It is expected that the revenues of U.S. big banks will grow moderately in Q4. Higher interest rates have helped boost interest income. As the stock and bond markets have slumped, Noninterest income may decline.

Fourth-quarter earnings season is set to begin in earnest during the second full week of January, led by banking giants JPMorgan Chase (JPM), Bank of America (BAC), Wells Fargo (WFC) and Citigroup (C). With another round of bank earnings just around the corner, what can investors expect to see?

Over the past few weeks, inflation has come down and the U.S. Federal Reserve is expected by some to pivot to a less aggressive stance. There is optimism that this will not be a long-lasting recession, and that pressure on the consumer from inflation and interest rates will ease. Even if this outlook proves to be overly optimistic, it is still expected good results from the banks, with decent earnings and attractive dividend yields. It’s uncertain whether it will be seen dividend increases, however, as banks wait to see how steep the economic slowdown will be. Trading revenues could be down due to declining markets, but it is expected to see a bit of a pickup on that front on the holiday season.

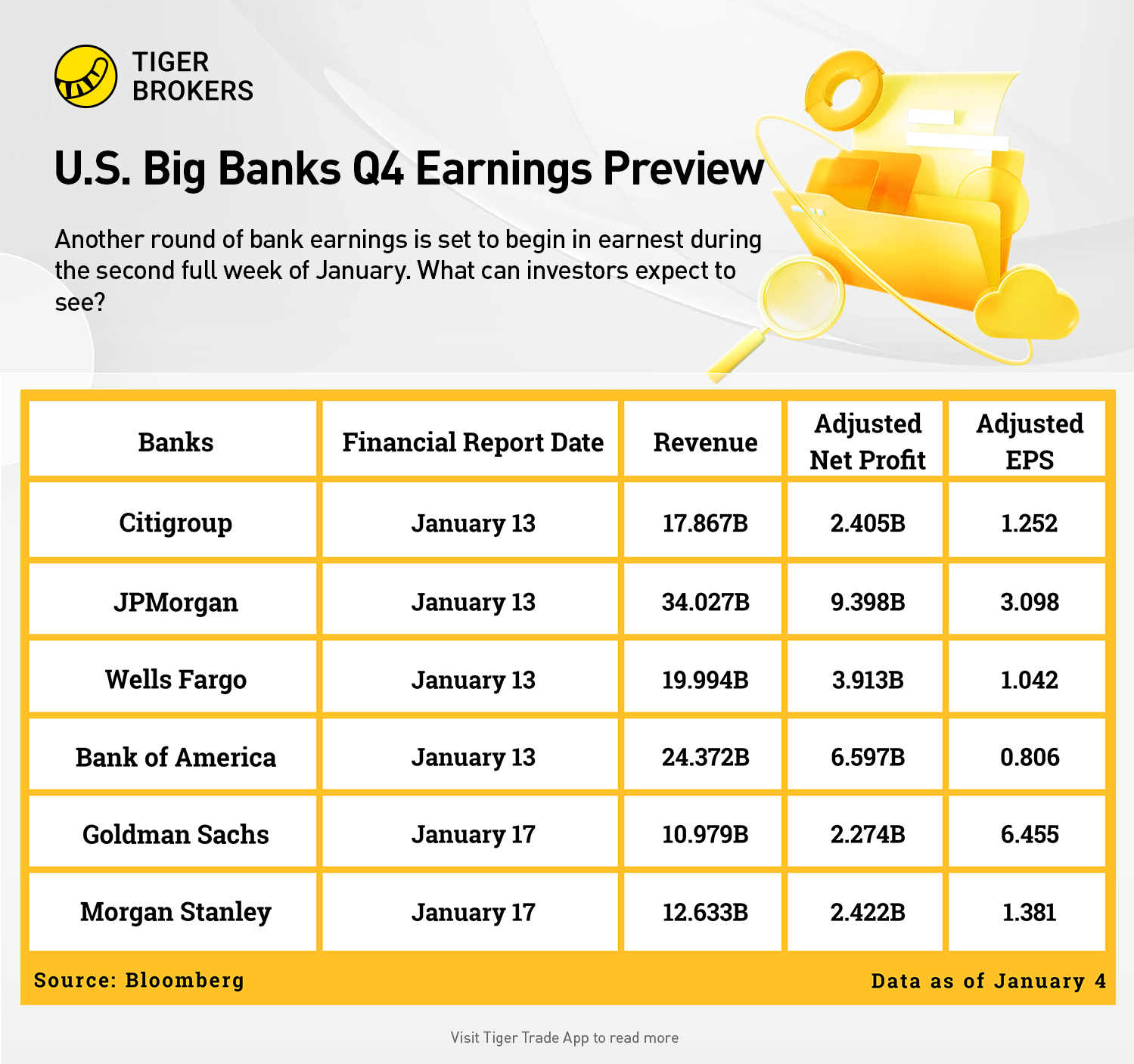

Big Six Banks Earning Expectations

Citigroup is on deck to report fourth-quarter earnings of $1.252 a share on revenue of $17.867 billion, according to Bloomberg consensus.

Analysts expect JPMorgan Chase to report earnings of $3.098 and revenue of $34.027 billion.

Up next is Wells Fargo, which is expected to earn $1.042 a share on revenue of $19.994 billion.

Bank of America is expected to earn $0.806 a share on revenue of $24.372 billion.

Goldman Sachs is expected to report earnings of $6.455 a share on revenue of about $10.979 billion.

Finally, Morgan Stanley is on tap to earn $1.381 a share on revenue of $12.633 billion, according to Bloomberg consensus.

What else should we pay attention to?

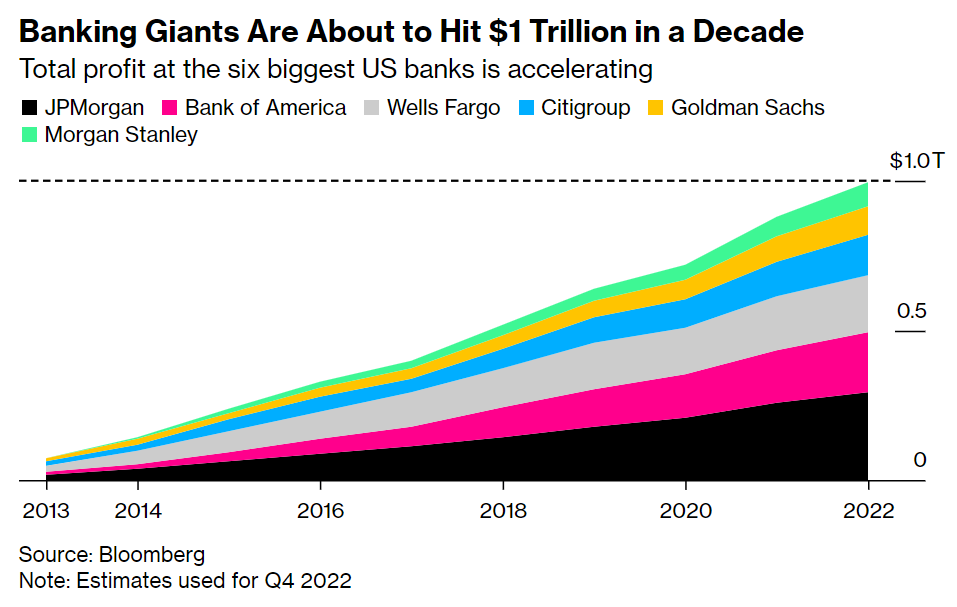

Wall Street’s Big Banks Score $1 Trillion of Profit in a Decade

The six giants of US banking are about to the first trillion-dollar decade. That’s not $1 trillion of total revenue, it’s pure profit. Analyst estimates show the six banks are quickly closing in on that feat — $1 trillion in a 10-year period — and that if they don't reach the milestone at the end of last year, they will sometime in the first few weeks of 2023. It isn’t just the scale of profit that’s so startling, though, but the industry’s ability to push through scandals and thrive anew.

Big Banks Predict Recession, Fed Pivot in 2023

Big banks are predicting that an economic downturn is fast approaching.

More than two-thirds of the economists at 23 large financial institutions that do business directly with the Federal Reserve are betting the U.S. will have a recession in 2023. Two others are predicting a recession in 2024.

To be sure, a majority of the economists who expect the U.S. economy to contract predict it will be a “shallow” or “mild” recession. They expect the economy and U.S. equity markets to rebound late in 2023, thanks largely to the Fed pivoting to rate cuts.

Analyst opinion

Citigroup

Citi price target raised to $61 from $57 at Barclays

Barclays analyst Jason Goldberg raised the firm's price target on Citi to $61 from $57 and keeps an Equal Weight rating on the shares. The analyst believes 2023 should see net interest margins peak for the large-cap banks, deposit betas rise, loan growth slow, and loan losses increase. In addition, banks trade well above tangible book value despite recession concerns, Goldberg tells investors in a research note. As such, the analyst is "becoming less constructive" on banks with "outsized" asset sensitivity and areas he believes loan losses will adjust the fastest, namely, lower-end consumer and commercial real estate. He made several rating changes as part of his 2023 outlook.

Citi price target lowered to $87 from $90 at Oppenheimer

Oppenheimer analyst Chris Kotowski lowered the firm's price target on Citi to $87 from $90 and keeps an Outperform rating on the shares. The analyst believes the banks will prove "steadier than most think" in Q4 and 2023. He does not buy the concern that we are near the peak in net interest income. Higher interest rates are likely to be an ongoing benefit, and loan growth helps too, Kotowski tells investors in a research note. The analyst adds that his models include a near doubling of loan losses as credit trends normalize. The group's "resilience will win out" and multiples will revert to a mid-70s relative price-to-earnings, contends Kotowski. His recommendations include Bank of America (BAC), Citi (C), Goldman Sachs (GS), Jefferies Financial Group (JEF), JPMorgan (JPM), Morgan Stanley (MS) and US Bancorp (USB).

JPMorgan Chase

JPMorgan price target raised to $189 from $162 at Barclays

Barclays analyst Jason Goldberg raised the firm's price target on JPMorgan to $189 from $162 and keeps an Overweight rating on the shares. The analyst believes 2023 should see net interest margins peak for the large-cap banks, deposit betas rise, loan growth slow, and loan losses increase. In addition, banks trade well above tangible book value despite recession concerns, Goldberg tells investors in a research note.

JPMorgan price target lowered to $169 from $174 at Oppenheimer

Oppenheimer analyst Chris Kotowski lowered the firm's price target on JPMorgan to $169 from $174 and keeps an Outperform rating on the shares. The analyst believes the banks will prove "steadier than most think" in Q4 and 2023. He does not buy the concern that we are near the peak in net interest income. Higher interest rates are likely to be an ongoing benefit, and loan growth helps too, Kotowski tells investors in a research note.

Wells Fargo

Wells Fargo price target raised to $64 from $58 at Barclays

Barclays analyst Jason Goldberg raised the firm's price target on Wells Fargo to $64 from $58 and keeps an Overweight rating on the shares.

Wells Fargo price target lowered to $48 from $50 at Citi

Citi analyst Keith Horowitz lowered the firm's price target on Wells Fargo to $48 from $50 and keeps a Buy rating on the shares. The analyst says the company's settlement with the Consumer Financial Protection Bureau a "costly step forward." He refreshed his model to include the expected $3.5B operating loss in Q4. Wells has "sufficient capital to withstand this hit," Horowitz tells investors in a research note. He dropped the price target to reflect greater than expected charges to resolve consent orders.

Bank of America

Bank of America price target lowered to $48 from $51 at Barclays

Barclays analyst Jason Goldberg lowered the firm's price target on Bank of America to $48 from $51 and keeps an Overweight rating on the shares.

Bank of America price target lowered to $51 from $52 at Oppenheimer

Oppenheimer analyst Chris Kotowski lowered the firm's price target on Bank of America to $51 from $52 and keeps an Outperform rating on the shares. The analyst believes the banks will prove "steadier than most think" in Q4 and 2023. He does not buy the concern that we are near the peak in net interest income.

Goldman Sachs

Goldman Sachs downgraded to Peer Perform from Outperform at Wolfe Research

Wolfe Research analyst Steven Chubak downgraded Goldman Sachs to Peer Perform from Outperform without a price target. The mid-point of the analyst's fair value range of $388 supports 13% upside to the shares. Chubak views Goldman's valuation on a price-to-earnings basis as "more full" and says Basel IV poses a threat to its returns and multiple. The analyst also sees downside risk to 2023 and 2024 consensus estimates.

Goldman Sachs price target raised to $495 from $410 at Barclays

Barclays analyst Jason Goldberg raised the firm's price target on Goldman Sachs to $495 from $410 and keeps an Overweight rating on the shares.

Morgan Stanley

Morgan Stanley downgraded to Underperform from Outperform at Wolfe Research

Wolfe Research analyst Steven Chubak double downgraded Morgan Stanley to Underperform from Outperform with an unchanged price target of $92. The stock's valuation "screens rich," especially when compared with its retail broker peers, Chubak tells investors in a research note. In addition, the analyst believes Morgan Stanley's net interest income is likely to peak in Q4 of 2022 or the first half of 2023, which he thinks should put pressure on operating margins. The company's organic growth is also likely to run below target levels into 2023, adds Chubak.

Morgan Stanley price target raised to $125 from $105 at Barclays

Barclays analyst Jason Goldberg raised the firm's price target on Morgan Stanley to $125 from $105 and keeps an Overweight rating on the shares.