Microsoft's fiscal 1Q23 results might highlight slowing growth across most of its product lines, with the greatest impact likely on its Windows unit within the More Personal Computing segment.

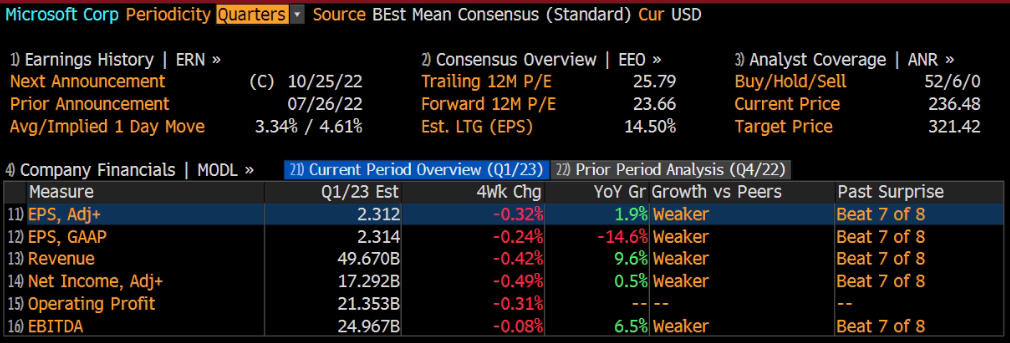

Microsoft will release its F23 Q1 earnings data after the market closes on Tuesday, October 25th. Investors are wondering whether Microsoft can overcome the headwinds of rapidly softening computer demand, and a slowdown in technology spending.

The tech giant is expected that revenue is $49.67 billion, adjusted net income is $17.292 billion, and adjusted EPS is $2.312, according to Bloomberg's consensus expectation.

Last Quarter Review

Microsoft last posted its earnings results on Tuesday, July 26th. The software giant reported $2.23 earnings per share (EPS) for the quarter, missing analysts' consensus estimates of $2.28 by ($0.05). The firm had revenue of $51.87 billion during the quarter, compared to the consensus estimate of $52.31 billion. Microsoft had a net margin of 36.69% and a return on equity of 43.31%. During the same quarter last year, the firm posted $2.17 EPS. On average, analysts expect Microsoft to post $10 EPS for the current fiscal year and $12 EPS for the next fiscal year.

Current Period Overview

Microsoft's fiscal 1Q23 results might highlight slowing growth across most of its product lines, with the greatest impact likely on its Windows unit within the More Personal Computing segment. Increasing global economic challenges are curtailing new PC buying, especially in the consumer market, and this weakness is expected to hurt Windows growth in 1Q and through most of 2023. 2Q guidance may be below estimates, driven by the persistent strength of the dollar compared with other currencies.

Intelligent Cloud

Microsoft's crown jewel in focus will undoubtedly be the intelligent cloud segment, which is its highest-growth business and takes up 40% overall revenue. Growth is expected to slow, but remains at an elevated level of about 20%.

To counter the negative impact of a slowing, Microsoft has already announced to slow down hiring, as well as potentially laying off existing employees. According to various news outlets, the workforce reduction is predominantly affecting Microsoft's cloud and security units.

Previous quarter’s results continued to point towards strong momentum with a 25% increase in commercial bookings, so some resilience could still be presented this time round. The key question will fall on the company’s outlook.

Citi Research analyst Tyler Radke recommended investors take a longer-term view on the software company’s strong growth potential and look beyond macro-related issues. His view is Microsoft’s “cloud-related revenue streams will enable growth to continue at double-digit levels with operating-margin expansion.”

Personal Computing

The outlook for PC sales has been deteriorating through 2022. According to IDC, worldwide shipments of personal computers fell 15% in the June quarter from a year earlier, after a 5% year-over-year decline in the March quarter. Earlier this month, the research firm said September-quarter PC shipments also fell by 15%.

Microsoft's personal computing division accounts for about one third of sales and includes Windows OEM products, Xbox content and services, Search and news advertising, as well as Microsoft Surface.

The personal computing division already slowed in Q4 FY 2022, increasing revenues only by about 2% year over year to $14.4 billion. Also, the September quarter marked a further slowdown in global PC demand - the steepest demand decline in over two decades.

Investors should not demand for too much positivity here. But expectations are likely already very low.

Productivity and Processes

Reflecting on Microsoft's September quarter, the key (open) question is the performance for 'productivity and processes'. A few months ago, Microsoft management commented that the segment is expected to grow between 12% and 14% in constant currency or $15.95 billion to $16.25 billion. And also added:

In Office commercial, revenue growth will again be driven by Office 365 with seat growth across customer segments and ARPU growth through E5. We expect Office 365 revenue growth to be sequentially lower by roughly two points on a constant currency basis with a bit more FX impact on U.S. dollar growth than at the segment level.

Although productivity gains and process-optimization efforts should be key for businesses in a challenging economic environment, it is doubtful whether businesses will actually invest in such 'optional' initiatives.

The lower estimate of the revenue guidance range ($15.95 billion) will be a more likely scenario.

Other Considerations

In Q4 2022, Microsoft returned to shareholders $12.4 billion in the form of share repurchases and dividends. There could be considerable upside to this number in Q1 2023 and/or in the future -- given that Microsoft is a net-creditorand generates about double the operating cash flow as compared to what has been distributed in FY Q4 2022.

Microsoft's business is strongly anchored on asubscription-based business model.Accordingly, it is very unlikely that the company's revenues and cash flows fluctuate enormously quarter over quarter. Note that as of June 2023, Microsoft recorded on the balance sheet about $43.5 billion of unearned revenues.

Investors should consider that the risk may not be in the past Q1 2023 quarter, but in the upcoming Q2 2023 and Q3 2023 quarters, which could preliminary disappoint/surprise due to a weak/strong guidance.

Analyst views

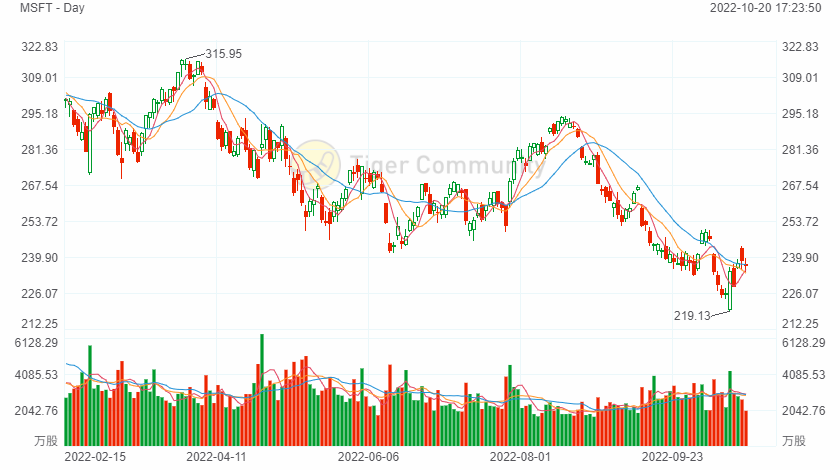

Bloomberg data shows a consensus of (52) analyst ratings at ‘buy’ for Microsoft. A mean of estimates suggests a long-term share price target of $321.42 for the company. The current share price trades at a 36% discount to this assumed long term fair value (as of the 19th of October 2022). While Since October this year, we have seen some analysts successively lowered Alphabet's target price.

Cowen analyst Derrick Wood lowered the firm's price target on Microsoft to $310 from $320 and keeps an Outperform rating on the shares. The analyst thinks an in-line Azure print and 2Q guidance should give investors comfort in core growth trends.

Citi analyst Tyler Radke lowered the firm's price target on Microsoft to $282 from $300 and keeps a Buy rating on the shares. Currency and PC headwinds are likely to impact the company's fiscal Q1 results and may drive reported results below consensus again, Radke tells investors in a research note. That said, the analyst's reseller survey and partner checks give him confidence that enterprise demand for Microsoft is holding up well, with record partner quota/accelerator achievement levels and incremental signs of Azure demand strength. He expects Microsoft to show more resilient growth trends versus peers.

Morgan Stanley analyst Keith Weiss lowered the firm's price target on Microsoft to $325 from $354 and keeps an Overweight rating on the shares. Ahead of earnings, he has reduced his revenue forecast for fiscal Q1 by 1% and for FY23 by a bit over 2% given the weaker PC demand environment and rising foreign exchange headwinds, though Weiss thinks sustained momentum in Microsoft's Commercial business should serve as a partial offset as the company continues to gain IT budget share. The longer-term teens total return profile and an "attractive valuation" continue to make Microsoft one of his top ideas, Weiss added in his Q1 earnings preview note.

Microsoft shares have dropped nearly 30% so far this year, which is roughly in line with the tech-laden Nasdaq Compositeindex’s 31% decline. Thinking ahead, what's next?