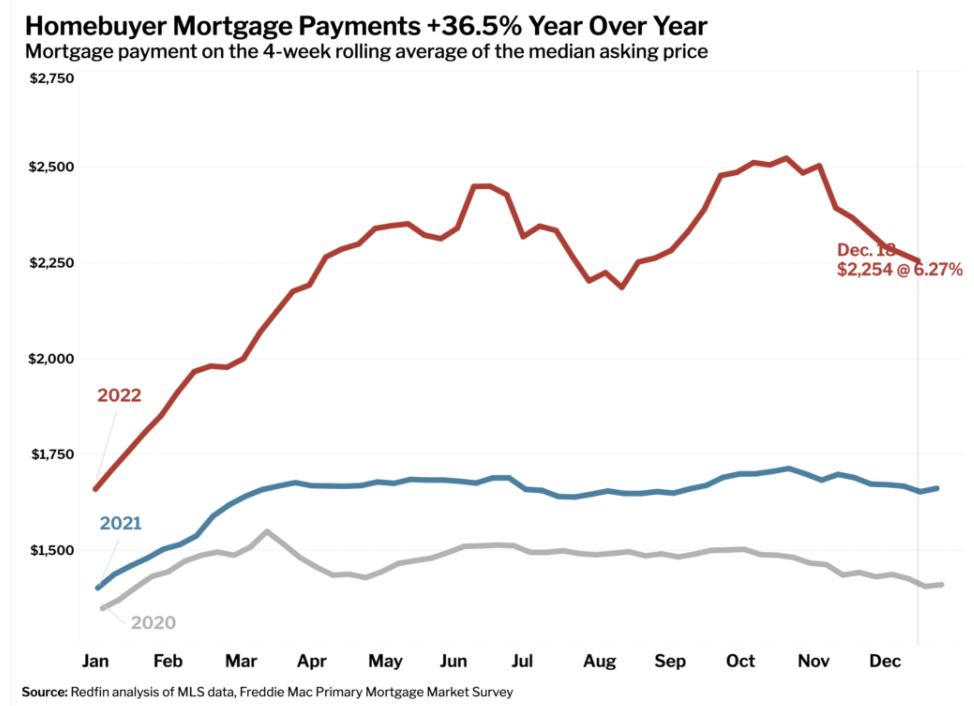

- So why do rising rates take so long to tickle through the economy? Take real estate as an example. The increase in interest rate cause mortgage rates to rise. In the U.S., mortgages are above 6% now. Rising mortgage rates decrease home buying demand, leading to a fall in home prices. But all of this takes time. New mortgages get more expenses; they almost double to $2,300 per month in the U.S. It also increases the cost of refinancing properties and the cost of properties financed with variable rates. So demand drops first, but prices of supply (i.e., offered properties in the market) take time to adjust, depending on the circumstances in each market. Sellers will eventually adjust (decrease) prices, but this takes time, depending on how desperate sellers are.

Another example is VC or P/E investments. You often hear that private investments are less volatile than public ones. However, they are still equity investments. The fact that they are private protects them from daily valuations but doesn’t protect them from adjustments in valuations. Illiquidity simply slows down the process of adjustment; it doesn’t avoid it.

Illiquidity simply slows down the process of adjustment; it doesn’t avoid it

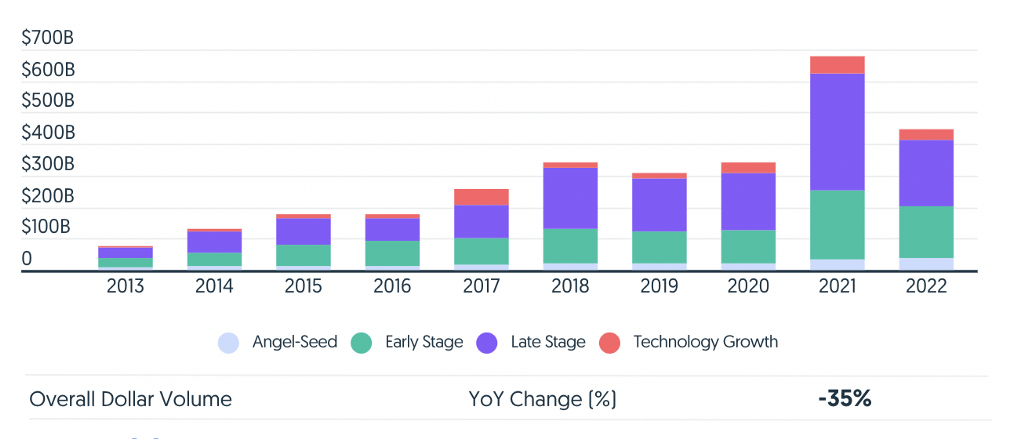

The “everything bubble” of the 2020s was just crazy for private investments. Think of all the not-so-innovative-companies which got hyped and funded. Remember how SPACs and NFTs were golden tickets to cash? That is what happens in an “everything bubble”. Looking at the data, venture and growth investors scaled back their investment pace significantly in the latter half of 2022. According to Crunchbase data, global venture funding in 2022 reached $445bn, a -35% YoY decline from the $681bn invested in 2021. There are so many implications of this. Eventually, the dry powder funds have will be deployed, and due to lacking returns of recent vintage years, LPs will scale back their investment in private funds;

P/E and VC funds will raise smaller funds -> funding rounds will decrease -> number of investments will decrease -> less competition for funding -> lower valuations. That is the normal market process of adjusting. In the private sector, it just takes longer.

The chart of the Global Venture Dollar Volume from 2013 to 2022 shows that funding slide in 2022 sets the stage for another tough year.

#6 What to hope for in 2023

The market is providing us with all the signals we need. It is up to us to read and interpret them unbiasedly and draw the right conclusion. Diversification, trend-following, and compounding returns remain the ingredients for success in investing. However, we must remember that freedom and liberty are the major forces driving us to the highest standard of living in human history. Freedom, based on the ideas of classical liberalism, has been the main driver for the success of the last decades.

If we want to secure long-term success and prosperity, we have to return to freedom and peace.

Unfortunately, our world has been developing in the opposite direction for the last few years. There are increasing government interventions around the world, wars, and the rise of surveillance states. Who wants to live in a surveillance state or under a dictatorship? It’s time for people to wake up. These forces come at the expense of free choice. It is not the finest hour for liberty and freedom. If we want to secure long-term success and prosperity, we have to return to freedom and peace. The cornerstones of economic freedom are (1) personal choice, (2) voluntary exchange coordinated by markets, (3) freedom to enter and compete in markets, and (4) protection of persons and their property from aggression by others.

This is a pretty long outlook, but there is too much going on in the world now.

- Society: Only a free economy can provide long-term property for all. The pendulum has to swing from increasing government intervention back toward freedom.

- Markets: As long as the cycle of globally rising rates continues, equity and bond markets will face headwinds. The ride continues to be bumpy.

- Companies: As Ray Dalio puts it, over the long term, being productive and having healthy income statements (earning > spending) and healthy balance sheets (assets > liabilities) are the markers of financial health. Many companies are still in this adjustment process. It’s highly painful and will likely continue in 2023.

Best,

Sebastian

2023 Outlook: The big adjustment is underway! was originally published in DataDrivenInvestor on Medium, where people are continuing the conversation by highlighting and responding to this story.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- EvanHolt·2023-02-06You're right. I also think the market is becoming less liquidLikeReport

- DonnaMay·2023-02-06Do you think it's still a good time to invest in commodities?LikeReport

- BellaFaraday·2023-02-06Improving portfolio diversification is really what we need to doLikeReport

- zerolih·2023-02-06very informative [Like]1Report

- Helen1229·2023-02-06👍🏻👍🏻👍🏻👍🏻1Report

- CaesarHicks·2023-02-05In 2023, the market will be much different from 2022, just change our mind.LikeReport

- PandoraHaggai·2023-02-06Owning tech stocks is definitely not a smart moveLikeReport

- Maria_yy·2023-02-06Stocks and bonds alone look safe enoughLikeReport

- Tantiad·2023-02-06Ok1Report

- xiaochoochoo·2023-02-06👍LikeReport

- Johnsnny·2023-02-06OkLikeReport

- Lamborghini1·2023-02-06👍1Report

- ken2020·2023-02-06[Like]1Report

- Hosay_hosay·2023-02-06[Cool][Cool]1Report

- StaQ·2023-02-06ok2Report

- Michael8208·2023-02-05[Great]LikeReport

- 淋淼淼·2023-02-05OkLikeReport

- NgKenny·2023-02-05NiceLikeReport

- neosh·2023-02-04ok....LikeReport

- Huey8·2023-02-04thanxLikeReport