Alphabet is expected to deliver year on year revenue growth, but earnings are expected to be negatively impacted from the group’s digital advertising operations. Revenue is however expected to be supported by Alphabet’s cloud services which has been a key growth driver for the business.

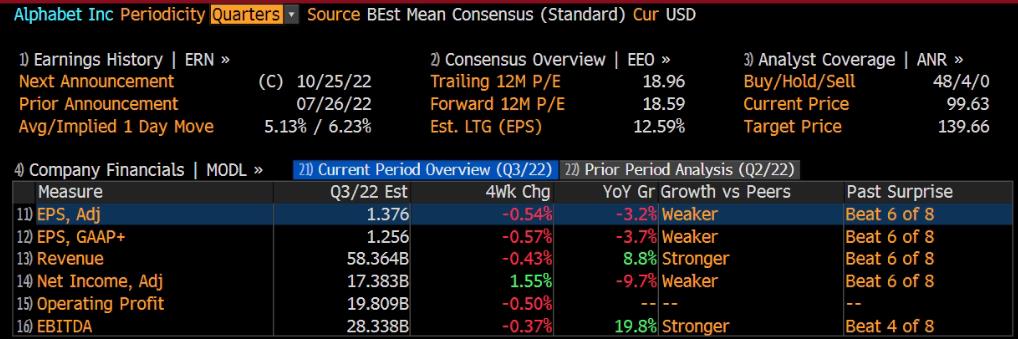

Alphabet will be issuing its quarterly earnings data after the market closes on Tuesday, October 25th. The tech giant is expected that revenue in the third quarter of 2022 is $58.368 billion, adjusted net income is $17.383 billion, and adjusted EPS is $1.376, according to Bloomberg's consensus expectation.

Last Quarter Review

Alphabet last posted its quarterly earnings data on Tuesday, July 26th. The information services provider reported $1.21 earnings per share (EPS) for the quarter, missing the consensus estimate of $1.27 by ($0.06). Alphabet had a return on equity of 28.65% and a net margin of 25.89%. The business had revenue of $57.47 billion for the quarter, compared to analysts' expectations of $57.55 billion. During the same quarter in the prior year, the firm earned $27.26 earnings per share. On average, analysts expect Alphabet to post $5 EPS for the current fiscal year and $6 EPS for the next fiscal year.

Current Period Overview

Though consensus for Alphabet's top-line growth has been lowered by about 8% for 2023, the company could see further negative revisions amid continued softness in digital-ad spending. Increased YouTube Shorts traction may have aided engagement vs. TikTok and impressions gains for the segment, in which consensus has moderated to 4% in 3Q. Search-ad spending might stay resilient, though tougher comparisons could weigh on growth expectations through 1Q23. Alphabet's ad pricing faces less headwind from Apple's IDFA changes.

Operating losses for the Cloud and Other Bets segments may remain a drag on Alphabet's free-cash-flow expectations and its valuation multiple relative to large tech peers.

Digital Advertising slows down further

Building on a negative global economic outlook, digital advertising - which remains Google's major revenue and profitability driver - has sharply slowed in 2022.

According to consulting company Magna, global advertising spending is set to grow only 9% this year which is below the company's previous forecast of 12%. However, the firm also said that current spending on digital advertising is still above the longer term (2015-2019), pre-pandemic average of 7%... which could potentially indicate that ad-spending has further to fall.

Considering that inflation remained elevated in the third quarter and Apple’s iOS changes weren’t reversed, advertisers will likely have maintained cautious spending attitudes and further dialed down ad campaigns in the third quarter. For those reasons, Google is likely to report a sequential slowdown in Google’s advertising revenue growth.

But investors should consider that inQ2 2022, Google's advertising business, which includes YouTube ads, Search ads and Network ads, has grown to $56.3 billion, a 12% year-over-year increase and a 3% quarter-over-quarter increase, respectively. Thus, Alphabet's business spending should actually be more resilient than what markets might expect and price.

Strong Google Cloud

Throughout the year, the three largest players - Microsoft (MSFT), Amazon (AMZN), and Google - have highlighted strong demand for cloud solutions and believes persist that cloud solutions could be a "deflationary force in an inflationary economy,"as Microsoft CEO Satya Nadella has highlighted.

Google Cloud still accounts for less than 10% of Google's total revenues (as of Q2 2022), but the segment has grown to be a key business driver for the search giant. And a positive performance from GC would definitely support sentiment towards Google stock. For reference, the cloud business unit is expected to generate 2022 revenues of $26.9 billion and an operating loss of approximately $3.7 billion (Bloomberg Intelligence). If an analyst believes that a x10 EV/Sales multiple for Google's cloud business is reasonable, any upside surprise for the revenue outlook could materially push the company's valuation higher.

More Buybacks

More buybacks from Google are highly likely. There are three considerations to point out.

First, Google has almost no debt ($96 billion of net cash). And accordingly, the discussion regarding if free cash flow should be used to retire debt or stock should be easily solved in favor of stock repurchase.

Second, Google stock is trading at a decade-low valuation, at a Price-To-Cash Flow ratio (TTM reference) of about x12.8. If Google management is shareholder friendly, a stock repurchase program should be strongly considered.

Third, Google can easily afford a multi-billion equity repurchase program, given that the Internet giant's cash from operations touches $95 billion/year (TTM reference). If Google wants to be really aggressive, and also wants to draw on the idle cash balance, the company could aim for a 10% annual buyback yield.

For reference,during Q2 2022, Google repurchased $15.2 billion of stock, which implies an annualized yield of about 4.7%.

Risks To Q3 Earnings

Betting on earnings is risky -- even for the FAANGS. Remember the 30% sell-off for Netflix (NFLX), twice, and the 30% sell-off for Meta Platforms. No matter how well-researched a company's quarterly performance is, there always remains some uncertainty. And this uncertainty is a risk.

That said, investors should also consider that the risk may not be in the past Q3 quarter, but in the upcoming Q4 2022 and Q1 2023 quarters, which could preliminary disappoint due to a weak guidance.

Analyst views

Bloomberg data shows a consensus of (48) analyst ratings at ‘buy’ for Alphabet Inc. A mean of estimates suggests a long-term share price target of $139.66 for the company. The current share price trades at a 40% discount to this assumed long term fair value (as of the 19th of October 2022). While Since October this year, we have seen some analysts successively lowered Alphabet's target price.

MKM Partners analyst Rohit Kulkarni lowered the firm's price target on Alphabet to $134 from $140 but keeps a Buy rating on the shares as part of a broader research note into Internet names. Companies reporting Q3 results are expected to have a cautious tone on earnings calls, citing currency headwinds and low visibility heading into the critical holiday shopping period, the analyst tells investors in a research note.

Credit Suisse analyst Stephen Ju lowered the firm's price target on Alphabet to $134 from $140 and keeps an Outperform rating on the shares ahead of quarterly results. The analyst also decreased his FXN growth estimates for 2023 as advertiser conversations for online/digital budget growth indications are "understandably decelerating sharply" to mid-single-digits. With that in mind, the automation-of-advertising theme, which has placed Google as a relative share gainer amidst IDFA deprecation and subsequent macro uncertainty-driven outlook deterioration, will remain resilient through the second half of 2022, Ju says. Near-term his checks indicate in-line results for Q3 and potentially modestly accelerating budgets for Q4. That said, similar to the first half of 2022 results, he has assumed greater Performance Max-driven allocation of budgets toward Search versus YouTube.

Morgan Stanley analyst Brian Nowak lowered the firm's price target on Alphabet to $135 from $145 and keeps an Overweight rating on the shares. His recent conversations in the industry indicate that the online ad market seems to be holding in "relatively well" and he still expects about 11% year-over-year U.S. online ad growth in 2022, but trends vary widely by ad vertical, Nowak tells investors. He expects Alphabet to miss consensus revenue and EBIT estimates for Q3, but would be a buyer on weakness, citing valuation, Nowak noted.

BofA analyst Justin Post lowered the firm's price target on Alphabet (GOOGL) to $114 from $125 and keeps a Buy rating on the shares. He has lowered his estimates for both Alphabet and Meta (META) on the potential top-down impact of a possible Western economy GDP recession as well as potential headwinds from TikTok monetization, Amazon (AMZN) ad growth, and new ad-supported streaming competition. Street estimates for Alphabet and Meta advertising revenues are "likely too high for 2023," but he sees potential for strong EPS resiliency for both from cost cutting in 2023, much like in 2009, Post said. Alphabet and Meta remain "top value stocks in the group," the analyst added.

Alphabet handled the difficult economic environment well in Q2, and whilst It is expect Q3 to look like a poor result on paper, the market is already expecting poor results. But the question is this – how much of that pessimism is already reflected in the current share price? Alphabet shares has fallen by 21% this year. Is it time to rebound?